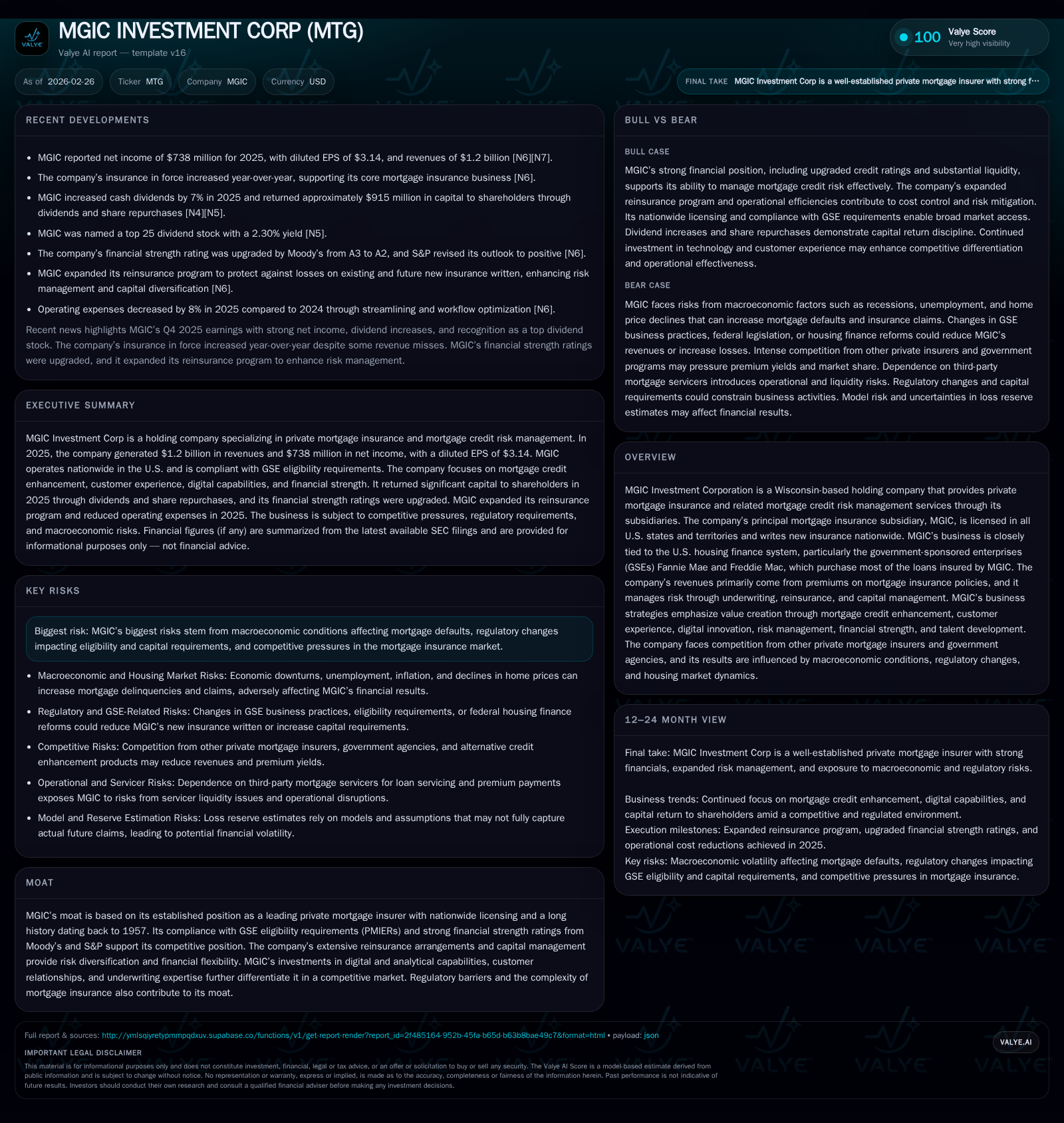

MGIC Investment Corp Delivers Resilient Profitability Amid Shifting Mortgage Dynamics

MGIC balances disciplined capital management and risk diversification to sustain profits despite market headwinds.

MGIC Investment Corporation, a pioneer in private mortgage insurance since 1957, demonstrated durable net income of $738 million in 2025 amid a moderation in insurance premium yields and evolving mortgage market conditions. The company navigated slowing home price appreciation and regulatory complexity by advancing its reinsurance strategy, streamlining underwriting expenses, and investing in digital technologies to maintain competitive differentiation. MGIC returned significant capital to shareholders via a 14% dividend increase and repurchased 12% of shares outstanding, underscoring strong cash flow generation. Looking ahead, close monitoring of GSE policies, regulatory capital requirements, and housing finance reforms remains essential as MGIC adapts its risk framework and growth initiatives.

Historic Financial Performance: Profitability with Operational Efficiency

MGIC Investment Corporation sustained profitable operations through 2025 despite external pressures on revenue growth. Total revenues approached $1.2 billion while net income stood at $738 million, a modest decrease from the prior year's $763 million [S1]. This decline primarily resulted from lower premium yields driven by runoff of older policies with higher rates and prevailing slower home price appreciation, as reflected in the Federal Housing Finance Agency's (FHFA) index rising only 1.4% for most of 2025 compared to stronger prior periods [S1].

Operationally, MGIC mitigated margin pressure by reducing underwriting and related expenses by approximately 8%, achieved through streamlining processes and workflow optimization [S1]. Complementary to efficiency gains, the company repurchased about 12% of its outstanding shares during the year, reinforcing capital discipline during revenue headwinds [S1]. As of December 31, 2025, MGIC reported direct primary insurance in force (IIF) totaling $303.1 billion and new insurance written (NIW) of $60.2 billion [S1], underscoring its broad national footprint.

| Fiscal Year | Revenue ($M) | Net Income ($M) | Underwriting Expenses Change YoY (%) | Cash Dividends Paid ($M) | Shares Repurchased (% out.) |

|---|---|---|---|---|---|

| 2024 | ~1,200 | 763 | 750 | ||

| 2025 | ~1,200 | 738 | -8% | 800 | 12% |

Note: Revenue is approximately $1.2 billion for both years based on disclosed figures [S1].

Mortgage Insurance Market and Regulatory Environment Impacting MGIC

The mortgage insurance industry is tightly linked to the U.S. housing finance system dominated by government-sponsored enterprises (GSEs), principally Fannie Mae and Freddie Mac [S1]. Approximately all of MGIC’s NIW involves loans purchased by these GSEs, making their business practices pivotal. Regulatory frameworks such as the GSEs’ Private Mortgage Insurer Eligibility Requirements (PMIERs) impose rigorous capital and risk management standards that MGIC currently satisfies while maintaining eligible status [S1]. Compliance supports investor confidence but requires significant capital allocation which can compress returns if requirements tighten [S1][S24].

Housing market dynamics exert cyclical influence on MGIC's risk exposure and earnings potential. After several years of elevated home price appreciation driving loan origination volume and favorable credit quality trends, the FHFA Purchase-Only Home Price Index slowed to around +1.4% through late 2025 from nearly +6.7% in early post-pandemic years [S1]. This deceleration exacerbates affordability challenges as price-to-income ratios exceed historical benchmarks, potentially dampening future NIW.

Additionally, competitive pressures have intensified with certain rivals leveraging off-shore reinsurance vehicles that afford tax advantages unavailable to MGIC’s U.S.-domiciled operations [S5]. This structural discrepancy may allow competitors to offer lower premiums or alternative credit enhancement solutions undercutting market share.

Regulatory scrutiny extends beyond PMIERs into state-level capital regimes as well as evolving compliance expectations regarding data privacy, underwriting fairness (including algorithmic bias considerations), and cybersecurity controls [S6][S15][S20]. Regulatory actions or unfavorable legislative reforms could constrain growth or affect profitability.

Advancing Growth: Business Strategy Execution and Competitive Positioning

MGIC has accelerated initiatives to sharpen its competitive edge through technology investments and enhanced risk management execution. A pivotal move in 2025 included retirement of legacy data platforms coupled with establishing a modern MI operations environment designed to facilitate advanced analytics deployment such as artificial intelligence (AI) models for underwriting refinement [S1][S5]. This digital transformation aims not only at improving credit decision accuracy but also at enriching customer experience—a vital differentiator given heightened borrower expectations.

Reinsurance remains central to MGIC's risk diversification approach. In 2025, the company expanded its reinsurance program via new transactions supporting both existing portfolio losses and anticipated new insurance flows. Additionally, renegotiation of seasoned reinsurance deals enabled recapturing attractive risk segments while reducing ceded premium costs [S1]. These flexible programs underpin capital efficiency without compromising loss protection.

Operational streamlining efforts contributed meaningfully to an 8% decline in underwriting expenses versus the previous year while maintaining underwriting discipline aligned with PMIERs standards [S1]. Maintaining balance between profitability targets and market share ambitions continues as underwriting remains a key lever amid uncertain volume outlooks.

Capital Deployment: Shareholder Returns, Dividends, and Buybacks

MGIC’s capital allocation embodies a disciplined philosophy focused on sustaining liquidity while delivering shareholder value. The company returned roughly $915 million in combined dividends and share repurchases during calendar year 2025 [S24]. Specifically, dividends increased by approximately 14% year-over-year to $0.56 per diluted share from $0.49 previously—totaling around $800 million paid from the operating subsidiary MGIC to the holding company [N10][N11][S24]. Concurrently, the firm repurchased about 12% of shares outstanding early in the year supporting EPS accretion despite modest net income decline [S1][N11].

Cash and investments at the holding company remained robust at approximately $1.1 billion at year-end [S24], providing a buffer against regulatory or market disruptions impacting dividend capacity or buyback flexibility.

While explicit return on equity figures were not disclosed across multiple sources, strong operating cash flow generation evident from stable dividend coverage suggests healthy underlying financial performance consistent with investment-grade rating upgrades assigned by Moody’s (from A3 to A2) and positive outlook revisions by S&P during the period [S24][S1].

Risk Management Framework: Navigating Credit Exposure and Reinsurance

MGIC’s foundational business model revolves around prudent mortgage credit enhancement balanced against comprehensive risk mitigation techniques aligned with PMIERs mandates [S6][S23]. Underwriting adheres strictly to rule-based models incorporating multiple borrower attributes including loan-to-value ratios (LTV), credit scores, debt-to-income ratios (DTI), loan vintage characteristics, and delinquency history—factors systematically assessed using proprietary algorithms continually recalibrated against emerging data patterns [S21][S23].

The insurer complements direct risk retention with layered reinsurance agreements that dilute tail loss exposures thereby smoothing claims volatility across economic cycles [S5]. While this strategy effectively conserves statutory capital usage enabling competitive premium offerings within regulatory constraints, it introduces counterparty concentration considerations especially given that MGIC's top ten customers accounted for over one-third of NIW—largest client alone ~16% in 2025—implying dependency risks if these relationships alter materially [S5].

Cybersecurity risks also pose growing challenges given extensive sensitive personal information processing integral to mortgage insurance operations; MGIC maintains robust defenses yet recognizes inherent vulnerabilities compounded by increasing AI-enabled cyberattack sophistication requiring ongoing vigilance [S15][S22].

Digital Transformation and Customer Experience Initiatives

Advanced technological adaptation underpins MGIC’s forward-looking growth imperatives. The complete decommissioning of legacy data platforms has established an infrastructure foundation capable of integrating AI/ML applications aimed at refining underwriting analytics accuracy leading to better risk segmentation and pricing precision—a crucial advantage within an increasingly commoditized mortgage insurance marketplace [S5][S1].

Customer engagement enhancements are also priorities consistent with broader industry recognition that digital fluency directly correlates with customer retention rates and willingness among lenders to commit volumes under competitive pricing scenarios where service quality plays an outsized role beyond pure cost considerations.

These digital innovations collectively support strategic differentiation by enabling faster decision-making processes coupled with granular portfolio monitoring facilitating proactive risk interventions before claim triggers escalate.

Key Takeaways and Forward-looking Considerations

MGIC Investment Corporation remains well-positioned within the incumbent cohort of private mortgage insurers leveraging decades-long institutional knowledge backed by scale licensing across all U.S jurisdictions plus territories including Puerto Rico and Guam [S1]. Its resilient profitability amidst softening premium environments signals effective margin management balancing expense control alongside risk transfer mechanisms.

However, notable headwinds include macroeconomic cyclical shifts influencing loan default probabilities such as potential recessionary pressures or regional economic disparities affecting borrower repayment behavior peculiarities. Further complicating outlook are possible GSE reform trajectories along with evolving PMIERs interpretations impacting capital cost structures thus shaping product offerings competitive viability over time.

Key metrics deserving investor scrutiny include quarterly updates on NIW volumes reflecting originations momentum amidst fluctuating interest rate climates; regulatory developments pertaining specifically to eligibility standards or newly adopted state level Model Act implementations; claims frequency trends influenced by housing affordability stresses; alongside continued progress toward full realization of AI-driven operating platform benefits.

In aggregate, MGIC’s integrated approach combining financial strength enhancement via selective reinsurance expansions; disciplined underwriting configured through technology upgrades; customer-centric product delivery improvements; supported by shareholder-focused return policies constitutes a comprehensive playbook navigating complex mortgage dynamics ahead.

This analysis is intended for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments