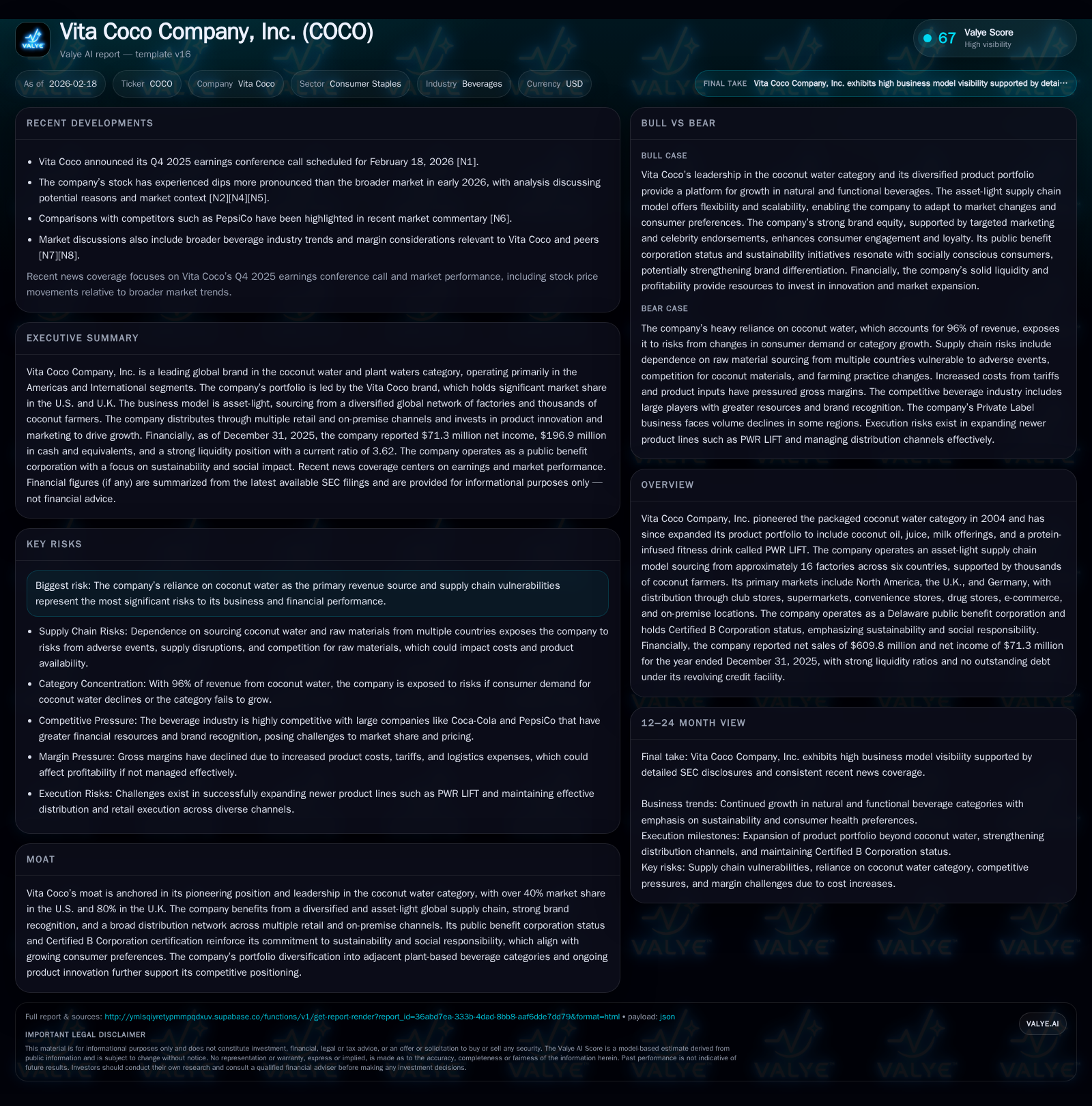

Vita Coco’s Brand Leadership Faces Supply Chain and Category Growth Challenges

Strong historical growth supported by coconut water dominance confronts supply-side pressures and category dependence.

Vita Coco Company, Inc. has solidified its leadership in the global coconut water market through pioneering efforts since 2004 and a diversified asset-light supply chain sourced from multiple countries. Despite achieving $609.8 million in net sales and $71.3 million net income in 2025, the company remains heavily dependent on coconut water, representing roughly 96% of revenues, exposing it to category-specific demand risks. Ongoing tariff volatility, shipping disruptions, and supplier concentration represent significant headwinds to margin stability. While expanding product offerings into adjacent plant-based beverages and fitness drinks, these remain nascent relative to core coconut water sales. Its strong capital structure with negligible debt supports continued marketing investments and innovation, but future growth hinges on scaling non-coconut water products and mitigating supply chain constraints.

Historical Performance and Growth Drivers

Founded as the pioneer of packaged coconut water in 2004, Vita Coco Company has built a commanding presence within its niche beverage category. The company reported net sales of approximately $609.8 million for fiscal year 2025 alongside operating income of $82.5 million and net income of $71.3 million [F1]. This continues a strong annual improvement trend: operating income rose from roughly $3.1 million in 2022 to $82.5 million in 2025, while net income grew from $7.8 million to $71.3 million over the same period [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 71 | 47 | 83 | 8 | +27.5% |

| 2024 | 56 | 43 | 74 | 1 | +20.0% |

| 2023 | 47 | 107 | 56 | 1 | +496.7% |

| 2022 | 8 | -11 | 3 | 1 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | 39 | 21.5 |

| 2024 | 12 | 42 | 21.6 |

| 2023 | 1 | 107 | 23.0 |

| 2022 | 0 | -12 | 5.5 |

Source: SEC companyfacts cache [F1].

*Note: Full revenue disclosure not available; estimate based on narrative [N1], SEC filings [S1].

Profitability gains were driven by expanding branded-market share—Vita Coco holds over 40% U.S. share and roughly 80% in the U.K.—and private label contracts across North America and Europe [S1][S7]. Its asset-light model sourcing from approximately sixteen factories across six countries enables scalability without heavy capital expenditures [S1].

Core Product Dependence and Portfolio Diversification

Despite portfolio expansion into coconut oil, juice, milk products, and PWR LIFT protein-infused fitness drinks, Vita Coco remains highly reliant on its core coconut water segment which accounted for about 96% of revenue in fiscal 2025 [S8][F1]. The company discontinued less synergistic lines such as Runa energy drink (ceased end-2023) and Ever & Ever sustainably packaged water (ceased production in 2024), signaling focus tightening but highlighting challenges diversifying beyond flagship products [S1][S20].

The growing consumer interest in plant waters and low-sugar hydration supports growth potential; however, elevating new product revenue above current low bases remains uncertain [S11].

Operational Performance: Supply Chain Under Pressure

Vita Coco operates a global asset-light supply chain fully reliant on third-party partners—about sixteen factories supplied by thousands of farmers across Asia-Pacific and Latin America—which affords flexibility but exposes the business to external shocks [S1][S7].

Tariff changes notably increased input costs during the year—U.S.-imposed tariffs averaged around a weighted rate of approximately 23%, with some origins facing up to an effective rate of ~50% before partial relief announced late-2025—and complicated sourcing decisions [S1][S16][S21]. Ocean freight volatility amid geopolitical tensions further pressured expenses [S18]. These cost increases are challenging to fully pass through due to consumer price sensitivity [S4][S16].

Private label agreements provide important revenue streams but carry risks from regular rebids and abrupt contract changes including recent regional volume losses with a major customer discontinuing parts of their supply early-2024 yet potentially restarting regionally in early-2026 [S8][S23].

Financial Strengths and Capital Allocation

Liquidity is robust with approximately $196.9 million in cash equivalents at year-end compared to $116 million in current liabilities, yielding a healthy current ratio near 3.6x [F1][S5]. The company carries minimal debt aside from immaterial vehicle loans with zero drawn on a revolving credit facility providing $60 million capacity maturing February 2030 [S5][S14].

Operating cash flow grew moderately (+10%) year-over-year to $47.2 million despite working capital demands likely linked to inventory buildup amid supply chain challenges [F1][S6]. Capital expenditures rose sharply (~$8.15 million vs ~$974k prior year), mainly reflecting investments in office infrastructure across New York, London, Singapore rather than production assets consistent with their asset-light model [S6].

Share repurchases continue as part of capital return strategy totaling $11.3 million in fiscal ’25, slightly down from prior year; dividends are not disclosed indicating none or minimal payouts currently [F1]. The firm prioritizes reinvestment into marketing innovation while maintaining shareholder returns via buybacks.

Industry Positioning and Competitive Environment

Operating within functional beverages aligned with health-conscious trends positions Vita Coco well given its Certified B Corporation status reflecting ESG commitments resonant with evolving consumer values [S1]. However, it faces competition from multinationals expanding plant waters portfolios alongside private labels challenging shelf space.

Retail consolidation risks pricing pressure as fewer retailers control more shelf space potentially reducing margin leverage [S19]. Expanding e-commerce channels including direct-to-consumer remain critical given shifting shopping behaviors though balancing visibility between physical stores and digital marketplaces is complex [S11].

Risks Summary

- Heavy dependence on coconut water exposes revenue to category contraction or changing consumer preferences.

- Tariffs create raw material cost uncertainty; ocean freight disruptions add supply unpredictability.

- Private label contract volatility risks rapid shifts in volume or margins.

- Regulatory scrutiny around labeling claims such as "natural" or "non-GMO" poses reputational risks requiring compliance vigilance [S13].

- Competition includes resourceful multinationals capable of aggressive pricing/marketing alongside innovative startups.

- Currency exposure inherent due to international sourcing is managed via hedging programs but remains a risk factor [S4].

Growth Outlook: Catalysts and Constraints

While explicit forward guidance is not provided, management highlights several growth priorities:

- Broadening innovation pipeline beyond coconut water including fitness-focused PWR LIFT appealing to wellness markets [N1][S11].

- Expanding international market penetration leveraging brand recognition plus local partnerships [S7].

- Growing e-commerce footprint particularly direct-to-consumer addressing changing buying behaviors [S11].

- Enhancing operational efficiency within supply chain while navigating tariff environments [S1].

- Leveraging sustainability credentials aligned with consumer preferences.

Constraints include potential limits imposed by overall category growth rates plus challenges managing rising input costs while protecting margins.

What To Watch Next

Key indicators include:

- Quarterly shipment volumes outside Americas segment revealing geographic diversification progress.

- Product mix shifts showing increased contributions from non-coconut water products.

- Updates on tariff or trade policy developments impacting sourcing costs.

- Private label contract renewals or losses affecting near-term revenues.

- Marketing spend effectiveness versus consumer retention/growth metrics indicating ROI.

- Announcements regarding strategic partnerships or acquisitions extending product portfolio footprint.

Conclusion

Vita Coco Company remains a leader within its functional beverage niche through pioneering brand strength combined with an asset-light flexible global supply model serving key markets worldwide. Its financial performance reflects strong profit growth supported by prudent capital management enabling ongoing investment behind brand equity and innovation.

However, significant reliance on coconut water creates vulnerability should category demand weaken or competition intensify unfavorably. Operational challenges stemming from tariff escalations and ocean freight disruptions also pressure cost structures despite mitigation attempts.

The company's ability to expand beyond core coconut water products while sustaining profitability amid supply chain headwinds will be central to translating past momentum into diversified longer-term growth that balances shareholder value creation with embedded sustainability principles.

This analysis is based solely on publicly available information including SEC filings ([S#]) and recent news transcripts ([N#]). No investment advice or forecasts are provided; this report aims only to deliver informed insights into operational factors shaping Vita Coco Company’s financial condition and strategic outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments