ENVIRI Corp Readies Post-Divestiture Focus on Harsco Environmental and Rail with $3B Clean Earth Sale

Q1 2026 results underline transition as ENVIRI advances $3 billion Clean Earth sale, setting the stage for a standalone New Enviri entity.

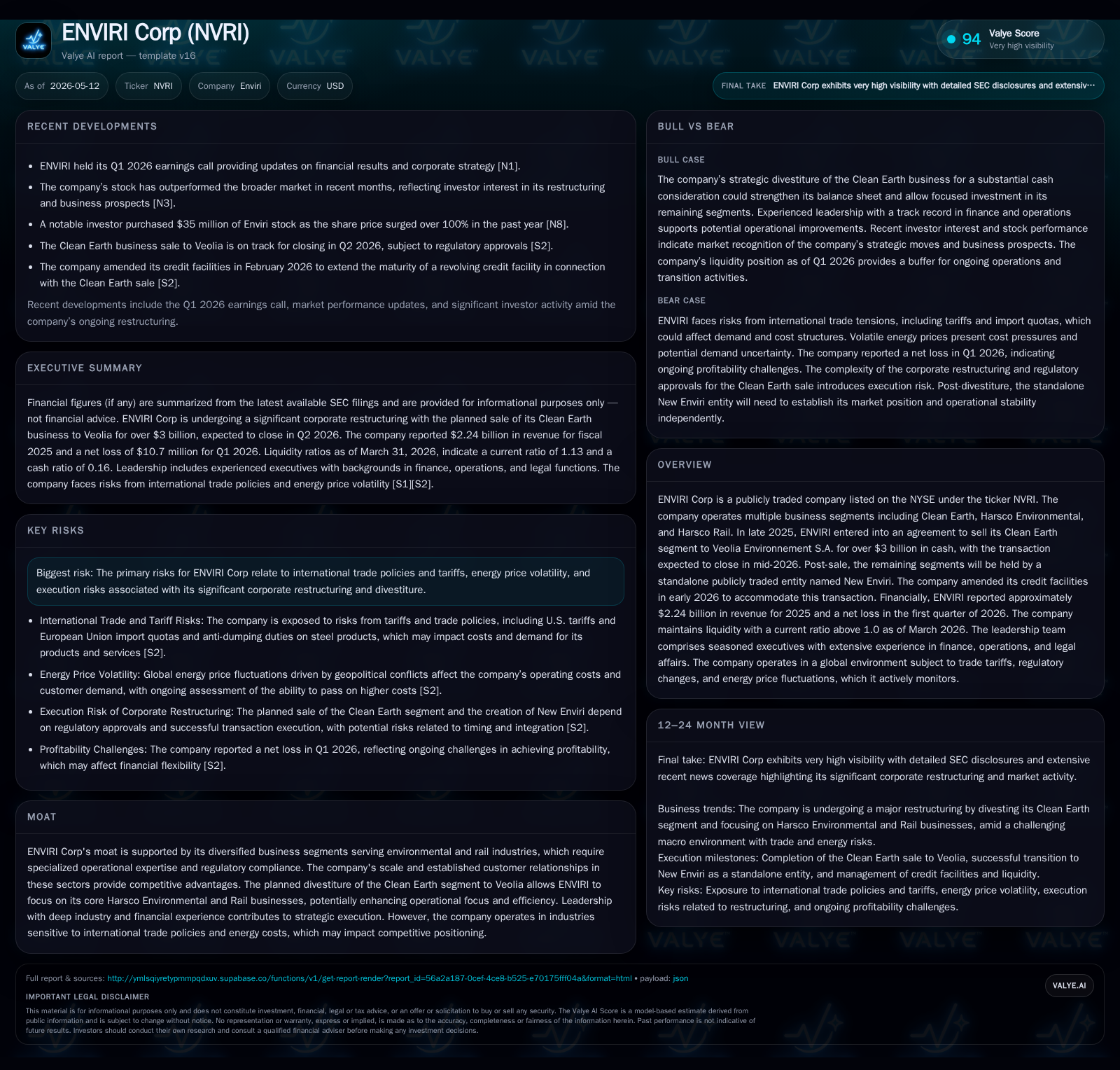

ENVIRI Corp's latest quarterly filing reflects a pivotal shift with the imminent divestiture of its Clean Earth business to Veolia for over $3 billion, expected in mid-2026. This transformative transaction refocuses ENVIRI on its Harsco Environmental and Rail segments housed in a new independent public company named New Enviri. Despite a net loss in Q1 2026, the company sustains adequate liquidity with a current ratio above 1.0. The upcoming post-sale period centers on operational efficiency and strategic execution amid ongoing trade policy uncertainties and energy cost volatility that influence demand dynamics and pricing.

Recent Operating Update

As of the first quarter ended March 31, 2026, ENVIRI Corp provided its latest operating disclosure through its Form 10-Q filed May 11, 2026 [S2]. The primary highlight is the ongoing sale of its Clean Earth business to Veolia Environnement S.A. for over $3 billion in cash consideration. Closing is anticipated by June 1, 2026, subject to regulatory approvals. Concurrently, ENVIRI is preparing a corporate separation whereby the remaining businesses—Harsco Environmental and Harsco Rail—will continue under a new publicly listed entity named New Enviri [S2][S3].

The Q1 results showed continued investment into transition activities contributing to a net loss for the period. However, the company maintained strong liquidity with cash and equivalents totaling approximately $106 million and a current ratio of 1.13 [F1][S2]. The maturity of revolving credit facilities was adjusted to align with the timing of the Clean Earth sale closing [S2].

This evolving operating landscape represents a material pivot for ENVIRI from a diversified environmental services platform towards a more focused industrial services profile anchored on engineered solutions within environmental remediation (excluding Clean Earth) and rail segments.

Business Model Analysis

ENVIRI historically earned revenue through three principal segments: Clean Earth (environmental waste management/environmental remediation services), Harsco Environmental (specialized environmental solutions), and Harsco Rail (railway track maintenance products). Revenue derives primarily from contracts with industrial clients requiring compliance-driven disposal or treatment services, as well as engineered product sales tied to rail infrastructure maintenance.

The strategic decision to sell Clean Earth—a large volume waste management business—marks a critical model transformation. This segment contributed significantly both top-line (note: full revenue breakdowns are embedded in filings but not detailed here) and cash flow metrics pre-sale; divesting this unit emphasizes higher-margin engineering service lines with potentially less cyclical exposure.

Going forward, New Enviri will rely on Harsco Environmental's specialized offerings including waste-to-product solutions and sustainable environmental remediation technologies alongside the Harsco Rail segment that supplies engineered products for rail track infrastructure upkeep. These units have differentiated niches demanding technical expertise and regulatory know-how, creating switching costs that support stable customer retention.

Pricing models vary across units: long-term fixed price contracts dominate engineered equipment sales in rail while more transactional or project-based pricing appears in environmental remediation projects. Volume fluctuations correlate with industrial production cycles but also strategic infrastructure spending decisions.

Industry Structure and Competitive Position

The industry environment is complex due to heavy regulation across environmental safety compliance and infrastructure maintenance sectors globally. ENVIRI’s Harsco Environmental benefits from scale and technical certification barriers impeding smaller entrants—its global footprint grants competitive advantages in managing multi-jurisdictional contracts.

Rail segment competitors range from commodity suppliers to integrated service providers; ENVIRI’s focus on engineered product innovation supports differentiation versus commoditized offerings. Furthermore, longstanding customer relationships with large rail operators establish conduit for recurring revenue streams.

However, tariff policies in multiple jurisdictions loom as external risk factors — U.S.-imposed tariffs on imported goods have prompted countermeasures notably in Europe where steel import quotas are tightening [S2]. Such trade frictions influence input costs for equipment manufacturing in rail products as well as downstream demand dynamics.

Energy cost fluctuations driven by geopolitical instability have multiplicative effects across operating expenses for all business lines given fuel intensity in logistics and processing activities.

Growth Drivers

- Post-Divestiture Strategic Focus: With Clean Earth sold, management can pursue operational efficiencies in specialized environmental services leveraging proprietary technologies and process optimizations.

- Infrastructure Investment Cycles: Urbanization trends and government stimulus spending targeting transportation infrastructure rehabilitation underpin steady demand growth for rail maintenance equipment.

- Environmental Regulation Trends: Increasingly stringent industrial emissions standards globally spur demand for innovative environmental remediation solutions offered by Harsco Environmental.

- Technological Advancements: Adoption of sustainable waste processing methods positions New Enviri favorably amidst rising ESG-driven client expectations.

- Contract Backlog & Renewals: Sustained backlog levels supported by multi-year service agreements provide revenue visibility; disciplined contract management aids margin stability.

Risks and Growth Constraints

- Execution Risk of Separation: Complexities involved in spinning off New Enviri raise operational integration challenges that may disrupt service continuity or increase overhead temporarily [S2][S3].

- Market Sensitivity to Trade Policies: Tariff impositions may elevate raw material costs particularly steel inputs affecting margins downstream in rail equipment manufacturing.

- Energy Price Volatility: Unpredictable fuel costs impact operating expenses severely; limited pass-through capabilities restrict margin protection.

- Regulatory Compliance Exposure: Failure to secure or renew critical permits could impede certain operations; environmental litigation risks persist.

- Customer Concentration & Contract Risk: Fixed-price contracts may carry margin compression risk if cost inflation materializes beyond assumptions; dependence on key customers could lead to volatility if contracts are lost.

- Labor Market Dynamics: Union negotiations or labor shortages could escalate wage costs or cause operational disruptions.

What To Watch Next

- Completion of Clean Earth Sale: Confirm closing by June 2026 without material delays or regulatory conditions impacting deal economics [S2][S3].

- New Enviri IPO/Market Debut: Performance metrics post-separation including revenue run rate, EBITDA margins, order backlog evolution will be critical indicators of standalone viability.

- Trade Policy Developments: Monitoring updates around EU steel import quota approvals or U.S trade negotiations that may affect input cost inflation.

- Energy Cost Pass-through Strategies: Management commentary regarding ability to mitigate energy cost pressures through pricing adjustments or operational changes.

- Contract Wins / Backlog Changes: Bookings trends within rail equipment orders or environmental project awards signaling demand strength or softness.

Financial Profile (Brief)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $106mm | |

| 2026-03-31 | ||

| Total debt | $1567mm | |

| 2025-12-31 | ||

| Net debt | $1461mm | |

| 2025-12-31 | ||

| Current assets | $722mm | |

| 2026-03-31 | ||

| Current liabilities | $641mm | |

| 2026-03-31 | ||

| Current ratio | 1.13x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Revenue reached approximately $2.24 billion during fiscal year 2025 with an operating income slightly above $4 million but was offset by significant net loss attributable largely to transitional charges related to restructuring efforts [F1]. The balance sheet at March 31, 2026 shows total current assets of about $722 million against current liabilities near $641 million sustaining a current ratio of approximately 1.13 indicating manageable working capital status [F1]. Cash reserves stood near $106 million supporting ongoing operational needs during this transition phase while total debt was estimated at around $1.57 billion at year-end 2025 implying substantial leverage ahead of divestiture completion [F1]. Capital structure revisions via amended credit facilities reflect proactive steps aligning maturities with transaction timing [S2].

This analysis is based strictly on available public disclosures including recent SEC filings up to May 11, 2026. It focuses on understanding operating shifts in light of significant corporate restructuring ahead at ENVIRI Corp without providing investment advice or forecasts not explicitly supported by cited evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments