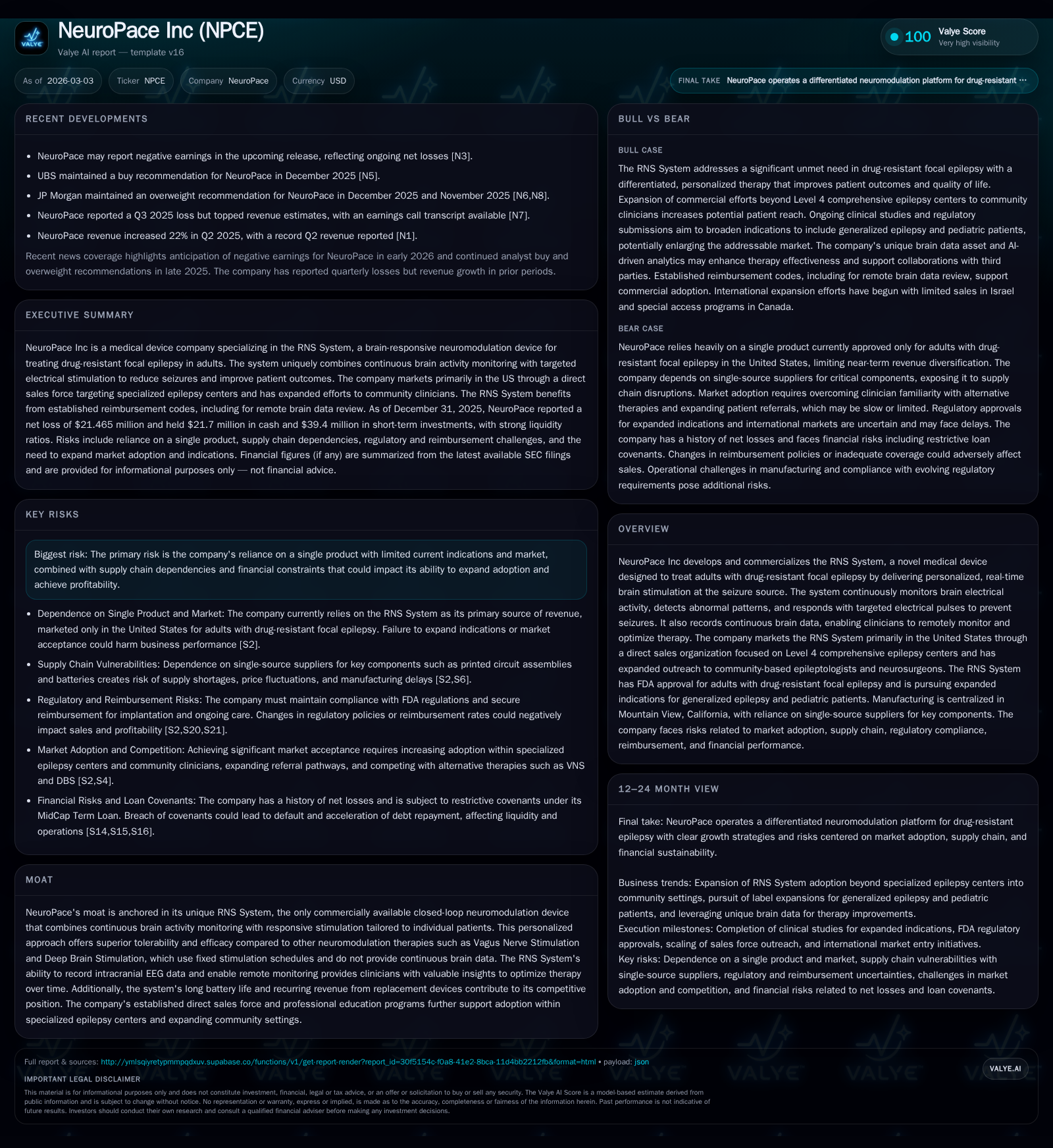

NeuroPace Advances Brain-Responsive Neuromodulation While Managing Profitability Challenges

NeuroPace leverages its pioneering RNS System to deepen epilepsy treatment penetration while working through ongoing operational losses and regulatory headwinds.

NeuroPace stands out in the epilepsy treatment landscape with its unique RNS System, which offers closed-loop neuromodulation by continuously monitoring brain activity and delivering tailored stimulation to prevent seizures. Over the last four years, the company has shown steady improvement in operating and net losses, albeit remaining unprofitable amid significant investment in commercialization. The commercial focus remains on adults with drug-resistant focal epilepsy within specialized Level 4 epilepsy centers, limiting near-term market scope. Prospective FDA approval for expanded indications in generalized epilepsy and pediatric populations represents a critical growth lever. Financially, disciplined capital allocation and strong liquidity support runway despite ongoing negative free cash flow. Key risks include supply chain concentration, compliance costs, and dependence on a single marketed product.

Evolution of NeuroPace’s Growth: Revenue Trends and Operational Shifts

Since 2022, NeuroPace Inc has steadily reduced its operating losses from -$40.8 million to -$16.3 million by the end of fiscal year 2025 [F1]. This marks approximately a 24.6% year-over-year improvement between 2024 and 2025 alone. Net losses have similarly contracted from -$47.1 million in 2022 to -$21.5 million in the latest fiscal year [F1]. Despite these improvements, the company remains unprofitable as it invests heavily in commercial expansion and product development aimed at broader adoption.

Operating cash flow has also improved materially—from a negative $36.9 million in 2022 down to -$11 million in 2025 [F1]. This reflects better cash management even as sales grow gradually within a complex neuromodulation market constrained by clinical training requirements and reimbursement nuances [N1][S1]. Capital expenditures remain modest at $332,000 in 2025, underscoring the company's asset-light model focused on intellectual property and direct sales efforts [F1].

This financial trajectory correlates with strategic initiatives targeting specialized Level 4 comprehensive epilepsy centers first before expanding to community neurologists and epileptologists [S1]. The incremental operating improvements signal effective cost control alongside expanded market reach.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -21 | -11 | -16 | 332000 | +20.9% |

| 2024 | -27 | -18 | -22 | 306000 | +17.6% |

| 2023 | -33 | -20 | -27 | 173000 | +30.0% |

| 2022 | -47 | -37 | -41 | 603000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -11 | -112.8 |

| 2024 | -18 | -338.7 |

| 2023 | -20 | -159.6 |

| 2022 | -37 | -135.4 |

Source: SEC companyfacts cache [F1].

Operating metrics show steady operational improvements driven by scaling efforts; cash flow remains negative but improving.

The Clinical Differentiator: RNS System’s Neuromodulation Advantage

Central to NeuroPace's innovation is the RNS System—a pioneering closed-loop neuromodulation device that continuously records intracranial EEG signals at seizure foci and delivers personalized electrical stimulation only when abnormal activity patterns are detected [S1]. This approach contrasts starkly with traditional therapies such as Vagus Nerve Stimulation or Deep Brain Stimulation that apply fixed-pattern pulses without adapting to ongoing brain signals.

This continuous brain activity monitoring enables clinicians to program patient-specific parameters minimizing unnecessary stimulation—typified by an average daily stimulation time of about three minutes—thus enhancing tolerability while optimizing seizure control [S1][N1]. Another clinically differentiating feature is the system's ability to transmit data remotely for physician review and therapy optimization without requiring frequent clinic visits.

This tailored real-time responsiveness embodies cutting-edge "closed-loop neuromodulation," a term reserved for devices integrating sensing with immediate therapeutic feedback—critical for managing complex focal epilepsies resistant to pharmacotherapy [N1]. Such remote monitoring capabilities represent an advance over prior generation devices lacking data-rich insights into patient neurophysiology.

Market Constraints: Indication Limitations and Commercial Penetration

While clinically robust within its FDA-approved indication—adults with drug-resistant focal epilepsy—the current indication limits total addressable market size to approximately 575,000 patients domestically [S1]. Commercial adoption is concentrated initially among Level 4 comprehensive epilepsy centers equipped with multidisciplinary teams including trained neurosurgeons for implantation and epileptologists for device programming.

Expansion beyond this niche faces challenges due to:

- The specialized training required for implantation and longitudinal programming,

- Complex reimbursement pathways affecting procedural profitability,

- Supply chain dependencies on single-source components creating potential bottlenecks,

- Competition from other established therapies such as resective surgery or newer pharmacological agents [S1][S2][N1].

Community-based neurologists remain slower adopters given the procedural complexities though NeuroPace has initiated outreach programs toward expanding prescriber familiarity beyond traditional tertiary epilepsy centers [N1]. The company’s direct sales organization remains critical in educating providers on device benefits while navigating regulatory hurdles.

Outlook on FDA Expansions and Pipeline Opportunities

A pivotal growth driver lies in successfully securing FDA approvals that extend the RNS System's label beyond adult focal epilepsy into generalized epilepsy forms as well as pediatric populations where neurological plasticity might enable better outcomes [S1][N1]. Expanding into these indications would unlock significantly larger US patient pools—upwards of an additional several hundred thousand candidates—and set the stage for possible international launches targeting millions globally affected by drug-resistant epilepsy.

Such regulatory milestones depend on demonstrating safety and efficacy through ongoing or planned clinical studies overseen by stringent FDA protocols [S1][N1]. These filings represent near-term catalysts capable of materially extending NeuroPace's revenue runway if approved.

Financial Performance Snapshot: Navigating Continued Losses

Despite improvements detailed above, NeuroPace maintains substantial losses indicative of aggressive growth investment strategies common among medtech innovators still scaling market penetration:

- Operating income improved nearly $24 million from -$40.8M (2022) to -$16.3M (2025) but remains negative [F1],

- Net income follows this trend reflecting ongoing R&D spend plus SG&A expenses required for sales expansion,

- Operating cash flow follows suit—negative but improving by ~39% YoY from ’24 to ’25 [F1],

- Capital expenditures remain nominal relative to operating losses illustrating a focus on clinical/marketing investments over heavy infrastructure buildout,

- Equity levels reported $19M at FY-end ‘25 supporting tangible book value amidst operating deficits.

Return on equity approximates -112%, consistent with accumulated net losses exceeding book equity [F1]. Liquid assets stand strong with $21.7 million cash combined with $94 million total current assets versus liabilities under $18 million yielding a current ratio above 5x—providing a buffer against short-term liquidity shocks [F1].

Capital Allocation Discipline: Cash Flow, Liquidity, and Investor Returns

NeuroPace exhibits conservative capital expenditure relative to operational scale—capex was just $332K in FY25 against $11 million negative CFO—highlighting cautious spending tied mainly to maintaining manufacturing capabilities rather than expansion [F1][S26].

The company carries no dividends or share buybacks; instead preservation of cash serves as priority amidst ongoing path toward profit generation [F1][S26]. Excess liquidity assists in meeting debt covenants of existing facilities while underpinning continued investment into clinical validation and sales infrastructure expansion.

Free cash flow remains negative at approximately -$11.3 million annually but reflects progress consistent with early-stage medtech firms balancing growth vs profit sequencing [F1]. This underscores the need for future revenue acceleration tied closely to indication expansions or volume-scale effects for viability.

Risks from Supply Chain and Regulatory Compliance

Substantial risks stem from dependence on single-source component suppliers integral to the RNS System manufacture—any disruption could significantly impair revenue delivery or product availability impacting clinical adoption reliability [S2][S13][S23]. Catastrophic events are partially mitigated by insurance but long lead times for FDA manufacturing site authorization could compound disruptions [S21].

Regulatory environment imposes complex burdens including:

- Extensive FDA pre-market PMA approval process governing product marketing plus stringent post-market surveillance obligations,

- Healthcare fraud & abuse laws encompassing Anti-Kickback Statute plus False Claims Act exposure necessitate robust compliance regimes,

- Cybersecurity governance tightly integrated via board audit committee oversight reflecting heightened medical device sector norms,

- Environmental regulations regarding hazardous substances used during production add another layer of cost/risk exposure [S4][S5][S6][S7].

Violations risk material fines plus reputational damage potentially delaying market entry or causing costly corrective actions impacting financial profile substantially.

Key Milestones Ahead: What Investors Should Monitor

Critical inflection points lie ahead centered on:

- Filing status updates around expanded FDA indications particularly for generalized epilepsy and pediatric segments,

- Emerging clinical trial data releases validating efficacy/safety enhancements necessary for label augmentations,

- Quarterly adoption rates reported through direct sales metrics especially penetrating community-based neurology practices beyond Level 4 centers,

- Regulatory compliance outcomes including cybersecurity incident disclosures or supplier audit findings may influence operational stability perception [N1][S3].

Successful navigation of these milestones will either reinforce confidence in scaling trajectories or expose bottlenecks restricting broader commercialization—a defining axis shaping medium-term growth prospects.

This analysis integrates company filings as filed up to March 3rd, 2026 together with recent earnings commentary but does not contain investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments