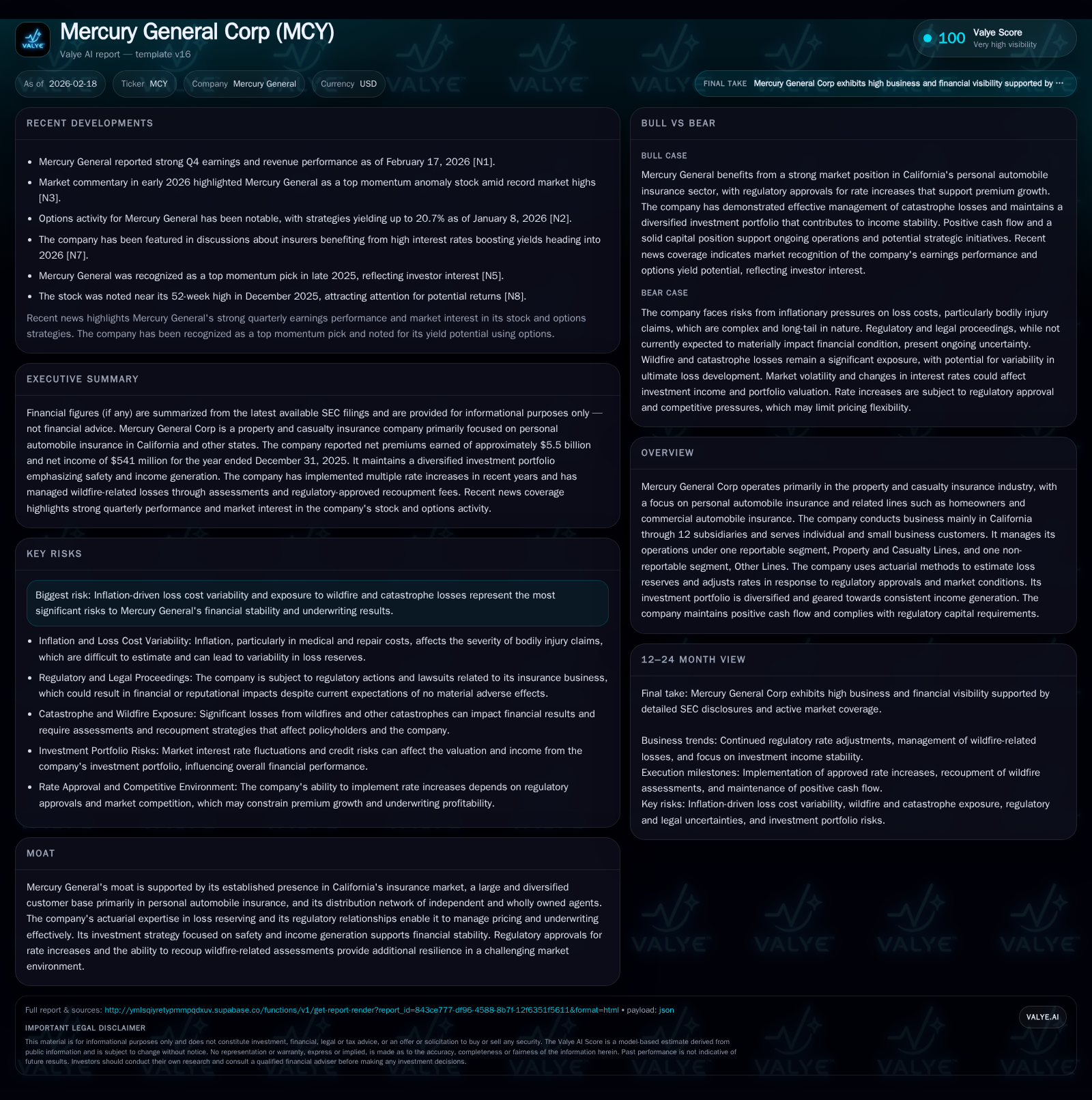

Mercury General’s 2025 Surge: California Market Dynamics and Investment Strategies Fuel Expansion

Mercury General Corp’s robust 2025 financial growth is underpinned by strategic rate hikes in California and a conservative investment portfolio emphasizing income generation.

In 2025, Mercury General Corp achieved significant revenue and net income growth driven by strong personal automobile insurance premiums and successful execution of rate increases approved by the California Department of Insurance (DOI). The company’s actuarially-grounded underwriting strategy, combined with evolving wildfire-related regulatory frameworks, has enhanced its pricing power amidst substantial catastrophe exposures. Mercury’s disciplined capital allocation complemented by strong operational cash flow and a diversified fixed maturity portfolio has maintained liquidity and financial resilience. Looking ahead, implementation of new catastrophe modeling rules and market-share mandates will be critical to sustaining underwriting profitability in a challenging environment.

Evolution of Revenue and Earnings: Tracking Mercury’s Growth Engines

Mercury General Corp posted solid top- and bottom-line expansion in fiscal year 2025, highlighted by revenue growth from $5.48 billion in 2024 to approximately $5.99 billion—an increase of about 9.4% [F1]. Net income showed even stronger momentum, rising from $468 million in 2024 to $541 million in 2025, reflecting a substantial gain of roughly 15.6% [F1].

This uplift was largely propelled by the company’s principal line: personal automobile insurance within California markets. Private passenger auto policies represented about 49% of total net premiums earned in California during the period [S1]. Rate increases were central to this gain, notably including a February 2024 premium rate hike averaging approximately 22.5%, approved for key subsidiaries MIC and CAIC [S1]. Homeowners insurance also contributed incrementally through successive rate adjustments realized in mid-2024 (7%) and early 2025 (12%), further buttressing revenue [S1].

The management’s reliance on actuarially rigorous underwriting coupled with calibrated pricing changes accounted for improved loss ratios compared to prior periods despite elevated catastrophe claims volatility [S7]. While operating income details are not disclosed explicitly via filings, positive cash flow trends corroborate efficient expense management parallel with underwriting gains [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6.0 | 541 | 1087 | 58 | +9.4% | +15.6% |

| 2024 | 5.5 | 468 | 1037 | 46 | +18.3% | +385.8% |

| 2023 | 4.6 | 96 | 453 | 37 | +27.1% | +118.8% |

| 2022 | 3.6 | -513 | 353 | 36 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1029 | 22.4 | |

| 2024 | 991 | 24.0 | |

| 2023 | 70 | 416 | 6.2 |

| 2022 | 105 | 317 | -33.7 |

Source: SEC companyfacts cache [F1].

Note: Operating income not available; Buyback data unavailable.

California Regulatory Landscape: Impacts on Pricing and Risk Management

California continues to set stringent conditions shaping Mercury’s underwriting playbook through its "Sustainable Insurance Strategy." Notable regulations enacted late in 2024 authorize insurers like Mercury to incorporate catastrophe modeling into rate-setting processes while requiring them to maintain market share thresholds—beginning at aligning wildfire-prone area policy coverage to at least 85% of statewide market share with potential upward adjustments annually [S1], [S27]. Additionally, recent directives enable explicit inclusion of reinsurance costs related to specific wildfire perils within rates upon meeting these regulatory benchmarks.

Simultaneously, reforms to the California FAIR Plan facilitate stabilizing assessment recoveries from insured parties following catastrophic events via pre-approved supplemental fees capped at specified industry-wide loss thresholds—mechanisms Mercury has actively navigated given its exposure profile [S1], [S27]. The Company received approval for its enhanced rating application integrating these elements effective July 2026—a milestone that requires close attention to implementation and compliance dynamics going forward.

Compared with prior regulatory constraints that limited pricing flexibility or recovery of catastrophe-related expenses, these developments improve Mercury's capacity to secure adequate premium income reflective of risk-adjusted cost structures amid volatile wildfire exposures.

Wildfire Exposures: Navigating Catastrophe Losses with Actuarial Precision

Mercury faces material wildfire-related claims burdens highlighted by its $50 million assessment levied by the California FAIR Plan after the Palisades and Eaton wildfires jolted industry capital reserves early in 2025 [S1], [S7], [S15]. Through regulatory allowance for temporary supplemental fees, the firm recouped half of this direct outflow via policyholder surcharges—a reflection of strengthened actuarial leverage embedded within loss reserving protocols.

The company applies stochastic catastrophe modeling alongside traditional reserving techniques calibrated for inflationary pressures exacerbated by geopolitical tariff escalations that inflate repair/replacement costs for damaged properties [S2]. This combination supports disciplined setting of loss reserves inclusive of incurred but not reported (IBNR) estimates consistent with observed claim development patterns.

Chronology-sensitive actuarial processes ensure timely adjustment cycles responsive to characteristics underlying wildfire season intensity variability while keeping resilience measures aligned with emerging legislation mandates.

Investment Portfolio Strategy: Income Focus Amid Market Uncertainty

A critical pillar underpinning Mercury General's financial stability is its investment strategy prioritizing principal safety balanced against consistent income yield generation within a total return framework [S1], [F1]. The portfolio predominantly comprises high-quality municipal securities (65% of fixed maturities at fair value), complemented by corporate bonds (14%), mortgage-backed securities (about 5%), collateralized loan obligations (13%), and modest allocations to other asset-backed issues [S1].

Weighted-average credit quality stands robust around A+ with strategic duration management optimized for matching projected claim payout obligations without an explicit asset-liability duration matching policy—favoring opportunistic total return enhancements instead [S21]. The firm tactically adapts allocations considering credit rating trajectories, macroeconomic volatility including interest rate shifts linked to Federal Reserve policy trends.

Municipal holdings benefit tax-exempt status enhancing after-tax income—a relevant factor given the emphasis on reliable yield as opposed to aggressive capital appreciation strategies under prevailing financial market uncertainty.

Cash Flow Robustness and Liquidity Management: An Operational Overview

Since its public offering in November 1985, Mercury has consistently generated positive operating cash flows, reaffirmed by the $1.09 billion recorded in FY2025—a nearly 5% increase from the previous year’s $1.04 billion [F1], [S14]. The upsurge reflects improved premium collections alongside increased proceeds from reinsurance recoveries and subrogation initiatives despite elevated claims payments linked partly to wildfire losses.

With cash plus short-term investments totaling approximately $1.65 billion at year-end 2025 along with a $250 million revolving credit facility (of which $200 million was drawn as working capital buffer), liquidity remains ample without reliance on forced security dispositions under stressed claim event scenarios [S4], [S14].

Debt-to-total-capital ratio stood at a conservative ~19%, comfortably within covenants under revolving credit terms priced near SOFR plus ~112bps—further reinforcing financial flexibility for risk mitigation or selective opportunistic deployment [S10], [S17].

Capital Allocation Priorities: Dividends, Repurchases, and Financial Discipline

Mercury General maintained steady shareholder return policies distributing approximately $70 million annually in dividends over recent years (including FY2025) consistent with Board-declared quarterly dividend payouts (e.g., the March 26, 2026 payment at $0.3175/share expected amounting close to $18 million) [F1], [S18]. No publicly disclosed common stock repurchases or buybacks have been reported indicating a preference toward capital retention aligned with regulatory constraints and ongoing business reinvestment demands.

Equity has grown significantly from $1.55 billion in FY2023 through $2.42 billion by year-end FY2025 driving an approximate return on equity nearing an attractive ~22.4%, evidencing disciplined capital stewardship balancing profitable underwriting returns with prudent dividend distribution frameworks suitable for an insurance holding structure [F1], [S18], [S25].

Capital expenditures also expanded sharply (+26.6% YoY in FY2025), reflective of priority investments into technology infrastructure crucial for underwriting analytics modernization and operational efficiency improvements—essential capabilities given increasing reliance on actuarial precision against catastrophe-related risk costs [F1], [S16].

Looking Ahead: Regulatory Milestones, Market Conditions, and Key Performance Indicators to Watch

The upcoming activation of Mercury's approved updated rating plan incorporating comprehensive catastrophe modeling approaches scheduled for July 2026 will be a pivotal inflection point influencing near-term pricing power and underwriting margins under persistent wildfire frequency risks documented since early-2025 loss events [S1]. Monitoring adherence to mandated market share requirements especially within high-risk zip codes will further reveal strategic effectiveness adapting to layered regulatory expectations.

Additionally, key performance indicators such as combined ratio trajectory post-implementation of enhanced loss cost assumptions adjusted for inflationary trends—including tariff-driven input cost escalations—and new business volumes within targeted California segments merit close observation as leading signals informing longer-term profitability sustainability frameworks.[N1],[S1]

Though explicit forward guidance remains absent formally from filings,[N1] analysts should closely track quarterly results releases emphasizing changes outlined above as proxies for evolving competitive positioning amid an increasingly complex wildfire exposure landscape entwined with evolving DOI oversight policies.

This analysis integrates publicly available disclosures as of February 18, 2026 ([F1],[N1],[S#]) without extrapolating or assuming undisclosed metrics or outcomes beyond stated factual content or regulatory announcements. It aims solely at providing a comprehensive view detached from investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments