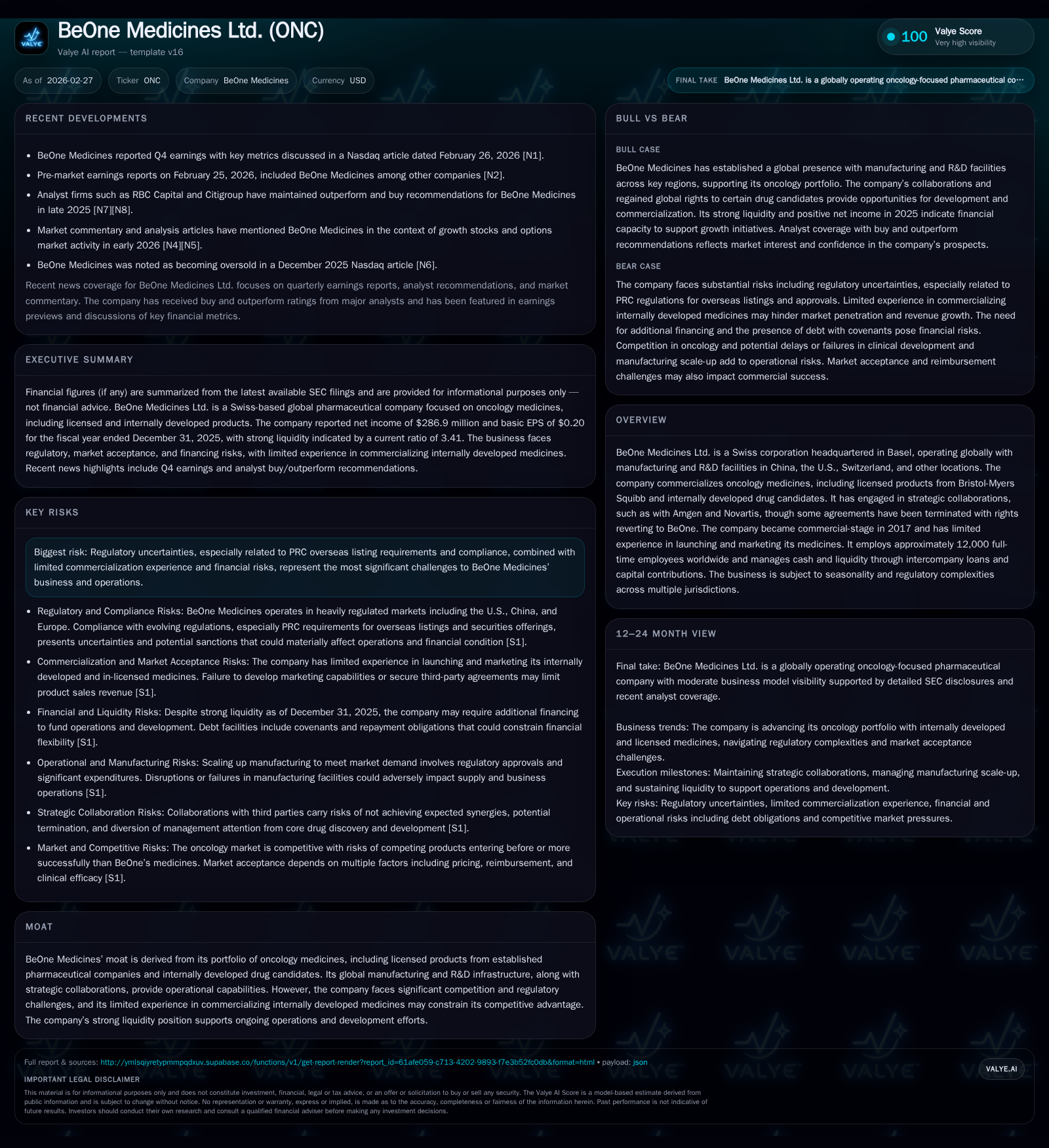

BeOne Medicines Ltd. Returns to Profitability with Operational Turnaround Amid Regulatory and Commercial Challenges

The Swiss oncology company achieved positive net income in 2025 after years of losses, driven by commercialization progress and improved cash flow.

BeOne Medicines Ltd., a Swiss oncology pharmaceutical company with global manufacturing and R&D operations, reported a significant operational turnaround in 2025, recording net income of $287 million and positive operating cash flow of $1.13 billion after several years of deep losses. Its recovery was fueled by growing revenues from licensed and internally developed oncology medicines following its transition to a commercial-stage company in 2017. Nevertheless, the firm faces persistent risks including complex regulatory compliance across multiple jurisdictions—especially PRC overseas listing uncertainties—and challenges related to limited commercialization experience and competitive pressures. Liquidity remains strong with ample cash reserves supporting ongoing investment, but the business is sensitive to evolving drug pricing reforms in key markets and litigation risks that could impact future performance.

Historical Performance Overview

BeOne Medicines Ltd., headquartered in Basel, Switzerland, has evolved into a commercial-stage oncology pharmaceutical company since launching its first marketed products post-2017. The company’s revenue showed steep growth starting from fiscal year (FY) 2016 with only about $1 million, rising sharply to $18.2 million in FY2017 [F1]. Though the headline revenue number remains modest compared with large peers, this early commercial traction paired with licensed portfolios from Bristol-Myers Squibb (BMS) set the foundation for subsequent operational scale.

Notably, BeOne’s operating income turned dramatically positive in FY2025 at approximately $447 million after consecutive years of substantial operating losses (exceeding -$1 billion in FY2023) [F1]. Similarly, net income mirrored this turnaround, recording a profit of roughly $287 million in FY2025 versus prior multi-year deficits [F1]. This reflected improved efficiency and scale within their commercial operations combined with cost control.

Operating cash flow followed a comparable trajectory: from negative cash flows surpassing $1 billion annually in preceding years to a robust positive inflow of about $1.13 billion in FY2025 [F1]. Simultaneously, capital expenditures decelerated sharply—from over half a billion USD previously to just under $186 million—suggesting completion or downscaling of major building projects or platform investments [F1].

Historical performance (annual)

| FY | Net ($bn) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0.3 | 1128 | 447 | 186 | +144.5% |

| 2024 | -0.6 | -141 | -568 | 493 | +26.9% |

| 2023 | -0.9 | -1157 | -1208 | 562 | +56.0% |

| 2022 | -2.0 | -1497 | -1790 | 325 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 942 | 6.6 |

| 2024 | -633 | -19.4 |

| 2023 | -1719 | -24.9 |

| 2022 | -1822 | -45.7 |

Source: SEC companyfacts cache [F1].

Current Business Model and Growth Drivers

BeOne's moat pivots on its portfolio composed mainly of oncology medicines licensed primarily from established entities like Bristol-Myers Squibb alongside internally developed pipeline candidates. The firm's global footprint encompasses manufacturing and R&D centers strategically located across China, the U.S., Switzerland, among others, enabling access to diverse regulatory jurisdictions and expanded market opportunities .

The company propelled itself from early-stage development into full commercial operations post-2017 launch but retains relatively limited experience in fully launching and marketing innovative medicines independently—highlighting reliance on strategic collaborations for sales infrastructure [S1][S21]. Such collaborations have historically included partnerships with Amgen and Novartis; however some agreements were terminated returning rights back to BeOne .

Key growth catalysts include continued rollout of licensed products gaining physician adoption, leveraging expanded manufacturing capabilities for internal drug candidates progressing through clinical trials, plus potential new licensing deals capitalizing on established oncology expertise.

Conversely, growth may face constraints due to intense competition within oncology therapeutic areas where innovative therapy emergence is rapid globally. Additionally, penetration challenges might arise given the company's relative novelty as an independent marketer coupled with price sensitivity amid new reimbursement landscapes.

Regulatory Environment and Risks

The company's operations span highly regulated jurisdictions including the U.S., China (PRC), Europe, and other select markets where pharmaceutical product approval processes are lengthy and costly [S14]. Regulatory compliance uncertainty is amplified by evolving PRC oversight concerning overseas listings—a notable risk factor given BeOne’s cross-border capital structure involving ADSs listed on Nasdaq plus shares traded locally on Hong Kong and Shanghai exchanges—with ambiguous CSRC enforcement policies potentially affecting securities offerings or dividend repatriation [S1][S16].

Furthermore, BeOne faces ongoing regulatory risks including possible FDA enforcement concerning promotion practices—recent untitled letters concerning Brukinsa® and Tevimbra® promotional claims illustrate heightened scrutiny [S22]. The firm must navigate complex fraud-and-abuse statutes across multiple healthcare systems that impact sales activities [S4][S5]. Data privacy regimes globally add layers of operational complexity given sensitive patient information handled during clinical development and post-market surveillance [S10][S16].

Additionally, evolving U.S. drug pricing reforms such as Medicaid supplemental rebates tied to Most Favored Nation (MFN) pricing models under CMS initiatives (GLOBE and GUARD models scheduled for implementation from late-2026) threaten margin compression by mandating rebates if Medicare prices exceed international benchmarks [S15][S26][S27]. State-level affordability boards further complicate pricing strategies domestically.

Environmental health safety laws address hazardous material use in facilities with associated compliance costs—non-compliance risks can lead to sanctions or increased operating expenses [S6][S13]. Cybersecurity threats targeting proprietary assets pose another emergent risk given reliance on digital infrastructure [S13].

Legal Proceedings Impacting Market Exclusivity

BeOne is actively defending intellectual property through litigation critical for maintaining competitive positioning:

- A patent infringement suit filed versus Zydus Pharmaceuticals under Hatch-Waxman provisions challenges generic entry attempts against BeOne’s approved drugs signaling proactive protection of market exclusivity [S23].

- Separate litigation initiated by AbbVie alleges trade secret misappropriation concerning BTK degrader programs; although vigorously contested by BeOne this introduces litigation uncertainty potentially affecting pipeline progression or reputation [S23].

Successful defense outcomes are important as patent loss could erode market share rapidly given generic competition intensity typical within oncology segments.

Financial Position and Capital Allocation Strategy

As of December 31, 2025, BeOne reported a robust liquidity position with approximately $4.55 billion in cash and equivalents against current liabilities near $1.83 billion yielding a current ratio above 3.4—a healthy working capital buffer supporting operational flexibility [F1][S11].

The company employs intercompany loans and capital injections strategically between subsidiaries across geographies for treasury efficiency while adhering to jurisdictional banking regulations [S1]. Debt financing involves facilities totaling up to $2 billion with financial covenants focusing on leverage controls underscoring prudent capital management aligned with growth needs [S11][S12][S24].

Recent capex reductions signify investment phasing reflecting expansion cycles’ maturity—allowing freer cash flow generation toward reinvesting into both R&D pipelines or potential licensing deals rather than fixed assets buildup [F1].

Free cash flow approximates nearly $942 million as calculated by operating cash flow less capital expenditure providing meaningful internal funding capacity while preserving balance sheet strength [F1]. Return on equity stands modest at around 6.6% reflecting the company’s transition to profitability with scope for enhancement if earnings scale sustainably improves.

Outlook: Milestones & What to Watch

While no explicit forward guidance was provided at the time of latest filings or releases ([N1][N2][S3]), industry observers should track:

- Expansion success of internally developed clinical-stage oncology candidates entering late-stage trials or first approvals.

- Progression or new licensing collaborations that can unlock additional revenue streams or commercial capabilities.

- Resolution trajectories concerning patent litigations which could decisively influence competitive moat.

- Outcomes related to PRC regulatory clarity impacting cross-border financing abilities or operational constraints.

- Effects triggered by U.S. Medicare payment model implementations starting late-2026 notably impacting product net prices.

- Responses to FDA communications on promotional compliance as they may signal enhanced regulatory enforcement intensity affecting marketing freedom.

Given BeOne’s scale reduction from early losses paired with strengthening cash generation capacity plus existing global infrastructure footprint, it is positioned cautiously for growth subject to navigating inherent pharma sector risks outlined above.

Conclusion

BeOne Medicines Ltd.'s fiscal year ending December 2025 marked an inflection point transitioning from significant accumulated deficits into profitability fueled by increasing sales execution related mainly to licensed oncology therapies alongside controlled spending initiatives. The large cash reserves ensure runway for continued R&D investment while addressing operational scaling needs globally.

Nonetheless, executives face multifaceted challenges including steep regulatory hurdles especially regarding PRC listings compliance uncertainties; intense competitor dynamics common within oncology therapeutics; dependence on maintaining robust IP protection amid ongoing patent lawsuits; and impending healthcare policy reforms pressuring product pricing resilience particularly within the U.S. market.

Sophisticated risk controls combined with selective strategic collaborations will be critical as BeOne endeavors to fully realize its commercial potential beyond initial launch phases where limited internal marketing expertise currently caps upside prospects.

This analysis is informational only and does not constitute investment advice or recommendations regarding BeOne Medicines Ltd.'s securities or financial performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments