Orion Energy Systems' Strategic Crossroads: Navigating Growth Amid Financial Constraints in Energy Lighting and EV Infrastructure

Orion Energy Systems reports stronger-than-expected Q3 results while confronting financial tightrope from acquisition obligations and capital needs.

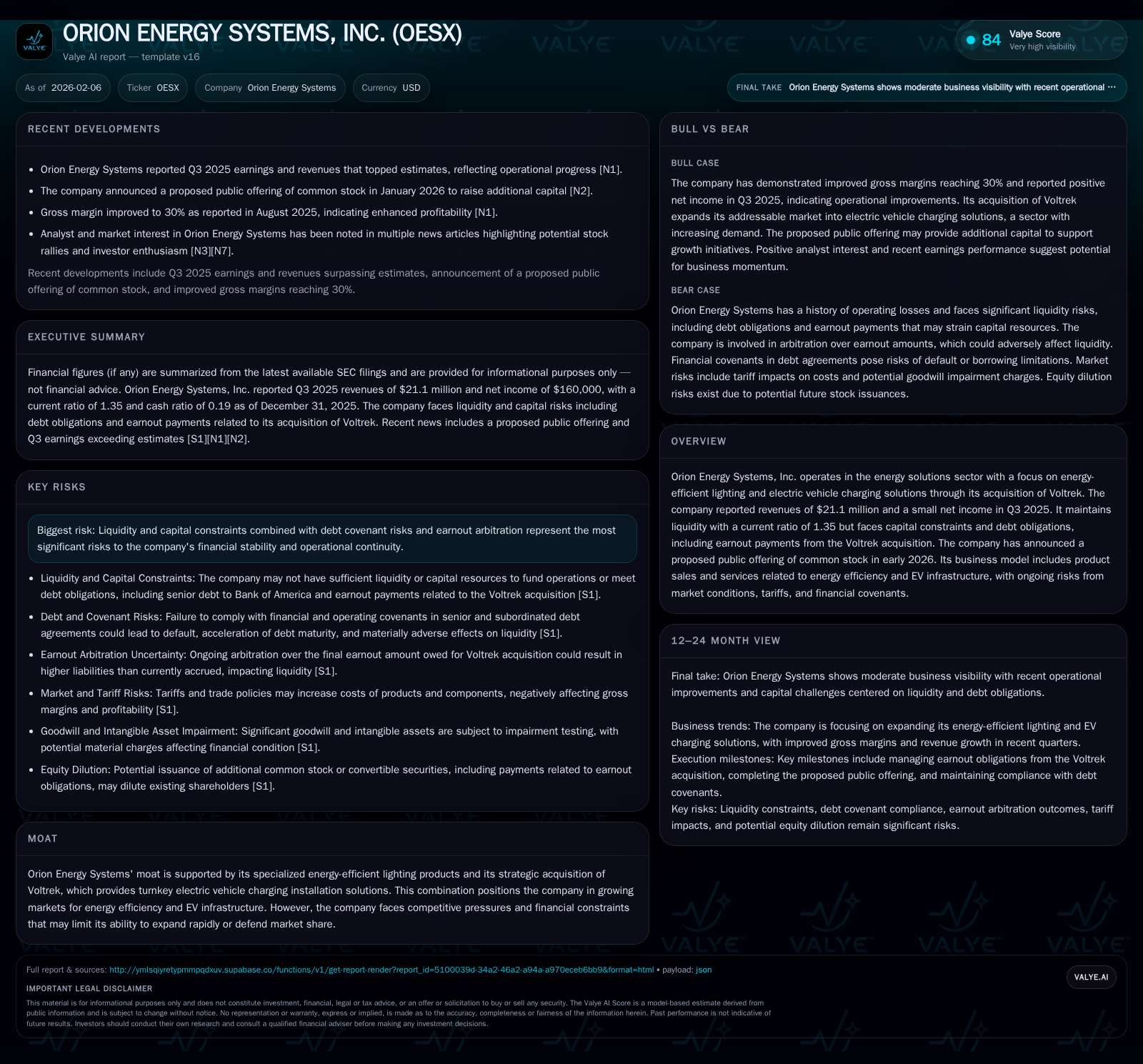

In Q3 2025, Orion Energy Systems generated $21.1 million in revenue and squeezed out a modest net income, signaling operational resilience despite a challenging industry backdrop. The company's acquisition of Voltrek broadens its footprint in the burgeoning electric vehicle (EV) charging market but introduces earnout payments that exacerbate liquidity pressures. With a current ratio of 1.35 and limited cash reserves facing substantial near-term liabilities, Orion is poised to pursue a public offering to bolster its balance sheet. This analysis explores how these dynamics intertwine within Orion’s niche specializations and prevailing risks, underscoring the delicate balance between growth ambitions and financial realities.

Outshining Expectations: A Q3 Earnings Deep Dive

Orion Energy Systems reported third-quarter 2025 revenue of $21.1 million, outpacing analyst estimates [N1][F1]. This top-line strength signaled operational execution capabilities amid a competitive energy solutions landscape focused increasingly on efficiency and sustainability. While the gross profit line holds promising indications for product-market fit, the net income achieved was a mere $160,000—barely tipping into positive territory [F1]. Such muted profitability underscores ongoing cost structure challenges typical for companies in capital-intensive sectors blending hardware sales with service components.

By threading this needle between revenue growth and fragile bottom-line gains, Orion paints a portrait of business fundamentals stabilized enough to support forward momentum but not yet robust enough to absorb debt or funding pressures comfortably.

Strategic Expansion: The Voltrek Acquisition's Promise and Uncertainties

In late 2024, Orion completed the acquisition of Voltrek, markedly expanding its product array into electric vehicle charging infrastructure [valye_report_excerpt]. This move aligns with energy transition trends as corporate and municipal clients seek integrated energy-efficient lighting paired with EV charging solutions—markets growing under regulatory pushes and consumer adoption curves.

Voltrek's turnkey installation service model complements Orion’s legacy lighting offerings by embedding itself deeper into customer site energy ecosystems. However, this expansion comes at a price: substantial earnout obligations linked to Voltrek’s performance milestones remain on Orion’s balance sheet [S2]. These contingent payments impose an added layer of financial strain, effectively siphoning capital that could otherwise fuel organic growth or deleveraging efforts.

The strategic logic here remains sound—synergistic cross-selling and broadening addressable markets—but balancing near-term cash flow demands against long-term value creation presents an ongoing managerial challenge.

Financial Tightrope: Crunching Liquidity, Debts, and Earnout Pressures

Dissecting balance sheet metrics reveals the tightrope that Orion must walk. At quarter-end December 2025, current assets stood at approximately $32.8 million against current liabilities over $24.2 million, calculating to a current ratio of roughly 1.35 [F1]. While above 1.0—a basic threshold signaling ability to cover short-term debts—the ratio leaves minimal margin for error given expected operational volatility.

Within current assets, cash and equivalents represent just $4.7 million [F1], stark compared to the weight of immediate obligations including senior debt owed to Bank of America alongside the aforementioned Voltrek earnouts [S2]. Notably, much of Orion’s asset base is encumbered through security interests granted under lending arrangements, limiting collateral availability for new financing.

Further complicating matters is the company’s history of operating losses spanning several years combined with inconsistent achievement against guidance targets [S2]. Such features reduce lender appetite and investor confidence alike.

Taken together, these factors frame an environment where liquidity management becomes paramount—operational missteps or adverse external shocks could precipitate liquidity crises requiring rapid restructuring or asset sales.

Capital Markets Playbook: Decoding the Proposed Public Offering

Against this backdrop of constrained liquidity and impending payment obligations, Orion announced plans for a public offering of common stock in early 2026 [N2]. The rationale is straightforward: raise fresh equity capital to enhance working capital resources and support debt servicing activities including Voltrek earnouts [S2].

Yet this strategic necessity carries shareholder consequences—the dilutive impact arising from issuing new shares typically tempers investor enthusiasm especially when share prices remain subdued amid existing concerns over profitability and execution risk.

Nonetheless, raising capital through equity rather than additional debt may represent the most viable option given existing leverage levels and collateral limitations documented in recent filings [S2]. Timing this offering amid positive earnings news might also improve reception compared to periods marked solely by distress signals.

Competitive Terrain: Orion’s Moat in Energy Efficiency and EV Charging

Orion's business differentiates itself through proprietary technology for energy-efficient lighting systems coupled with integrated EV charging infrastructure via Voltrek [valye_report_excerpt]. This blend targets customers seeking comprehensive sustainability upgrades—leveraging reduced energy costs along with EV readiness initiatives increasingly mandated across commercial properties.

However, barriers to entry are modest relative to deep-pocketed competitors who can undercut pricing or scale more rapidly through broader distribution networks or vertical integration. Moreover, emerging players specializing solely in EV infrastructure sometimes demonstrate agility that offset Orion’s combined approach advantages.

Financial constraints limit aggressive scaling or defensive marketing investments further suppressing market share aspirations despite product quality or technological edge upholds a defensible niche position.

Risks Below the Surface: Arbitration, Tariffs, and Market Volatility

Layered onto internal challenges are looming external uncertainties detailed in filings [S2]. In particular, earnout arbitration looms as a material risk—potential disputes over payments tied to Voltrek's post-acquisition performance could inject unpredictability into cash flow forecasts.

Tariff exposure on imported components used within lighting fixtures or charging hardware elevates cost structures just as inflationary pressures test margin resilience [valye_report_excerpt][S2]. Shifts in geopolitical tensions or trade policy thus compound operational risk beyond conventional market fluctuations.

Taken together these factors demand vigilant risk management practices embracing both contractual safeguards around acquisitions and proactive supply chain diversification strategies.

Outlook Portrait: Can Orion Balance Growth Ambitions with Capital Constraints?

Investor interest described as coming from 'trend' oriented segments attracted by sustainability themes provides optimistic signals for market receptivity if execution hurdles can be overcome [N3]. Achieving consistent revenue growth aligned with margin improvement remains crucial for unlocking further valuation expansion.

Operationally, blending expertise across efficient lighting systems with EV charging capabilities situates Orion favorably within unfolding clean energy ecosystems despite stiff competition. Nonetheless meaningful progress depends heavily on managing liquidity prudently while navigating inevitable short-term dislocations linked to debt loads, credit covenants, tariffs, and acquisition-related financial commitments [valye_report_excerpt][S2].

The proposed capital raise early in 2026 emerges as a pivotal event that could either facilitate renewed scaling investments or introduce dilution pressures that temper stakeholder enthusiasm.

In sum, Orion sits at an inflection point where strategic intent must be matched tightly by financial discipline; success will hinge not just on product innovation but also on nuanced navigation through a constrained capital landscape peppered with complex risks.

This memorandum synthesizes publicly available information as of February 2026 without endorsing any investment action or projecting specific outcomes. Readers should consider multiple perspectives when evaluating company prospects amid evolving industry conditions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments