NexPoint Diversified REIT’s Q1 Challenges Highlight Adviser Conflicts and Leverage Risks

The latest quarterly report reveals operational losses intertwined with adviser conflicts and high leverage, shaping NexPoint’s risk landscape in real estate investing.

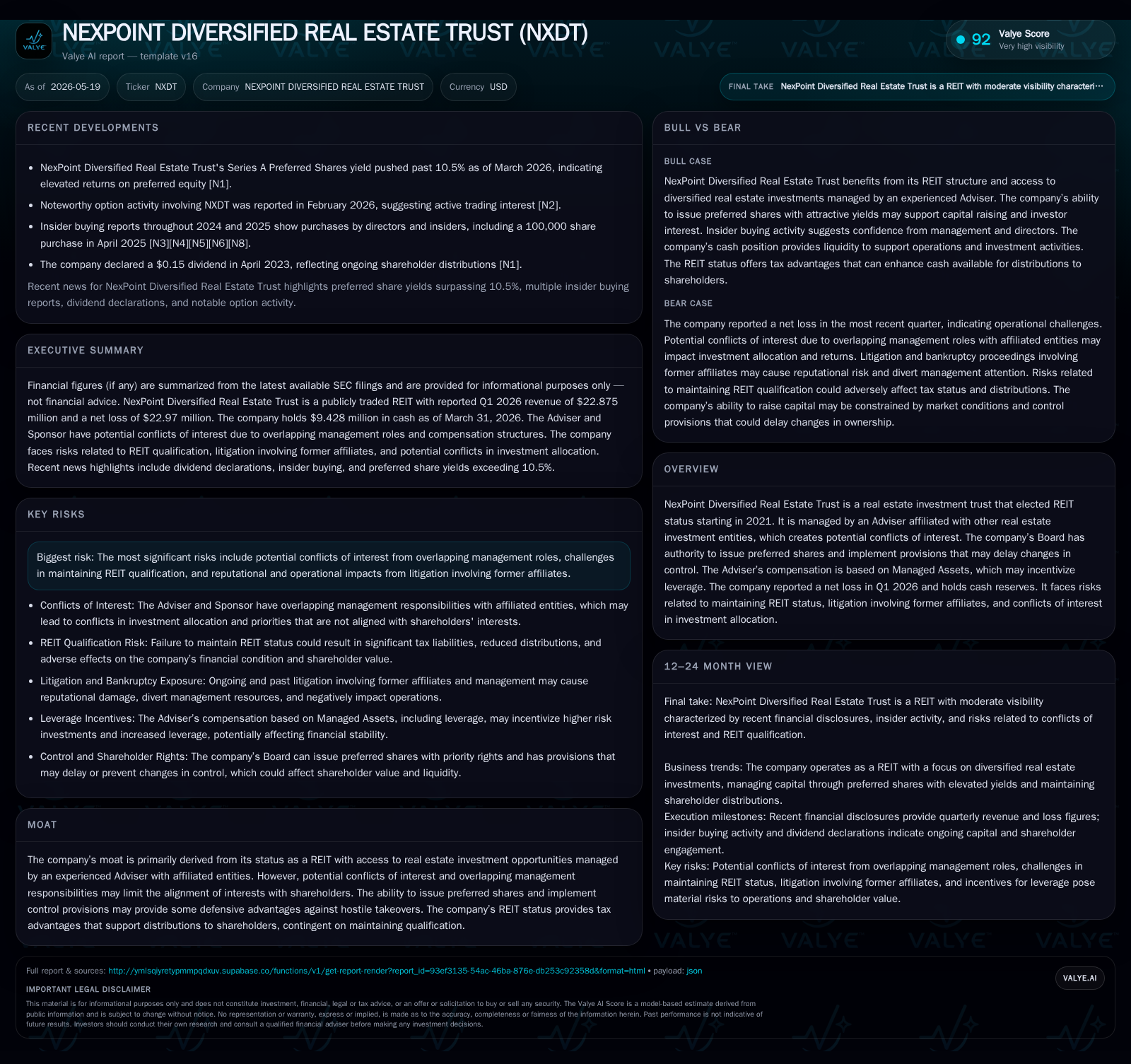

NexPoint Diversified Real Estate Trust reported a net loss in Q1 2026, underscoring operational pressures and significant leverage near $275 million in net debt. The company’s adviser-managed structure, involving multiple affiliated real estate entities, generates potential conflicts of interest that influence investment allocation and risk exposure. Maintaining REIT status remains crucial amid IRS scrutiny of mortgage loan classifications and industry-wide leverage sensitivity. Going forward, litigation outcomes, asset mix success, and management strategies around leverage will be pivotal indicators of the trust’s trajectory.

Q1 2026 Operating Update: Losses, Leverage, and Strategic Signals

NexPoint Diversified Real Estate Trust’s latest quarterly filing [S2] details a challenging start to 2026 marked by a net loss reflective of broader operational pressures. The reported operating results underscore the tension between pursuing growth through leverage and managing earnings volatility inherent in their diversified real estate portfolio. At quarter-end March 31, 2026, the company held approximately $9.4 million in cash and equivalents against total debt near $284.4 million for a net debt position around $274.9 million [F1]. This capital structure situates the trust with significant leverage relative to liquidity, amplifying its sensitivity to interest rate fluctuations and potential credit market headwinds.

The persistence of net losses signals stress on distributable earnings capacity, calling attention to the sustainability of dividend policies under continued earnings volatility. Although there were no material changes in disclosed risk factors this quarter [S2], the results accentuate the imperative for NexPoint’s management to navigate adviser-related governance complexities while controlling financial risk.

Business Model Examination: Adviser-Managed REIT With Multifaceted Real Estate Investments

Operating as a REIT since 2021, NexPoint Diversified relies on an Adviser that manages a suite of affiliated real estate investment vehicles including other REITs with overlapping leadership teams [S1]. This affiliation forms the backbone of its business model but also introduces layered conflicts of interest. The Adviser’s compensation is based in part on managed assets rather than pure performance metrics, providing structural incentives to increase leverage to expand asset scale [S1]. This creates tension between expanding asset bases and preserving capital resilience.

The advisory agreement allows the entity considerable discretion within broad investment guidelines encompassing equity stakes in commercial properties as well as mortgage loans. Notably, potential internalization efforts—where the company might acquire management functions from the Adviser—have proven contentious with litigation risks highlighted historically [S1]. The operating partnership structure further adds complexity to capital flows among NexPoint affiliates and poses challenges in aligning shareholder interests against those of the sponsor firms.

Competitive & Industry Context: Peer Overlaps, REIT Qualification Challenges, and Sector Leverage Dynamics

Within the competitive ecosystem, NexPoint operates alongside related publicly traded entities such as NexPoint Residential Trust (multi-family), VineBrook Homes Trust (single-family rentals), and NexPoint Real Estate Finance (mortgage REIT) under shared management umbrellas [S1]. This clustering creates competition for similar investment opportunities, particularly in mortgage loans where return profiles have been pressured by intensifying rivalry.

A defining compliance risk for NexPoint lies in IRS gross income tests mandated for REIT qualification. Mortgage loans that do not meet specific secured real estate thresholds may cause NexPoint to fail the 75% gross income test if IRS positions challenging current interpretations around loan security prevail [S1]. Such regulatory scrutiny aligns with broader sector concerns regarding high leverage models faced with inflationary pressures and rising interest rates that exacerbate refinancing risks.

Growth Drivers: Asset Class Diversification and Adviser Deal Flow as Revenue Catalysts

NexPoint’s strategic path for growth rests heavily on its broad asset diversification strategy that spans both real estate equity investments and debt instruments such as senior loans secured by properties [S1][S2]. This mix aims to balance yield generation with capital preservation within volatile market conditions

Crucial to this approach is the Adviser’s ability to source attractive deals from its network across multiple related entities, leveraging scale advantages and market insight. However, conflicts inherent in allocation decisions among competing funds could dilute deal quality or skew returns if certain affiliates receive preferential access—a key point of investor vigilance.

Successful adoption of this mixed portfolio approach would be reflected in improving gross income test compliance metrics and stable margins amid fluctuating interest spreads.

Risks & Governance Watchpoints: Conflicts of Interest, Regulatory Compliance, and Leverage Concentration

Central to NexPoint’s risk profile are governance frictions arising from conflicts of interest due to overlapping advisory roles managing several related vehicles with potentially competing objectives [S1][S2]. These conflicts raise questions about fair allocation of investment opportunities which materially impact returns.

Further layers of risk involve reliance on maintaining its tax-advantaged REIT status amidst evolving IRS interpretations regarding mortgage loan security classifications that could lead to costly recharacterizations.

The high leverage level compounds these risks by heightening sensitivity to credit market tightening or downturns that could impair liquidity or force distressed asset sales.

Additionally, historical internalization efforts have sparked litigation threats implying non-trivial legal expenses that divert capital from distribution or reinvestment priorities [S1]. While no new material risk factor updates appeared in Q1 filings [S2], these governance issues remain persistent watchpoints.

Upcoming Catalysts & Metrics to Monitor: Retaining REIT Status, Litigation Trajectory, and Investor Signal Points

Key near-term milestones include monitoring any IRS actions clarifying treatment of mortgage loans relative to REIT qualification tests. Such guidance would materially influence NexPoint’s gross income compliance probability and strategic adjustments.

Outcomes from ongoing or new litigation related to adviser internalization plans will also unveil financial impacts or governance shifts affecting future capital deployment approaches.

Investors should track timing for net income inflection points indicating recovery from recent losses along with any announced changes in preferred share issuances or other control provisions initiated by the Board as defensive measures against hostile control shifts [S3]

The direction taken by the Adviser concerning asset allocation priorities across affiliated entities will serve as a barometer for future conflict intensity and overall portfolio quality.

Financial Overview: Latest Balance Sheet Liquidity, Debt Positioning, and Operating Performance

As of March 31, 2026, NexPoint maintained cash reserves approximating $9.4 million versus total debt obligations near $284.4 million [F1], resulting in a net debt position close to $274.9 million indicative of substantial financial leverage. This ratio places pressure on cash flow sufficiency given recent operational losses annualized above $130 million [F1].

This liquidity-debt profile underscores limited flexibility during adverse market conditions or regulatory shifts requiring capital restructuring or loss absorption. Net operating losses have directly diminished distributable earnings capacity creating tension between sustaining dividends expected by shareholders and conserving capital buffers amid unstable earnings dynamics.

Overall, this financial snapshot concurs with earlier analyses on strategic vulnerability stemming from adviser-influenced growth ambitions compounded by elevated leverage risks.

Disclaimer: This analysis is strictly informational and does not constitute investment advice or research views. All data included is based on publicly filed documents up to May 15, 2026. Readers are encouraged to consult official filings and perform their own due diligence before making any investment considerations.

Financial position in context

As of 2026-03-31, companyfacts shows $9mm in cash and equivalents and $284mm of total debt [F1]. The same snapshot implies net debt of roughly $275mm, keeping balance-sheet context relevant but secondary to the operating story [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments