Warrior Met Coal’s Blue Creek Advancements Amid Cyclical Steel Demand and Regulatory Shifts

Warrior Met Coal is expanding metallurgical coal production through early Blue Creek mine operations while navigating steel market cycles and evolving regulatory risks.

Warrior Met Coal Inc. plays an indispensable role in the global steel supply chain by producing high-quality metallurgical coal essential for steelmaking. The early commissioning of its Blue Creek mine significantly boosts production capacity and cost competitiveness, underpinning a robust financial position bolstered by nearly $300 million in cash. However, cyclical demand in the steel industry, commodity price volatility, and regulatory challenges frame a complex operating environment. Insider activity and options market debut reflect heightened investor focus amid these dynamics.

From the Mines to Steel Mills: Warrior Met’s Crucial Role in Global Steelmaking

Warrior Met Coal emerges as a vital player in the international steelmaking ecosystem by focusing exclusively on metallurgical coal—the coking variety required for coke production integral to steel furnaces. Its geographically diverse customer footprint spans Europe, South America, and Asia. The company mines premium quality coal primarily from underground longwall operations in Alabama's Southern Appalachian region. This coal exhibits favorable characteristics such as low sulfur content and high fluidity that boost its desirability for integrated steel mills.

The firm differentiates between its Mine No. 7 hard coking coal trading near Platts Premium Low Volatility Australian benchmark prices, versus Mine No. 4 and Blue Creek coals categorized as High Volatility A quality priced relative to Atlantic Basin indices. By aligning product grades to target regional indices, Warrior Met secures demand stability amidst fluctuating global trade flows [S1].

Blue Creek Breakthrough: Early Operations Ahead of Schedule and Its Upside Potential

A defining strategic inflection for Warrior Met is the accelerated start-up of the Blue Creek longwall operation in October 2025—beating timelines by eight months while remaining on budget. This advance has shifted the company's production profile markedly upward; it achieved roughly 1.8 million metric tons output in its inauguration year and anticipates at least 4.1 to 4.4 million metric tons in 2026 alone.

Technological innovations implemented have pushed Blue Creek’s nameplate capacity from an initial 4.4 million up by 25% to approximately 5.4 million metric tons annually. Further enhancements including a fourth continuous miner could lift potential capacity toward roughly 6.4 million metric tons—a transformative leap that expands overall company capacity by about 88% from prior figures around 7.3 million to nearly 13.7 million metric tons per year [S1][N3].

Importantly, Blue Creek operations contribute to lowering cash production costs and enhance positioning within the industry's lowest quartile cost bracket—an essential foothold when facing commodity price variability [S1].

Financial Pulse: Analyzing the Latest Earnings and Balance Sheet Strength

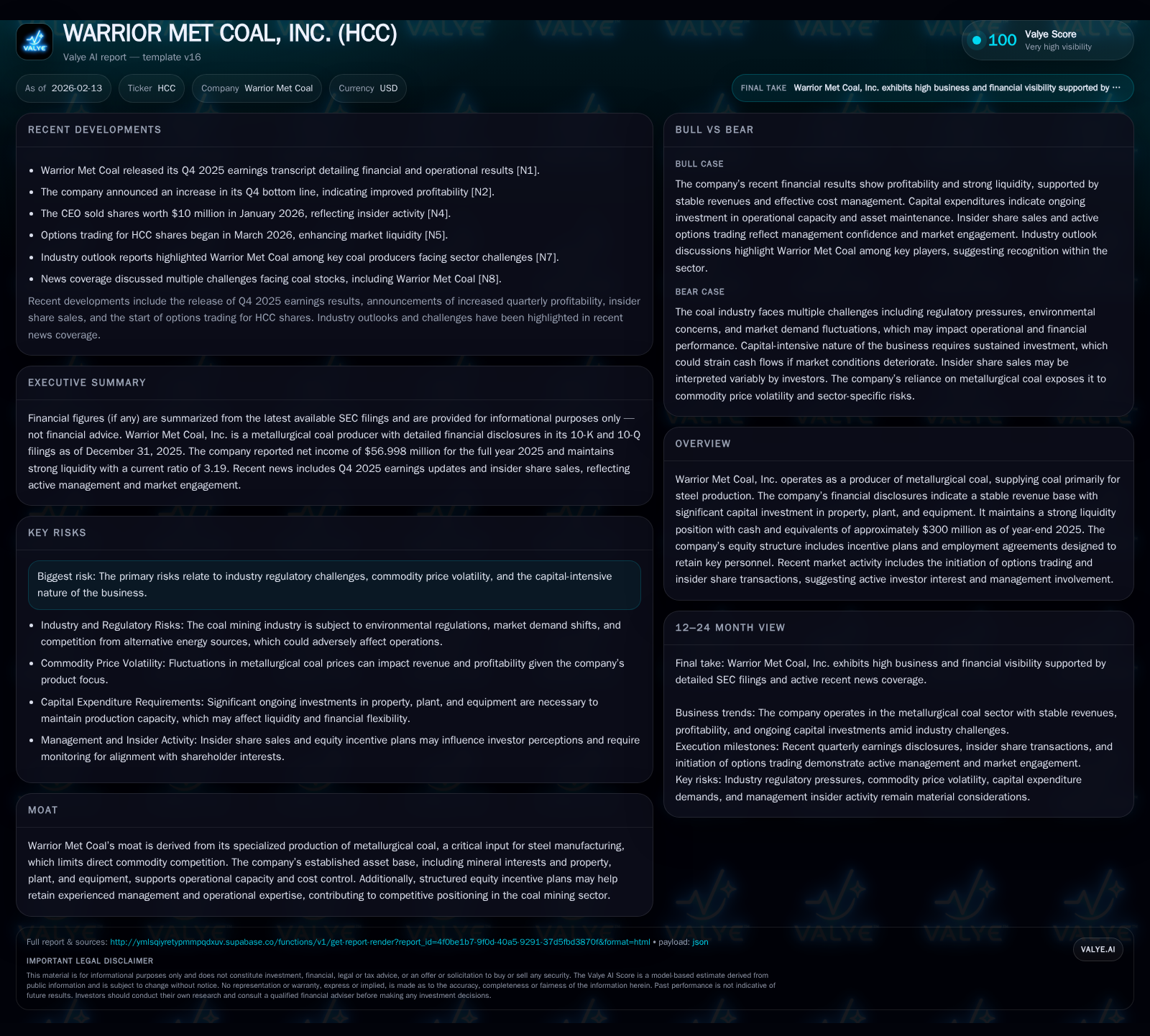

Examining recent financial results sheds light on Warrior Met’s sturdy operational footing amid sector cyclicality. For full-year fiscal 2025, net income reached approximately $57 million with revenues stabilizing around $903 million according to company filings [F1]. Q4 earnings transcripts reveal consistent sales near prior year levels but reflect rising depreciation due to heavy capital investment.[N1]

The balance sheet remains resilient; cash and equivalents totaled nearly $300 million at year-end supporting flexibility for outstanding capital requirements related to Blue Creek and other projects [F1]. Current assets stood at $820 million against current liabilities of $257 million yielding a comfortable current ratio near 3.2x—a positive liquidity buffer.

Production Capacity Surge and Cost Dynamics Driving Competitive Edge

Warrior Met’s recoverable reserves across three operating underground mines approximate 179.3 million metric tons while Blue Creek adds an incremental estimated 54 million metric tons—a notable increase in the company's resource base underpinning multi-year production potential.[S1][F1]

Consistent capital deployment exceeding $950 million on Blue Creek underscores commitment to infrastructure that supports scalable output without significant cost penalties. This scale combined with efficient mining practices has reduced all-in cash cost breakeven points substantially—the effect manifested already since Blue Creek began commercial production [S1].

The company’s ability to maintain first-quartile cost structure strengthens resilience amid volatile coal pricing environments where margins can erode swiftly without operational discipline.

Navigating Commodity Price Volatility and Market Demand Cycles

Steel demand volatility inevitably cascades into fluctuations for metallurgical coal prices given tight linkage—the mainstay commodity for blast furnace coke blending [S1][S2]. Warrior Met’s contracts typically reflect short-to-medium term pricing (3-month terms common), exposing earnings directly to market swings without extensive long-term price protection mechanisms.

The business model thus requires active risk management balancing sales exposure against customer credit profiles; the firm selectively enters natural gas swaps primarily for input cost hedging though not extensively for coal price risk mitigation [S1].

Recent industry analyses highlight dual pressures: upward steel demand from infrastructure spending juxtaposed with substitution risks as alternative metallic products or electric arc furnace methods gain share [N9]. Warrior Met must maneuver carefully within these shifting cycles.

Regulatory & Environmental Risks: Challenges on the Horizon

Federal coal lease acquisitions signed late in 2025 expand Warrior Met’s exclusive rights over substantial acreage—8,346 acres at Mine No.1 and another 5,704 acres at Mine No.4—with estimated recoverable reserves topping nearly 48 million metric tons combined [S1]. While these leases extend operational longevity, they also introduce compliance obligations aligned with Bureau of Land Management oversight.

Environmental regulations continue tightening amid broader energy transition pressures capturing governmental scrutiny over fossil fuel extraction impacts. Concurrently, corporate tax treatment nuances such as valuation allowances against deferred tax assets—particularly state-level deferred credits amounting to ~$45 million—signal caution on future tax benefit realizations given legislative changes like repeal of Alabama's "throwback rule" [S1].

These factors compound capital intensity challenges inherent to mining initiatives demanding vigilant cost control alongside environmental stewardship.

Leadership Moves and Insider Activity: Signals from the Top

In January 2026, Warrior Met's CEO divested shares valued at about $10 million—a notable insider transaction occurring amid operational scale-up phases [N2]. Such insider activity juxtaposed against existing equity incentive plans outlined within SEC disclosures suggests a nuanced balance between liquidity actions by management and structured retention mechanisms designed to secure key talent [S1].

This dynamic signals potentially mixed management perspectives: optimizing personal portfolio positions while affirming commitment towards long-term operational execution through incentivization frameworks.

Options Market Debut: What Increased Trading Interest Suggests

January marked the introduction of HCC options contracts commencing March expiration dates—a development indicating growing derivative market participation possibly fueled by both speculative appetite and tactical hedging needs [N6][N7].

Noteworthy option trades observed during this period convey investor engagement reflecting anticipation around critical catalysts such as Blue Creek output ramp-up, earnings momentum, or commodity price trajectory shifts. This added layer of market interest enriches price discovery albeit introducing volatility dimensions warranting monitoring.

Conclusion: Strategic Positioning in a Transitional Industry

Warrior Met Coal occupies a strategically defensible niche anchored by high-quality Appalachian metallurgical coal reserves coupled with low cost structures enhanced decisively by early Blue Creek mine ramping. The company's financial profile rooted in solid liquidity and improving profitability underpins operational agility essential amid cyclical steelmaking commodity markets.

That said, inherent sector cyclicality paired with evolving regulatory environments invites ongoing risk calibration—particularly surrounding coal pricing exposure, environmental compliance costs, and tax asset usability uncertainties.

Management moves alongside emerging options market trends further underscore increased scrutiny from sophisticated investors navigating this transitional phase of the steel raw materials supply chain.

Ultimately, Warrior Met’s outlook embodies the tension between asset-driven competitive advantage enabling growth trajectories versus external macro factors requiring adaptive resilience.

Disclaimer: This analysis is provided for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments