Net Lease Office Properties Trims Portfolio to Sharpen Focus on Domestic Net-Lease Office Assets

After spinning off from W. P. Carey in late 2023, NLOP has reshaped its portfolio amidst market headwinds and maintained operational stability through strategic disposals and strong cash flows.

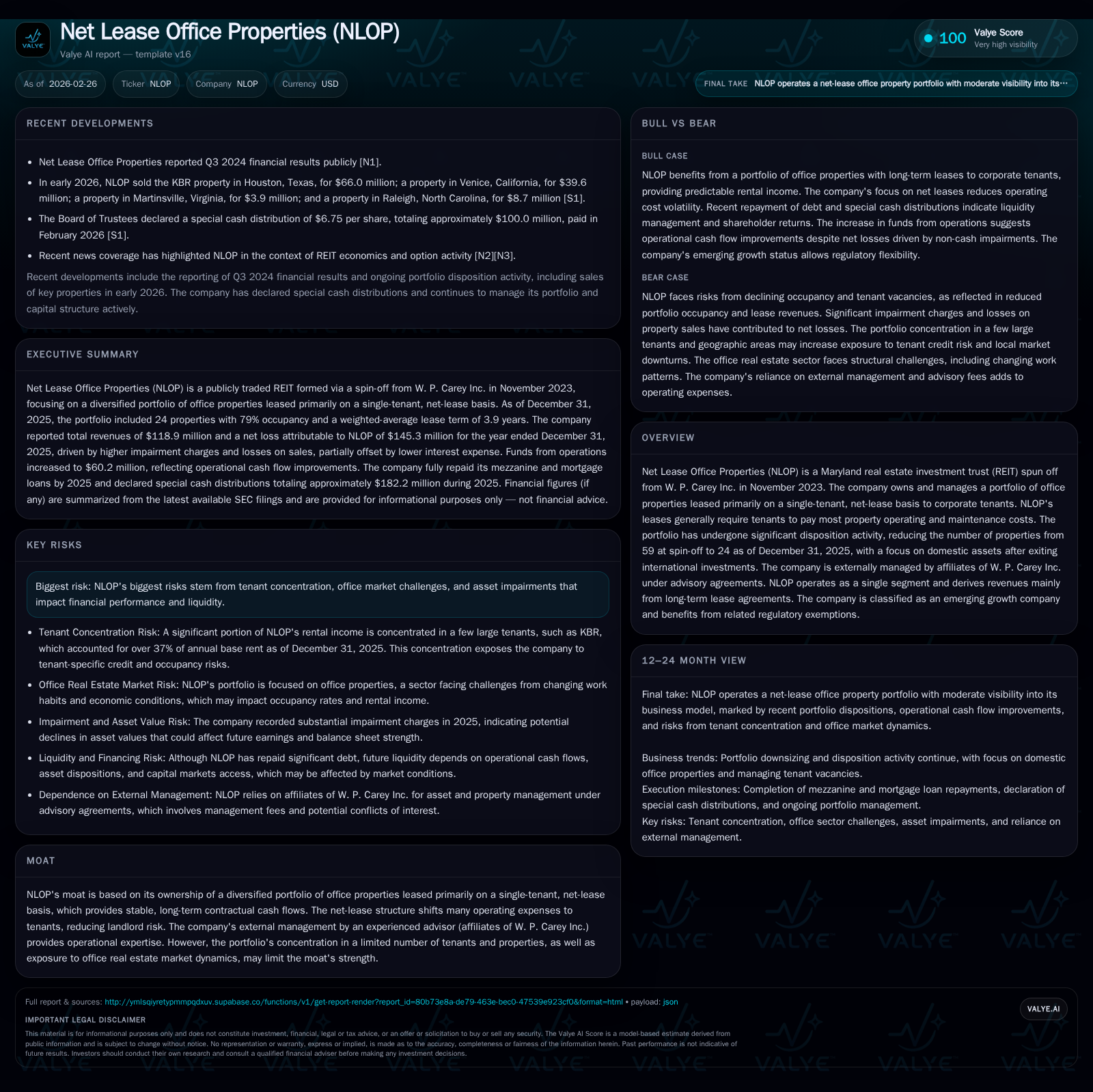

Net Lease Office Properties (NLOP) emerged from W. P. Carey Inc. in November 2023 with a focus on single-tenant net-leased office properties largely in the U.S. Since inception, it has significantly reduced its property count from 59 to 24 by shedding international holdings and non-core assets, concentrating on domestic office investments. This repositioning coincides with challenging office market dynamics and tenant concentration risks, particularly with KBR representing nearly a third of lease revenues in 2025. Despite declining revenues and continued net losses, NLOP sustains positive operating cash flow and substantial liquidity, supported by proactive debt reduction and a sizeable special cash distribution to shareholders in early 2026.

Company Overview and History

Net Lease Office Properties (NLOP) launched as an independent Maryland REIT following its spin-off from W. P. Carey Inc. in November 2023 [S1]. The company owns a diversified portfolio of office buildings leased predominantly on single-tenant net-lease agreements to corporate tenants. Under these leases, tenants bear most operating expenses, effectively reducing landlord risk [S1]. At spin-off, the portfolio consisted of 59 properties including international assets located in Norway, Poland, and the UK, which have since been divested [S10].

The entity operates under external management via advisory agreements with affiliates of W. P. Carey Inc., retaining access to seasoned real estate operational expertise while functioning as a single business segment focused on net-leased office real estate [S1,S10]. As an "emerging growth company," NLOP benefits from scaled reporting requirements under the JOBS Act through at least late 2028 [S1].

Historical Performance and Portfolio Transformation

Since inception, NLOP has aggressively reshaped its asset base to concentrate on core U.S.-domiciled office properties. By December 31, 2025, the property count fell to 24 from the original 59 at spin-out, driven primarily by the disposition of all international holdings—complete exits from Norway and Poland during 2025 and the UK during 2024—as well as domestic asset sales focusing the portfolio [S10,S19]. These high-value sales generated significant proceeds enabling debt reduction and liquidity enhancement.

Financially, annual revenues have contracted markedly following the spin-off due to these dispositions coupled with market demand pressures for office space: revenues declined roughly -16% year-over-year to $119 million in FY2025 from $142 million in FY2024 and $175 million in FY2023 [F1]. This trend mirrors ongoing challenges faced across U.S. office real estate amid hybrid work adoption.

Despite revenue pressures, net losses widened substantially: FY2025 net loss reached $145 million versus $91 million in FY2024—exacerbated by impairment charges on certain assets, notably international properties prior to sale—and elevated non-cash expenses [F1,S1,S26]. Operating cash flow remained positive but slightly reduced at $64 million for FY2025 down from $72 million a year prior [F1], underscoring the portfolio’s steady baseline cash generative profile supported by lease structures.

Selected Key Financials:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 119 | -145 | 64 | -16.4% | -58.8% | |

| 2024 | 142 | -91 | 72 | 3 | -18.7% | +30.6% |

| 2023 | 175 | -132 | 71 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 61 | -49.4 | |

| 2024 | 1 | 69 | -15.7 |

| 2023 | 1 | 69 | -19.5 |

Source: SEC companyfacts cache [F1].

Table reflects consolidated financial data highlighting shrinking revenues alongside escalating net losses but stable operating cash flows.

Capital Structure and Liquidity

NLOP entered the public markets leveraging significant financing arrangements established concurrent with spin-off comprising a $335 million senior secured mortgage loan (NLOP Mortgage Loan) maturing November 2025 plus two one-year extension options and a $120 million mezzanine loan facility maturing November 2028 [S6,S10,S12]. Using sales proceeds and operating cash flow during FY2024-FY2025 periods, NLOP fully repaid its mortgage loan by end-2024 and completely retired the mezzanine loan by April 2025 ($61 million outstanding as of December '24) [S4,S6,S16]. Consequently total debt declined from about $169 million at end-2024 to approximately $22 million non-recourse fixed-rate mortgages outstanding at December 31, 2025 with weighted average interest rate easing to roughly 7% [S6,S20]. Variable rate debt was fully retired.

Liquidity strengthened substantially with cash and equivalents rising from approximately $25 million at end-December 2024 to over $119 million as of December 31, 2025 post-dispositions [F1,S6]. Unleveraged property assets remain valued around $277 million at year-end providing additional financial flexibility though conversion risk persists given office sector conditions [S6]. Scheduled debt principal payments are manageable: only about $22 million non-recourse mortgage repayments fall due during calendar year 2026 with limited longer-term maturities stated [S20].

Interest expense plummeted by over $55 million year-over-year reflecting debt reductions while other gains/losses fluctuated modestly including non-cash allowances for credit losses tied to finance leases [S16]. NLOP's effective hedging strategy includes an interest rate cap expiring November 2025 which limits variable rate exposure; however that derivative is no longer designated for hedge accounting due to paid-off borrowings [S12,S13].

Dividend Policy and Capital Returns

NLOP initiated larger dividend distributions aligned with cash flows generated post-spin-off [F1,S19]. Dividends paid surged dramatically from just over $1 million annually pre-spin-off to nearly $61 million during FY2025 reflecting both increased payout ratios relative to AFFO/FFO metrics common within REITs as well as a special cash distribution declared January 2026 totaling approximately $100 million or about $6.75 per share [S19,N1]. This sizable payout was funded partly by liquidation proceeds including the sale of major tenant KBR's Houston property sold early in calendar year '26 after representing close to one-third of total lease revenue at end-December '25.

This policy indicates management’s effort to return excess capital amidst portfolio rebalancing while maintaining adequate liquidity buffers. No buybacks or repurchase programs were noted.

Tenant Concentration & Portfolio Risks

Tenant diversity is a material concern with KBR historically constituting around one-fifth to nearly one-third of lease revenues from CY23 through CY25—29.5% in FY25 alone—and representing over twenty percent of long-lived asset value during that period [S10]. Given KBR's sale of its key property post-year-end (January '26), this concentration risk may abate but will require monitoring given potential impacts on income stability.

Market conditions for office leasing remain subdued broadly across U.S. markets with ongoing structural questions regarding demand levels post-pandemic affecting rent growth prospects across net lease portfolios generally—a challenge compounded for occupants seeking flexible solutions rather than long-term net leases.

Moreover asset impairments remain significant; impairment charges exceeded $140 million for real estate assets during FY25 alone related mainly to write-downs on certain international properties prior to their sale but also reflecting persistent valuation pressures domestically [S26]. Environmental compliance costs appear manageable without material contingencies currently flagged [S11,S14].

Governance & Management Framework

While wholly externally managed by W.P Carey affiliates providing strategic guidance continuity since spin-off [S1], this governance model introduces potential agency considerations around capital allocation discretion especially concerning asset sales pace and dividend policy balancing liquidity needs.

Forward-Looking Considerations

Although explicit earnings guidance or forward forecasts are not provided formally within filings or news releases up to February '26 [N1], critical developments to track include:

- Execution speed on further dispositions supporting debt repayment or potential reinvestment into higher-yielding offices;

- Lease renewals and tenant credit trends amid macroeconomic headwinds affecting corporate occupiers;

- Interest rate environment evolution impacting potential refinancing costs beyond current maturity horizons;

- Regulatory changes under new tax legislation affecting REIT status benefits starting mid-2025 [S1];

- Impact of shareholder distributions on retained capital for growth opportunities versus yield preservation.

Monitoring these factors will frame NLOP’s trajectory carefully over remaining years within its emerging growth company window.

Summary

NLOP represents a refined real estate investment trust focused narrowly on domestic single-tenant net-leased office properties following an active disposition agenda subsequent to its late-2023 independence from W.P Carey Inc. It faces clear top-line pressure from asset sales compounded by difficult office leasing market fundamentals yet maintains steady positive operating cash flows indicative of strong lease contracts underwriting stable income streams. Significant deleveraging achieved via full repayment of major credit facilities has enhanced liquidity posture considerably headed into calendar year ‘26. Tenant concentration risks centered primarily around KBR paint a nuanced backdrop given their disproportionate contribution vis-à-vis overall revenue; recent property divestitures may mitigate this dynamic. Capital returns via dividends have risen meaningfully during this phase suggesting confidence in free cash generation albeit balanced against limiting future reinvestment capacity amid modest portfolio scale remaining. Given these factors alongside regulatory changes effective July ‘25 impacting tax treatment and REIT qualification thresholds alongside macroeconomic uncertainties influencing leasing activity—a cautious optimism grounded in prudent financial management appears characteristic of NLOP’s current positioning.

This analysis is based solely on publicly available SEC filings ([F1],[S#]), news releases ([N#]), and expert sector context without providing investment advice or forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments