Anbio Biotechnology’s Revenue Stabilization and Margin Expansion After IPO and COVID-19 Pivot

Post-IPO, Anbio Biotechnology leverages product diversification and cost control to sustain growth while managing operational cash flow challenges.

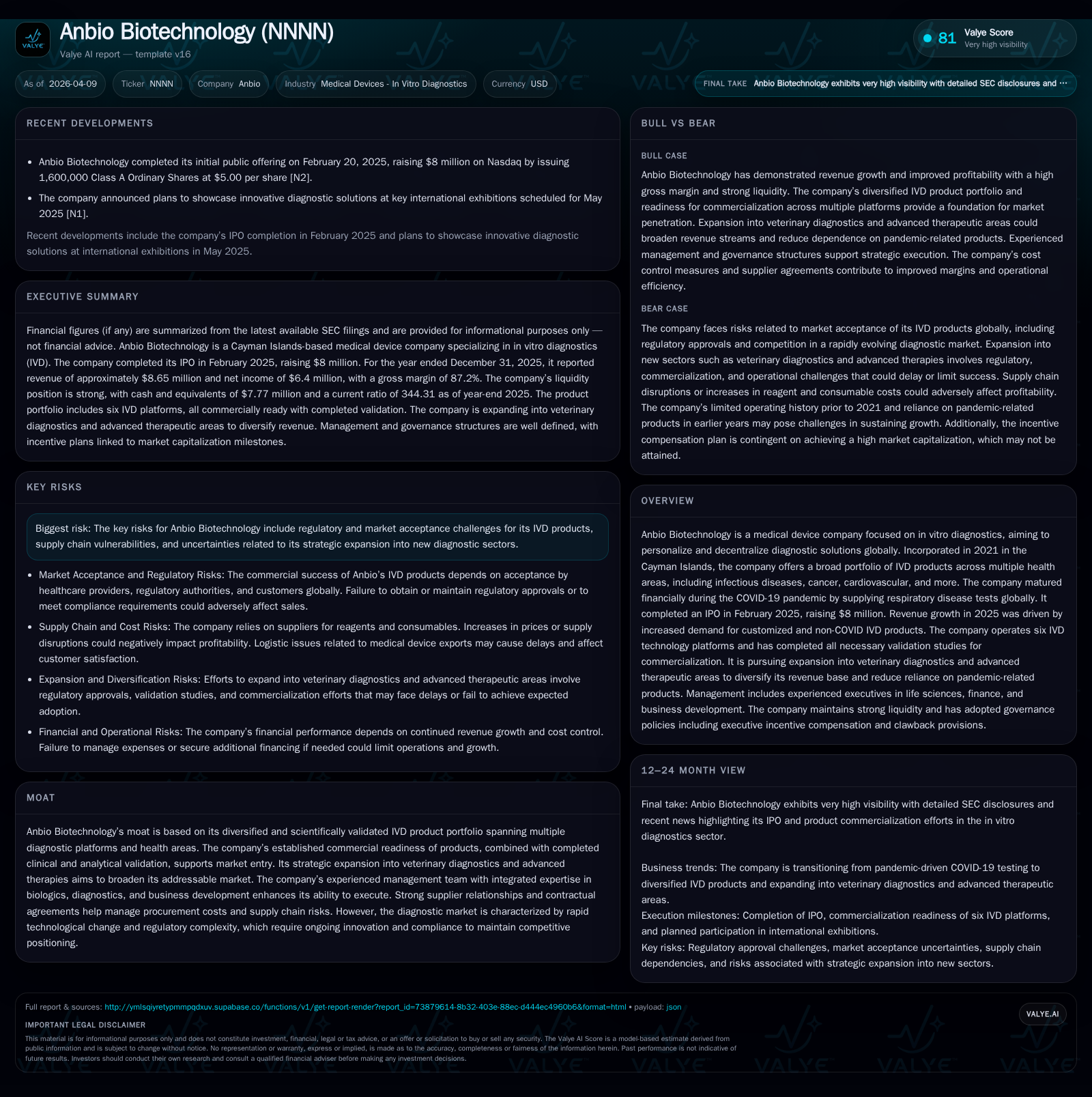

Anbio Biotechnology, a Cayman Islands-incorporated medical device company specializing in in vitro diagnostics (IVD), demonstrated strong financial growth during 2023–2025, capitalizing initially on COVID-19 respiratory tests. Revenue increased modestly by 5.6% from 2024 to 2025 to about $8.65 million, driven primarily by growing demand for customized and non-COVID IVD products. The company achieved a significant gross margin expansion to over 87% in 2025 through cost optimization and shifting product mix. Despite net income soaring nearly 170%, operating cash flow turned negative in 2025 due to working capital investments. The business plans to expand into veterinary diagnostics and advanced therapeutic areas to diversify revenue, while prudently managing capital allocation with no dividend payments foreseen. Key risks include regulatory hurdles and supply chain dependencies in a competitive and fast-evolving diagnostic market.

Company Overview

Founded in mid-2021 and headquartered legally in the Cayman Islands with operational centers in Germany among others, Anbio Biotechnology positions itself as a global player aiming to personalize and decentralize diagnostics via innovative in vitro diagnostic (IVD) solutions [S1]. The company offers a diverse product portfolio that extends beyond its initial focus on COVID-19 respiratory tests during the pandemic years — including assays for infectious diseases, cancer markers, cardiovascular conditions, endocrine disorders, pharmacogenomics, and more.

Historical Growth and Financial Performance

Anbio's financial trajectory reflects its transition from pandemic-driven revenues to a diversified IVD product revenue base:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | 6 | -7 | 6 | +5.6% | +169.9% |

| 2024 | 8 | 2 | 2 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 21.2 |

| 2024 | 13.8 |

Source: SEC companyfacts cache [F1].

(Data sourced from SEC filings [F1], [S4])

Revenue grew impressively by about 22% from 2023 to 2024 as Anbio expanded its non-COVID product lines and broadened its customer base across global regions. However, growth moderated to approximately 5.6% year-over-year into 2025 as the market normalized post-pandemic.

The gross margin improvement is notable; rising from approximately half of revenue in early years to sustaining nearly an additional third margin gain by late-2025. This was driven largely by shifts towards higher-margin customized tests and efficient procurement arrangements including bulk supplier contracts [S4].

Operating income tripled between FY24 and FY25 due not only to margin expansion but also significantly reduced operating expenses following the IPO year peaks related to listing costs: SG&A dropped over half year-over-year while R&D spending fell as product pipelines matured [S7].

Net income increased substantially between FY24 and FY25 providing an estimated return on equity around the low twenties percentage-wise by end of FY25 ([F1]: net income of $6.4M against equity of ~$30M). Yet operating cash flow reversed sharply negative in FY25 due primarily to working capital movements including large increases in accounts receivable ($2.6M) and prepayments ($8.4M), illustrating capital invested ahead of sales [S6], [S21].

Strategic Shifts and Future Growth Drivers

The company completed an IPO on Nasdaq Global Market in February of 2025 raising $8 million gross proceeds that are intended mainly for scaling non-COVID diagnostics commercialization efforts globally [S1]. This enabled Anbio not only to continue distributing its established respiratory disease tests internationally but also begin diversification into veterinary diagnostics as well as advanced therapeutics related IVD products.

Expansion plans emphasize leveraging the six validated technology platforms already commercial-ready after extensive clinical validation studies [S1]. Emphasis on decentralized testing at point-of-care alongside at-home wellness offerings aligns with broader industry trends favoring rapid personalized diagnosis outside traditional centralized labs.

Key internal growth drivers include:

- Broadening geographic reach particularly targeting high-opportunity regions where personalized diagnostic penetration remains low.

- Increasing customized testing services where premium pricing supports better margins.

- Expansion into veterinary sectors which represent a less competitive niche with sizable IVD testing needs.

However these prospects carry certain headwinds:

- Regulatory approval pathways globally remain complex; delays or failure to secure or maintain certifications could restrict market entry.

- The fast-moving technology landscape demands continuous innovation lest existing platforms become obsolete versus competitors deploying next-generation molecular or digital diagnostics.

- Supply chain resilience is critical given previous pandemic disruptions; Anbio’s ability to maintain supplier relationships underpins production capacity planning [S16].

Capital Allocation and Returns

Since going public the company has prioritized reinvestment over distributions:

- No dividends have been declared or expected imminently; board discretion remains broad with dividends paid only if profitable surplus allows without jeopardizing solvency under Cayman Islands law [S12], [S16].

- Share repurchases have not been reported since listing; the dual-class share structure grants Class B shares concentrated voting power but no economic rights complicating alignment incentives somewhat [S14], [S15].

- IPO proceeds alongside operational cash flows fund working capital needs; however negative operating cash flow in FY25 signals cash management risks especially if sales cycles lengthen or receivables delay collections.

Operational Highlights: Cost Structure & Margins

Cost of goods sold (COGS) dropped markedly—from over $3.3 million in FY23 down near $1.1 million last fiscal—reflecting stringent product/customer vetting focusing narrowly on higher-margin segments [S4]. Procurement agreements negotiated during prior years likely contributed bulk discount benefits that sustained improved gross margins even amid modest revenue uptick. Selling & general administrative expenses showed a steep decline after a peak related to IPO preparation activities: down more than half from $3.4M (FY24) to under $1.6M (FY25). Control of discretionary spending combined with enhanced operational discipline contributed materially here. R&D spend likewise tapered substantially (~$200k FY25 vs $450k FY24) consistent with a portfolio pivot from development-heavy early stage products toward marketing validated commercial assays while ensuring compliance support across different jurisdictions’ regulations. Interest income declined mostly due to realized losses on equity securities despite continued bank deposit yields indicating some volatility around ancillary investment returns [S7], [S18].

Governance & Risk Management

Recent governance updates included director replacements enhancing financial oversight capabilities; notably appointing an audit committee chair with extensive finance experience effective January-February 2026—a positive step for transparency at this growth stage [S3]. Anbio maintains a cybersecurity risk management framework aligned with industry standards protecting proprietary data integral for applying advanced biotech analytics underpinning assay reliability. Risks comprehensively disclosed pertain mostly to regulatory approvals uncertainty globally; potential supply chain bottlenecks amidst geopolitical tensions; pricing pressures from competitive innovation; potential obsolescence if technology enhancements aren’t timely incorporated; plus currency exposure management tied mainly between USD/EUR remittances though currently minimal derivative usage is reported [S16], [S19].

What To Watch Forward (analysis)

- Quarterly/annual revenue composition shifts—monitor balance between COVID legacy products vs customized IVD offerings plus progress in veterinary diagnostics rollout.

- Working capital efficiency—especially receivable days management impacting liquidity given recent operating cash outflows.

- Regulatory newsflow on approvals or rejections across key markets influencing near-term growth potential.

- Capex intensity—whether expanding manufacturing infrastructure or tech platform upgrades signal scaling approach.

- Any changes regarding dividends or share buybacks hinting at evolving shareholder return policies post-growth phase.

Conclusion

Anbio Biotechnology’s journey from a pandemic-response specialist toward a multifaceted IVD player appears financially disciplined with strong margin improvement validating strategy execution post IPO infusion of capital. Still early-stage cash flow dynamics require careful monitoring amid ambitious expansion plans underpinned by regulatory complexity inherent to global diagnostic markets. Stakeholders should weigh robust profitability gains against capital deployment cadence reflecting continuing transformation toward sustainable long-term growth.

This analysis is based exclusively on publicly filed company financials and disclosures up through April 9th, 2026 without inclusion of unverified third-party information or forward-looking investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments