5E Advanced Materials Battles Liquidity Strains While Driving Boric Acid Innovation for LCD Applications

5E Advanced Materials advances its boric acid technology for LCD glass amid financial headwinds and ongoing capital raises.

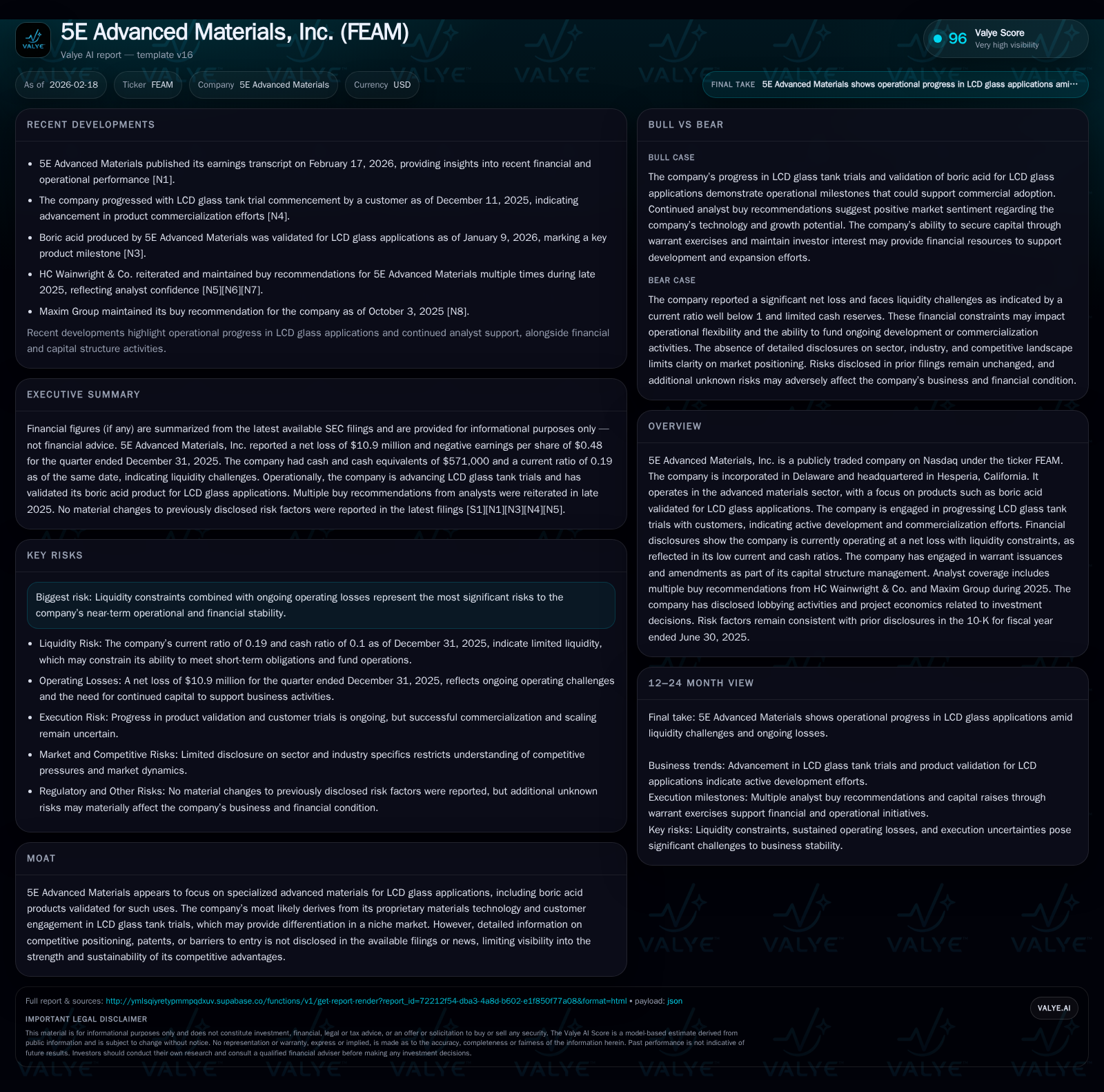

5E Advanced Materials, Inc. (FEAM) operates at the nexus of specialized boron chemistry and nascent LCD substrate markets but continues to face liquidity challenges and operating losses. The company has validated its boric acid product for critical LCD glass applications and is progressing through customer tank trials, signaling forward momentum in commercialization. However, recent financial disclosures reveal a tight balance sheet with a current ratio under 0.2 and persistent negative cash flow, prompting a $36 million equity raise in early 2026 to support scaled facility operations and mine development. Key forthcoming milestones include FEED engineering and commercial mine plan finalization, which could underpin future growth if executed amid the company’s structural financial constraints.

From Consecutive Operating Losses to Technology Validation: Historical Financial and Operational Trajectory

Since FY2022, 5E Advanced Materials has charted a path marked by sustained operating losses as it invests heavily in developing its specialized boron-based materials technology targeting the LCD glass market. Operating income losses declined from -$67.8M in FY2022 to -$35.9M in FY2024, followed by a further reduction estimated at -$43.7M by mid-FY2025 [F1]. Net income followed a similar pattern: a loss of -$66.7M in FY2022 improved slightly over subsequent years but remained heavily negative (-$62.0M in FY2024) [F1]. These results reflect extensive R&D spending alongside scale-up costs typical for a company transitioning from technology development toward early commercial validation.

Despite the financial strain, the company announced successful validation of its boric acid product for LCD glass applications by early 2026 [N3], demonstrating significant operational progress amid this challenging backdrop. This duality—financial pressure coexisting with product milestone achievements—defines FEAM’s recent trajectory.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -32 | -24 | -44 | 124000 | +49.1% |

| 2024 | -62 | -27 | -36 | 88000 | -102.5% |

| 2023 | -31 | -31 | -37 | 352000 | +54.1% |

| 2022 | -67 | -29 | -68 | 1220000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | -49.9 |

| 2024 | -27 | -579.2 |

| 2023 | -31 | -57.2 |

| 2022 | -30 | -106.5 |

Source: SEC companyfacts cache [F1].

*Note: Revenue data unavailable; Capex reflects property and equipment investment.

Specialized Boric Acid for LCD Glass: Technology Highlights and Customer Engagements

At the heart of FEAM's strategy lies its proprietary boric acid formulation optimized for LCD glass production—a niche but critical component that enhances substrate performance characteristics such as durability and clarity [N3]. The company is actively engaged in customer 'tank trials,' an industry term denoting preliminary manufacturing line tests using new material formulations under controlled conditions yet prior to full-scale adoption, signaling real-world validation within client supply chains.

The emphasis on 'boron specialty chemicals' tailored for 'LCD substrate enhancement' showcases advanced materials sector fluency—boron compounds often play decisive roles in optimizing glass transitional properties, thermal stability, and impurity reduction crucial for high-resolution displays.

Overview of Recent Capital Raises and Impact on Corporate Liquidity

Navigating tight liquidity prompted FEAM's February 2026 public offering that raised gross proceeds of $36 million through issuance of 18 million common shares at $2 per share [S8]. After deducting placement agency fees (~7%) and expenses, net proceeds are estimated at approximately $30.3 million.

Preceding this raise were strategic warrant amendments executed in December 2025 allowing holders to exercise mostly on a cashless basis once partial cash exercises occurred [S6]. These transactions generated ~$2 million gross proceeds while increasing share count to roughly 23.5 million common shares [S7]. Despite these inflows, as of December 31, 2025 reported cash & equivalents stood at only about $571K with current liabilities exceeding current assets by over $4 million [F1], translating into a constrained current ratio near 0.19.

This fungibility between equity vehicles—warrant amendments, equity raises—and controlled dilution reflects management's tactical approach toward improving working capital while balancing shareholder interests.

Assessing Near-Term Risks: Liquidity Constraints and Operating Cash Flow Trends

Aside from technological progress, liquidity risk remains prominent given repeated operating deficits combined with suboptimal liquidity ratios documented as recently as Q2 FY2025 [F1,S2,S4,S5]. Persistent negative operating cash flows surpassing $23 million annually counterbalance modest capex outlays but produce substantial free cash flow burn (~-$23.8M latest), calculated as operating cash flow minus capex [F1]. Such dynamics imply dependency on continual external financing or transformative growth catalysts.

From an industry perspective, companies at this developmental juncture must maintain sufficient capital turnover ratios—here reflected by near zero short-term reserves—to sustain operations pending commercialization ramps or licensing monetization.

The company's risk disclosures underline unchanged principal concerns around these funding needs materially affecting ongoing viability absent timely financing or profitable market penetration initiatives [S4,S5].

Future Outlook: Planned Facility Operations, Commercial Mine Development, and Engineering Milestones

Management’s stated deployment of the recent equity raise centers on scaling small-scale boron facility operations concomitant with advancing wellfield development essential for raw material inputs [S8,N1]. Finalizing the commercial mine plan remains a pivotal engineering milestone informing feasibility studies progressing towards full-scale mining activities — necessary prerequisites to reliably supply boric acid feedstock domestically.

Furthermore, FEED (Front End Engineering Design) completion exemplifies standard industry practice governing detailed plant design before capital-intensive buildouts commence—a critical gatekeeper step ensuring engineering robustness aligns with operational targets.

Although explicit sales or production guidance is absent from disclosures [N1], these engineering achievements constitute tangible stride markers suggesting catalytic events that could shift growth trajectory contingent upon execution success.

Capital Structure Evolution: Warrants, Equity Issuances, and Governance Support

Since March 2025 restructuring events introduced warrants totaling over five million shares exercisable nearly entirely via amended cashless terms [S6], the effective management of these instruments is crucial for maintaining financial flexibility without excessive dilution.

The recent warrant exercises yielded gross proceeds near $2 million while elevating shares outstanding to approximately 23.5 million by December-end '25 [S7]. The approved increase to the equity compensation pool underscores ongoing resource allocation toward incentivizing personnel aligned with commercialization horizons [S15].

Additionally, all incumbent directors were re-elected at the December '25 annual meeting indicating governance continuity amidst strategic transition phases [S7,S21], supporting operational consistency during capital structure shifts.

No dividend payments or share repurchase programs are noted within disclosures or filings [F1,S6–S29], consistent with preservation of capital during developmental stages.

Key Metrics to Track: Operating Income Trends, Cash Flow Improvements, and Commercial Scale Progress

Close monitoring of quarterly operating income trajectories will signal whether costs stabilize or decline further reflecting potential operational efficiency gains—for instance recent fiscal reductions in operating loss of roughly -22% YoY imply some containment efforts are effective [F1].

Operating cash flow improvements (+12% YoY) despite ongoing negative values suggest potential progress towards mitigating working capital cycles though still far from breakeven states necessitating continual scrutiny [F1].

Capex modestly increased (+40%), likely reflecting incremental investments related to scaling production capabilities rather than large-scale plant construction so far; tracking changes here can offer insight into physical growth pace versus research expenditures.

Commercial milestones such as completing tank trials conversion into purchase commitments or finalizing mine development contracts remain key catalysts that could alter risk/reward calculations going forward given sector norms requiring proof points along extended supply chain validation phases.

Disclaimer: This report is provided solely for informational purposes based on public filings and news sources as cited without any investment advice or recommendations regarding securities of 5E Advanced Materials, Inc. Readers should conduct their own due diligence before making any decisions related to the company.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments