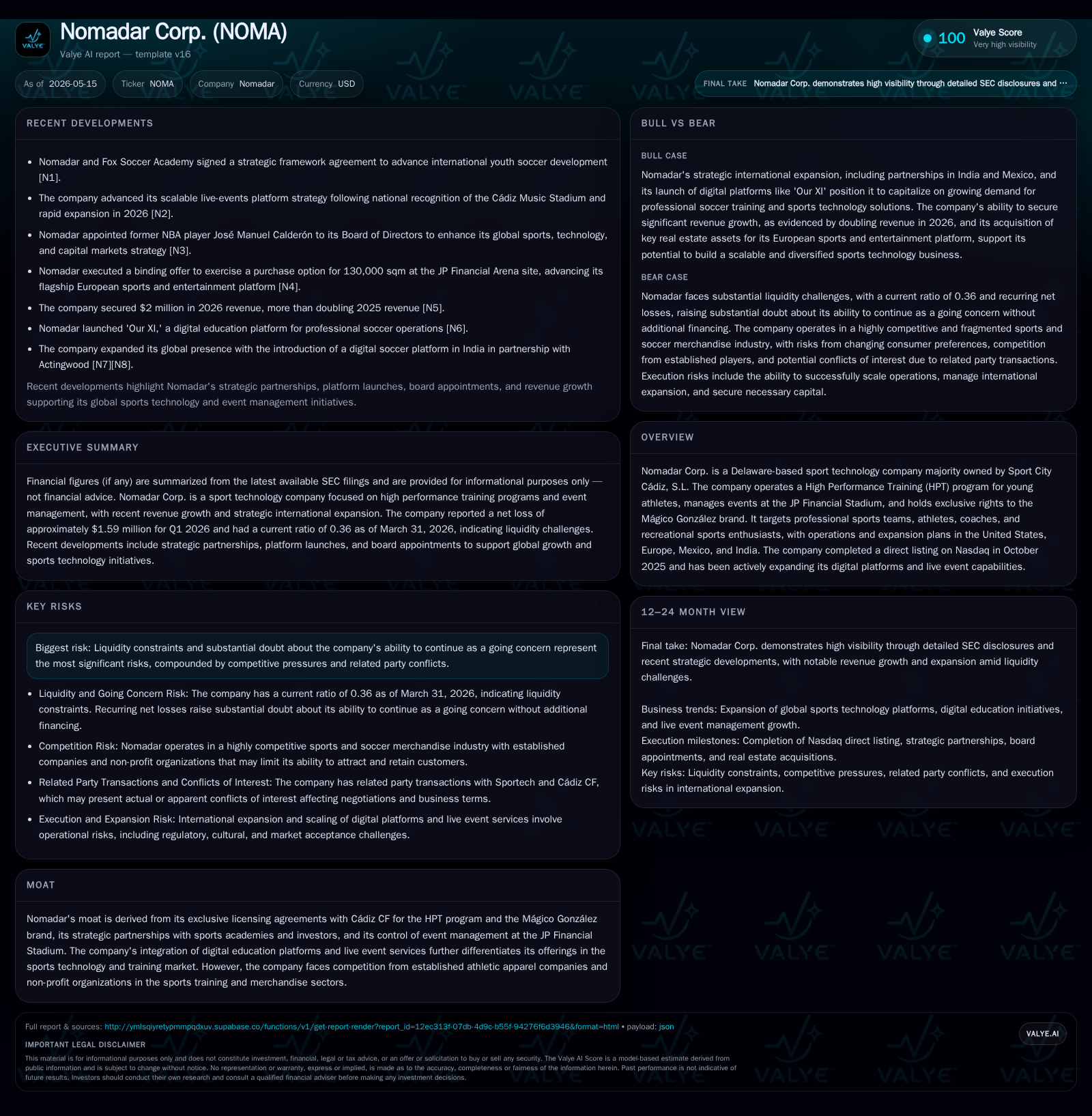

Nomadar Corp.'s Expansion Hinges on Licensing Moat and Liquidity Amid Operational Losses

Nomadar reports Q1 2026 operating updates emphasizing exclusive rights, event management expansion, and liquidity pressures.

Nomadar Corp. operates a niche high performance sports training program leveraging exclusive licenses with Cádiz CF and event management at JP Financial Stadium. The latest quarterly filing confirms continued revenue generation alongside significant net losses and liquidity constraints. The company is expanding globally through strategic partnerships and live event capabilities but faces risks from capital needs and competitive pressures. Monitoring its financing initiatives and execution on digital sports platforms will be key to evaluating progress.

Recent Operating Update: Q1 2026 Highlights

The latest quarterly report filed May 15, 2026 [S2] provides the most current operational snapshot for Nomadar Corp., emphasizing revenue continuity from its High Performance Training (HPT) program and event management services at the JP Financial Stadium. Despite generating some revenue streams, substantial net losses persist — with net loss exceeding $2.7 million as of the fiscal year-end December 2025 [F1], reflecting high operating costs, including professional fees exceeding $2.7 million [S12]. The operational update signals ongoing efforts to scale while managing cost structure.

Liquidity metrics remain strained with a current ratio of just approximately 0.36 as of March 31, 2026 [F1], underscoring working capital deficits driven by outsized current liabilities relative to assets. While no new explicit disclosure on debt or leverage was reported in the latest quarter or event filings, historical figures suggest total debt under $500,000 as of end-2024 [F1], implying nominal leverage relative to current liabilities but highlighting cash flow pressures.

Recent capital infusion actions demonstrate material reliance on external funding: Sport City Cádiz has contributed over $1.9 million in early 2026 via stock issuance [S12], supplemented by a $5.4 million strategic investment secured from an international investor announced in March 2026 [S21]. These steps explicitly address the substantial doubt management has flagged regarding Nomadar’s ability to continue as a going concern without continued funding [S9].

The board was strengthened by the April appointment of former NBA player José Manuel Calderón as director [S3,N3], bringing professional sports experience aligned with Nomadar’s strategic focus on global sports technology expansion.

Business Model

Nomadar’s business is centered on three core pillars:

High Performance Training Program (HPT): Leveraging exclusive license agreements with Cádiz CF, Nomadar offers athlete development programs aimed at young participants targeting elite soccer integration internationally. This program constitutes a commercialized intellectual property sublicensing model where revenue is recognized over time as rights to use the Mágico González brand are granted to sublicensees [S1].

Event Management at JP Financial Stadium: The company holds exclusive rights to manage live events at this multi-purpose venue. Monetization derives from ticketing, sponsorships (e.g., naming rights licensed to JP Financial), and associated event services [S24].

Digital Sports Education Platforms: Complementing physical training centers, Nomadar is actively expanding digital platforms offering educational content and remote coaching services targeted at athletes, coaches, and sports enthusiasts across multiple geographies [N2].

Strategically consistent with being majority-owned by Sport City Cádiz S.L., Nomadar integrates tightly into the broader Cádiz CF ecosystem and its investor base through Sportech [S1]. This interconnectedness facilitates access to proprietary branding assets but creates potential conflict-of-interest considerations due to overlapping leadership roles on both sides [S1].

Revenue mechanics pivot on milestone fees tied to sublicensing contracts that grant usage rights over the Mágico González brand abroad plus recurring revenues linked to academy operations and event hosting. Pricing levers appear bounded by standard market rates for sports academies and venue management; volume growth depends heavily on scaling international academies and premium live-event programming.

Industry Structure and Competitive Position

Nomadar occupies a distinct niche at the confluence of sports technology, athlete development, event management, and branded merchandise licensing—an intersection where traditional competitors include legacy athletic apparel companies (who have entrenched consumer bases) and non-profit or local sports training organizations (which compete more on accessibility than brand exclusivity).

The company’s moat is primarily built around exclusive licensing deals — especially with Cádiz CF — conferring unique control over key intellectual properties like the Mágico González brand outside Spain. Such rights afford differentiation beyond commodity training services or standard event spaces.

Moreover, ownership of JP Financial Stadium’s event platform represents a valuable asset that could scale through diversified live shows beyond soccer-related events [N2]. This positions Nomadar as not merely a training academy but a multifaceted sports entertainment enterprise.

However, entrenched incumbents benefit from scale advantages in marketing budgets, established partnerships with professional teams worldwide, and direct apparel sales channels complementing their training programs—elements where Nomadar must prove competitive.

Growth Drivers

Several vectors underscore potential revenue expansion:

International Academy Expansion: Agreements like the recent framework deal with Fox Soccer Academy signal intent to broaden youth soccer development reach into markets including the U.S., Europe, Mexico, and India [N1]. Convincing adoption across these regions will drive volume growth.

Live Events Platform Scaling: Post national recognition of the Cádiz Music Stadium segment within JP Financial Arena grounds Nomadar’s push into scalable live events beyond sports matches — potentially tapping into concerts and entertainment rentals for incremental revenue diversification [N2].

Brand Licensing Exploitation: The Mágico González brand exclusivity outside Spain allows development into merchandise sales channels or digital content opportunities servicing fans globally.

Digital Training Platforms: Subscription-based or pay-per-use digital educational portals provide recurring revenue streams less constrained by physical capacity or geography.

These drivers are aligned with KPIs such as new academy enrollments/bookings, live-event attendance figures/capacity utilization at JP Financial Stadium, digital platform subscriber numbers, and milestone payments from sublicensing arrangements.

Risks / Watchpoints / Growth Constraints

Liquidity Risk & Going Concern Uncertainty: The severely negative working capital position requires consistent capital injections; failure to secure adequate funding could force operational cutbacks or jeopardize continuity [S7,S9].

Licensing Dependence: Revenue concentration around licensing deals that can be terminated presents structural fragility—loss of any major partner like Cádiz CF would impair core offerings significantly [S1].

Related Party Conflicts: Overlapping management roles between Nomadar’s executive team and controlling shareholder Sport City Cádiz introduce governance risks which could constrain favorable contract negotiations or future independence [S1].

Competition & Market Acceptance: Competition from large incumbents with broad athletic ecosystems limits pricing flexibility; gaining meaningful market share requires sustained investment in brand awareness.

Execution Risks in International Expansion: Navigating multiple regulatory environments for academies abroad adds operational complexity; delays in stadium completion or event scheduling also constrain revenue realization timelines [S1].

Brand Reputation Sensitivity: Given strong reliance on iconic branding tied to Mágico González's image and association with Cádiz CF’s popularity trajectory creates exposure to performance fluctuations impacting consumer demand.

What to Watch Next

Key upcoming developments include:

- Capital raising progress following the $5.4 million subscription agreement finalized in early 2026; success in these efforts directly affects going concern risk mitigation.

- Construction milestones or acquisition closure related to JP Financial Arena stadium expansion (purchase option executed April 2026) [N4,S14], critical for capacity scaling.

- Growth metrics from international HPT academies including enrollment trends linked with partnership frameworks such as the Fox Soccer Academy alliance announced May 2026 [N1].

- Subscriber adoption rates and engagement figures on digital training platforms expected as part of broader monetization strategies noted in recent disclosures [N2].

- Any modifications or renewals related to core intellectual property license agreements with Cádiz CF impacting exclusivity or financial terms.

- Potential governance changes following board appointments such as José Manuel Calderón that might steer strategic focus or capital markets interface more assertively [S3,N3].

Financial Profile Overview (Latest Quarter)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $3mm | |

| 2026-03-31 | ||

| Current liabilities | $7mm | |

| 2026-03-31 | ||

| Current ratio | 0.36x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Current Assets | $2,664,458 | |

| 2026-03-31 | ||

| Current Liabilities | $7,397,974 | |

| 2026-03-31 | ||

| Current Ratio | 0.36 | |

| 2026-03-31 | ||

| Total Debt | $488,664 | |

| 2024-12-31 | ||

| Net Income | -$2,767,318 | |

| 2025-12-31 | ||

| Operating Income | -$2,691,505 | |

| 2025-12-31 | ||

| Revenue | $921,940 | |

| 2025-12-31 |

The financials reveal nominal revenue generation trailing substantial operating losses tied mainly to fixed costs like professional fees and marketing expenses related to market entry efforts. A heavy reliance remains on non-operational financing steps for cash inflows rather than organic free cash flow generation.

This analysis synthesizes SEC filings up through mid-May 2026 without incorporating speculative projections beyond stated company disclosures. It aims to illuminate Nomadar Corp.’s operational positioning within its emerging sport technology niche balancing compelling exclusive rights against critical liquidity constraints and competitive headwinds.

This document does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments