Mosaic Co's Revenue Resurgence and Margin Recovery in Fertilizer Markets

An exploration of Mosaic Co’s financial rebound in 2025 amidst cyclical challenges in potash and phosphate fertilizer markets.

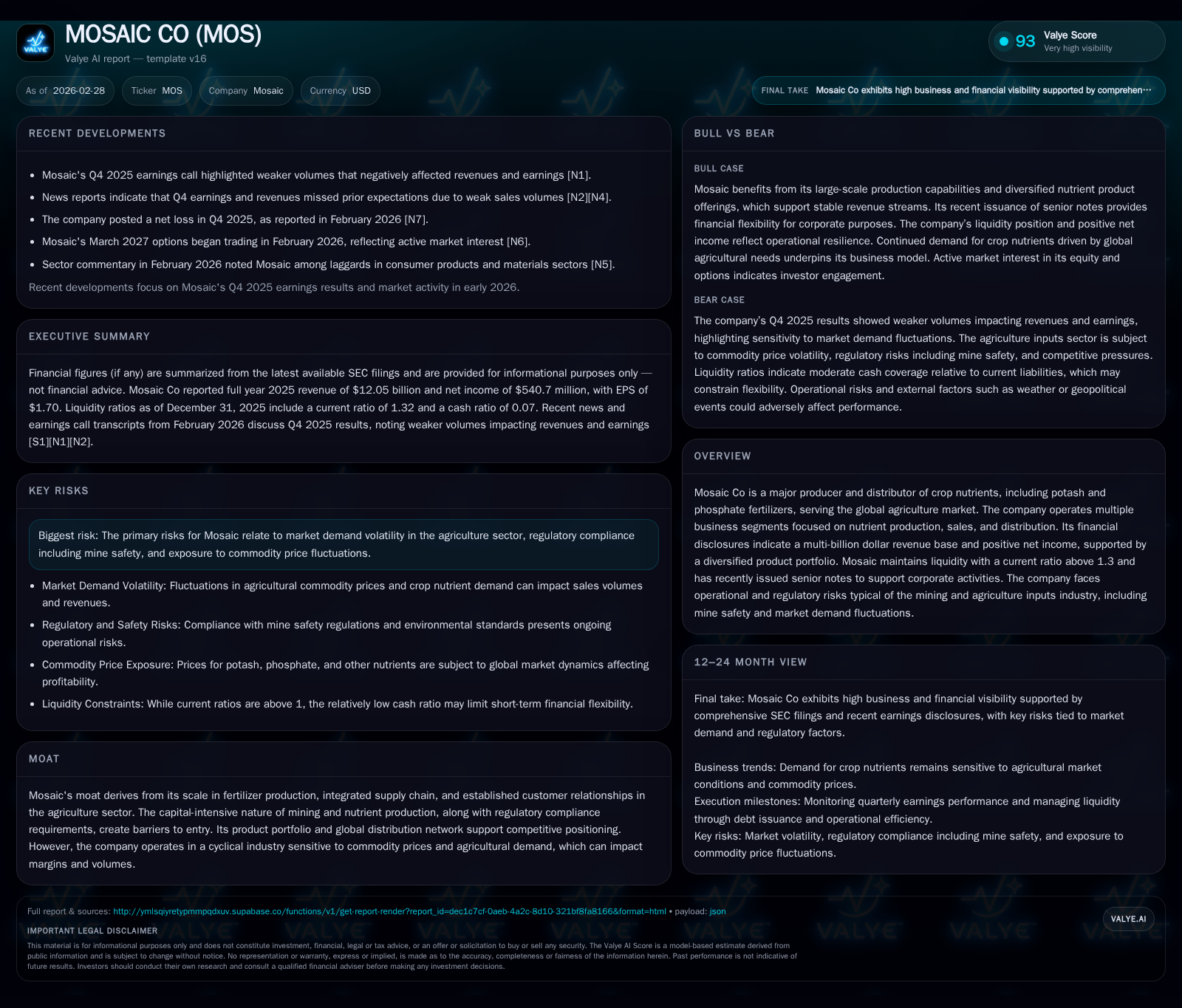

After enduring a pronounced contraction in revenue and earnings from 2022 through 2024, Mosaic Co exhibited a notable rebound in 2025 driven by improving market dynamics and operational repositioning. The company grappled with weak volumes and margin pressures throughout late 2025, linked to the intrinsic cyclicality of agricultural input demand and commodity price fluctuations. Strategic capital actions included senior note issuances to maintain liquidity, while operational focus on potash and phosphate segments reflects nuanced agricultural seasonality. Regulatory factors, particularly mine safety compliance, remain critical risk elements. Going forward, careful monitoring of volume trajectories and regulatory developments will be pivotal to sustaining profitability improvements.

Shifting Tides: Mosaic’s Historic Revenue and Profit Trends Through 2025

Mosaic Co experienced a stark revenue contraction across FY2022–FY2024, with sales declining from $19.13 billion to $11.12 billion—a nearly 42% drop—before partial recuperation to $12.05 billion in FY2025 ([F1]). Operating income displayed even more pronounced volatility: from approximately $4.79 billion in FY2022 down to $621 million in FY2024, recovering to $822 million by FY2025 ([F1]). This variability underscores the cyclical nature of fertilizer commodity markets coupled with macroeconomic factors impacting global agriculture demand.

Net income followed a similar path but with steeper troughs and moderate recovery; it tumbled from $3.58 billion in 2022 to $175 million two years later before rebounding partially to $541 million last year ([F1]). The swings highlight both volume downturns and margin compression persisting through that mid-period.

Operating cash flow offers insight into cash conversion efficacy, diminishing sharply by over one-third year-over-year going into 2025 despite slightly elevated capital expenditure levels (CapEx rising ~8.6% YoY), pushing free cash flow negative at an estimated -$535 million ([F1]). This capex intensity amid tightening cash flow reflects industry-standard capital demands within nutrient production.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.1 | 0.5 | 0.8 | 0.8 | +8.4% | +209.1% |

| 2024 | 11.1 | 0.2 | 1.3 | 0.6 | -18.8% | -85.0% |

| 2023 | 13.7 | 1.2 | 2.4 | 1.3 | -28.4% | -67.5% |

| 2022 | 19.1 | 3.6 | 3.9 | 4.8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 280 | 0 | -0.5 |

| 2024 | 271 | 235 | 0.0 |

| 2023 | 352 | 756 | 1.0 |

| 2022 | 198 | 1665 | 2.7 |

Source: SEC companyfacts cache [F1].

Table: Mosaic annual financials demonstrate precipitous drop then recovery from FY22-FY25 ([F1]).

Supply-Demand Dynamics and Commodity Price Pressures Defining Current Market Conditions

Earnings calls through Q4-2025 revealed persistent volume weakness contributing materially to quarterly revenue misses versus analyst expectations—Mosaic’s nutrient shipments lagged due to softer farmer demand linked to global crop pricing uncertainty and inventory destocking within distribution channels ([N1],[N2],[N3],[N4]).

Commodity prices for potash and phosphate fertilizers remained under pressure during late-2025 as elevated inventory levels tempered pricing power, exerting oscillatory impacts on margins ([S1],[S5]). The company highlighted fluctuating channel inventory flows often driven by regional seasonal planting cycles that complicated short-term demand forecasts.

These headwinds exemplify cyclical stresses endemic in agriculture input markets where producers balance output planning against volatile end-user buying patterns influenced by weather variables, crop economics, and geopolitical trade disruptions.

Segment Performance: Potash and Phosphate Contributions Reflecting Agricultural Cycles

Mosaic’s segmented disclosures clarify that potash and phosphate divisions remain core profit centers with distinct seasonal rhythms ([S1],[S5]). Potash margins benefit from integrated supply chain efficiencies yet remain sensitive to regional fertilizer application windows.

Phosphate operations face challenges from feedstock cost variability alongside shifts in regional channel stocking behaviors—factors underpinning the management of segment profitability across quarterly periods ([F1]).

This segmentation approach enables Mosaic to strategically navigate channel inventory cycles by aligning production rates with downstream demand cues while pursuing margin optimization through cost controls and product mix adjustments.

Regulatory and Operational Risks Impacting Production and Safety Compliance

Mine safety remains a focal risk area emphasized through mandatory disclosures under Dodd-Frank Section1503(a) regulations ([S4],[S6],[S7]). Mining operations integral to nutrient production bear exposure to stringent environmental standards coupled with operational continuity risks from potential violations or accidents.

Such regulatory layers impose compliance costs that can elevate operating expenses unpredictably if incidents arise or new legislation intensifies requirements—key considerations for investors assessing operational resilience within this capital-intensive sector.

Capital Structure Evolution: Debt Issuance, Liquidity, and Shareholder Returns

To reinforce liquidity amidst market uncertainties, Mosaic closed on approximately $900 million aggregate senior notes issuance across two tranches at coupons of roughly 4.35%-4.6% during late-2025 ([S12],[S13],[S14]). This move underscores proactive financing strategies aimed at extending debt maturities while preserving flexibility for corporate needs including possible debt refinancings or working capital support.

Balance sheet metrics reveal a current ratio around a healthy ~1.32 as of December-31, 2025 balancing robust current assets against liabilities ([F1]), signifying manageable near-term liquidity.

Dividend payments persisted with incremental increases ($280 million paid out in FY25 vs ~$270 million prior year), though no share buybacks occurred during the most recent fiscal period after material repurchases totaling over $235 million in FY24 were executed ([F1],[S2]). This suggests management prioritization of balance sheet strength over capital return enhancements amid ongoing cyclical volatility.

Cash Flow and Capital Expenditure: Balancing Growth Investments With Free Cash Flow Constraints

Despite operational recovery signs, operating cash flow declined notably (-37%) between fiscal years ending December-31, underscoring persistent pressures on cash conversion cycles principally due to constrained revenue growth paired with elevated working capital demands ([F1]).

Capital expenditure showed moderate growth (+9%), reflective of continued asset reinvestments imperative for sustaining mine infrastructure reliability and capacity enhancements typical of high capex intensity industries such as mining nutrients.

The resulting negative free cash flow (~$535 million deficit) signals prudence required when funding expansion initiatives amid ongoing market headwinds that delay stronger cash generation normalization.

Market Signals and Analyst Insights: Readying for Upcoming Milestones in Fertilizer Demand

Market sentiment indicators have shifted positively recently; Scotiabank’s upgrade endorses improving fundamental prospects for Mosaic amid anticipated stabilization or upticks in potash pricing ([N14]).

Simultaneously, surge activity in MOS call options expiring March-April periods indicates growing speculative positioning betting on rebounds tied closely with early-planting season volume recoveries expected post-Q1/Q2 earnings ([N7],[N9],[N11]).

Investors appear increasingly attentive to potential catalysts such as better-than-forecast shipment volumes or regulatory approvals easing constraints on output expansion plans.

What to Monitor: Volume Trajectories, Price Realizations, and Regulatory Developments

Looking ahead without speculative forecasts obligates vigilant tracking of several key signals:

- Volumes reported for Q1/Q2-2026 will illuminate whether the revenue resurgence sustains beyond late-2025 softness;

- Pricing trends for potash/phosphate commodities will critically influence margin trajectories amid inventory rebalancing;

- Regulatory filings including mine safety compliance outcomes could impact operational continuity or future cost structures;

- Corporate announcements regarding capital allocation alterations including potential resumption of share repurchases or dividend policy shifts may reflect confidence gradations;

- Global agricultural policies or trade developments affecting fertilizer demand patterns also warrant scrutiny given their pivotal role,

Maintaining awareness around these vectors ensures readiness for evolving fundamentals shaping Mosaic’s operating landscape moving forward.

This analysis integrates SEC filings, earnings transcripts, public disclosures, and market data up to February 28, 2026, presenting objective insights into Mosaic Co’s business dynamics without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments