Motorcar Parts of America: Leveraging Scale and Innovation Amid Profit Challenges

MPAA navigates a Q3 profit retreat through deep infrastructure investments and diagnostic technology expansion.

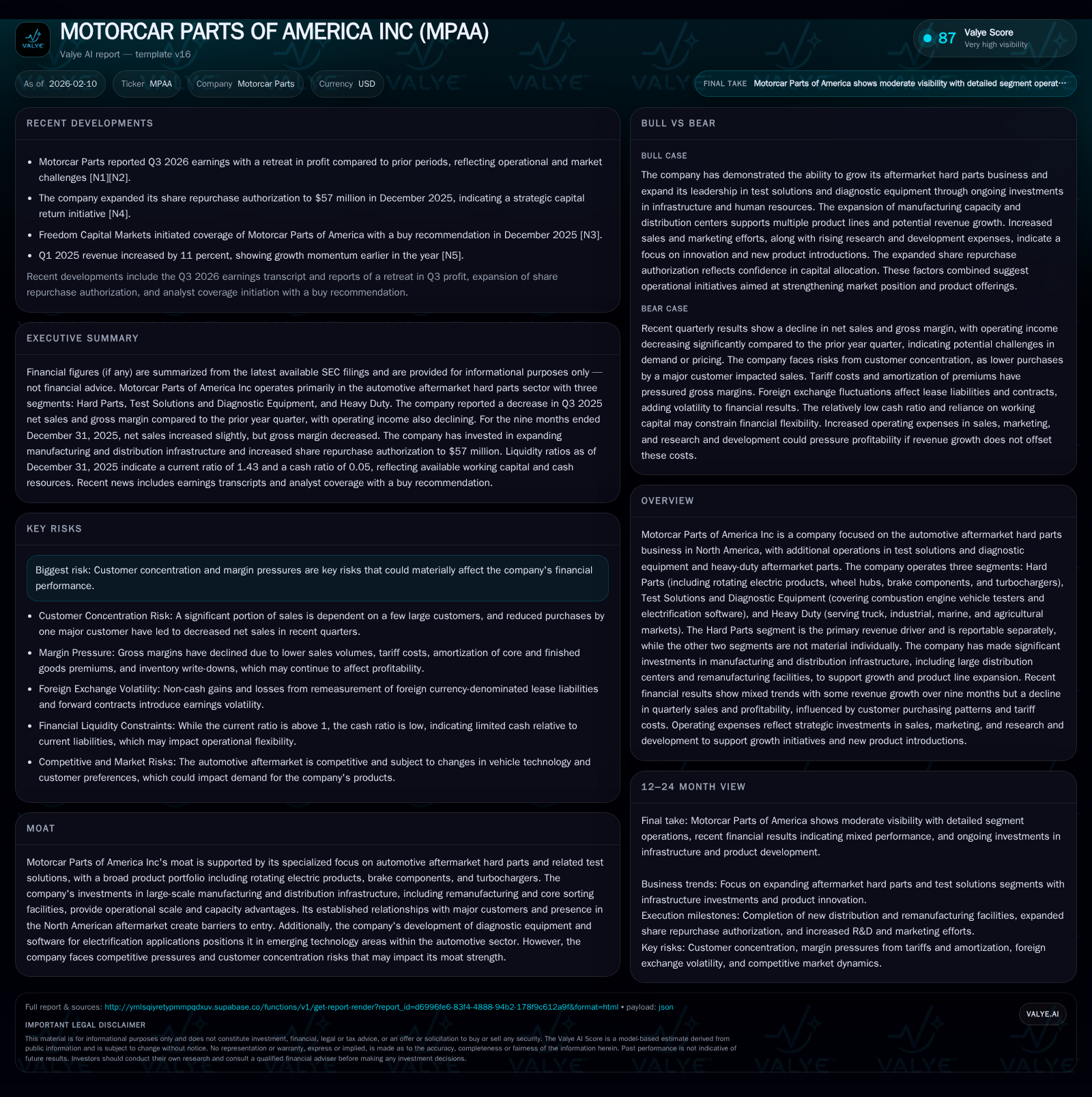

Motorcar Parts of America Inc (MPAA) recently reported a decline in quarterly profitability despite substantial investments in manufacturing and distribution infrastructure. Its Hard Parts segment remains the cornerstone of revenue, while emerging Test Solutions and Diagnostic Equipment signal strategic positioning in electrification trends. However, margin pressures and customer concentration present tangible risks to sustained financial health. This analysis explores how MPAA balances scale advantages with innovation to maintain its competitive moat amid operational headwinds.

Balancing Scale: Infrastructure Investments Fueling Core Competency

Motorcar Parts of America (MPAA) has anchored its growth strategy in substantial investments in manufacturing footprint and distribution capabilities. The company’s recent expansions include a 410,000 square foot distribution center designed to optimize product flow across North America. Complementing this are two buildings totaling 372,000 square feet dedicated to remanufacturing and core sorting brake calipers—an essential service enabling cost-effective aftermarket part supply. Additionally, production has been realigned at MPAA’s original facility in Mexico spanning 312,000 square feet.

These expansions reflect a deliberate strategy to create operational scale that supports diverse product lines while fostering cost efficiencies. The infrastructure not only bolsters capacity but enhances flexibility amid fluctuating aftermarket demand patterns across automotive sectors [S2].

Diving Into The Hard Parts Segment: Primary Revenue Engine

The Hard Parts segment stands as the backbone of MPAA’s revenue generation. This segment encompasses an extensive portfolio: light-duty rotating electric products such as alternators and starters; wheel hub products; comprehensive brake components including calipers, boosters, rotors, pads, and master cylinders; as well as turbochargers.

Segment reporting confirms its primacy within MPAA’s financial profile—the only reportable segment—underscoring how critical this diverse mix is in positioning the company within North America’s automotive aftermarket hard parts landscape [S2]. This breadth enables cushioning against volatility in any single product line while servicing a wide spectrum of vehicle repair needs.

Innovation Edge: Test Solutions and Diagnostic Equipment in an Electrifying Market

Beyond core hard parts, MPAA invests strategically in Test Solutions and Diagnostic Equipment—a unit addressing both combustion engine vehicle diagnostics and the emerging electric vehicle (EV) market. This includes benchtop testers for electrical components traditionally used in combustion vehicles as well as pre-and post-production equipment tailored for EVs.

Notably, MPAA is developing software applications that emulate power systems integral to vehicle electrification across various transport modes—automobiles, trucks, aerospace electrification systems, and charging stations. Although currently below reportable materiality thresholds, this segment represents a forward-looking thrust aimed at capitalizing on the industry-wide shift toward electrification [S2].

Heavy Duty Segment - Niche but Steady Contributions

The Heavy Duty aftermarket segment supplements MPAA’s portfolio by catering to non-discretionary replacement parts required by heavy-duty trucks, industrial machinery, marine craft, and agricultural equipment. While smaller than the Hard Parts core business, it provides steady recurring demand resistant to some economic cyclicality.

This diversification enhances resilience against automotive sector downturns by capturing incremental revenue streams from crucial support markets serving commercial transportation and equipment [S2].

Q3 Profit Retreat: Unpacking Financial Signals and Operational Challenges

Despite structural investments and segment diversity, MPAA’s recent financial disclosures reveal headwinds. Net income for Q3 ended December 31, 2025 registered $1.777 million—a decline relative to prior periods. Concomitantly, cash flow from operations swung negative by $8.229 million compared to a positive $34.357 million last year [F1][S2].

Inventory management metrics corroborate some operational strain; finished goods turnover slowed slightly from an annualized rate of 3.7 to 3.4 times over the quarter. This hints at challenges converting inventory promptly into sales revenue amid shifting demand dynamics or supply chain constraints.

These early warning signs suggest margin compression pressures or elevated operating costs are tempering bottom-line results even as strategic investments continue unfolding [N1][N2].

Evaluating Risks: Customer Concentration and Margin Pressures

Management disclosures highlight customer concentration as a salient risk—dependency on relatively few large customers may impair negotiating leverage over pricing or disrupt revenues if contracts fluctuate unexpectedly [S2].

Margin pressures compound this vulnerability; competitive bidding in aftermarket parts along with raw material cost fluctuations tighten profitability corridors. These risks require vigilant cost control measures and diversification efforts to mitigate potential adverse impacts on financial stability.

Such challenges emphasize the importance of maintaining broad customer relationships while innovating product offerings to justify pricing premiums where possible.

Assessing the Moat: Competitive Position and Market Barriers

MPAA’s moat rests on several pillars: specialized expertise in automotive aftermarket hard parts combined with expansive manufacturing and distribution infrastructure create high barriers for new entrants seeking scale parity.

Long-standing relationships with major North American customers entrench the company within established supply chains. Moreover, early engagement with electrification diagnostics positions MPAA ahead of peers still focusing solely on traditional combustion engine components.

Nonetheless, the moat is not impervious; concentrated customer bases introduce revenue volatility risks while growing competition from broader aftermarket suppliers demands continual efficiency gains and innovation investment [valye_report_excerpt].

Outlook & Strategic Priorities Moving Forward

Post-Q3 profit contraction puts renewed emphasis on extracting returns from existing infrastructure investments—a challenge management acknowledges openly. Efforts to optimize capacity utilization within their expansive facilities remain critical alongside streamlining inventory turnover.

Simultaneously, expanding Test Solutions’ footprint aligns with long-term growth imperatives tied to vehicle electrification trends. The diagnostic software pipeline exemplifies this innovation thrust aiming to future-proof MPAA’s relevance across emerging transport technologies.

Margin improvement initiatives will likely accompany intensified focus on customer diversification to soften concentration risk exposure going forward. In sum, MPAA appears committed to balancing solidifying its Hard Parts foundation with calculated bets on high-potential diagnostic segments—an approach reflecting pragmatic adaptation amid evolving market realities [N1][S2][valye_report_excerpt].

This analysis synthesizes publicly available information without issuing investment advice or recommendations. It aims solely to provide an informed perspective on Motorcar Parts of America Inc's operational strategies, financial developments, risk factors, and competitive positioning within their industry context as of early 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments