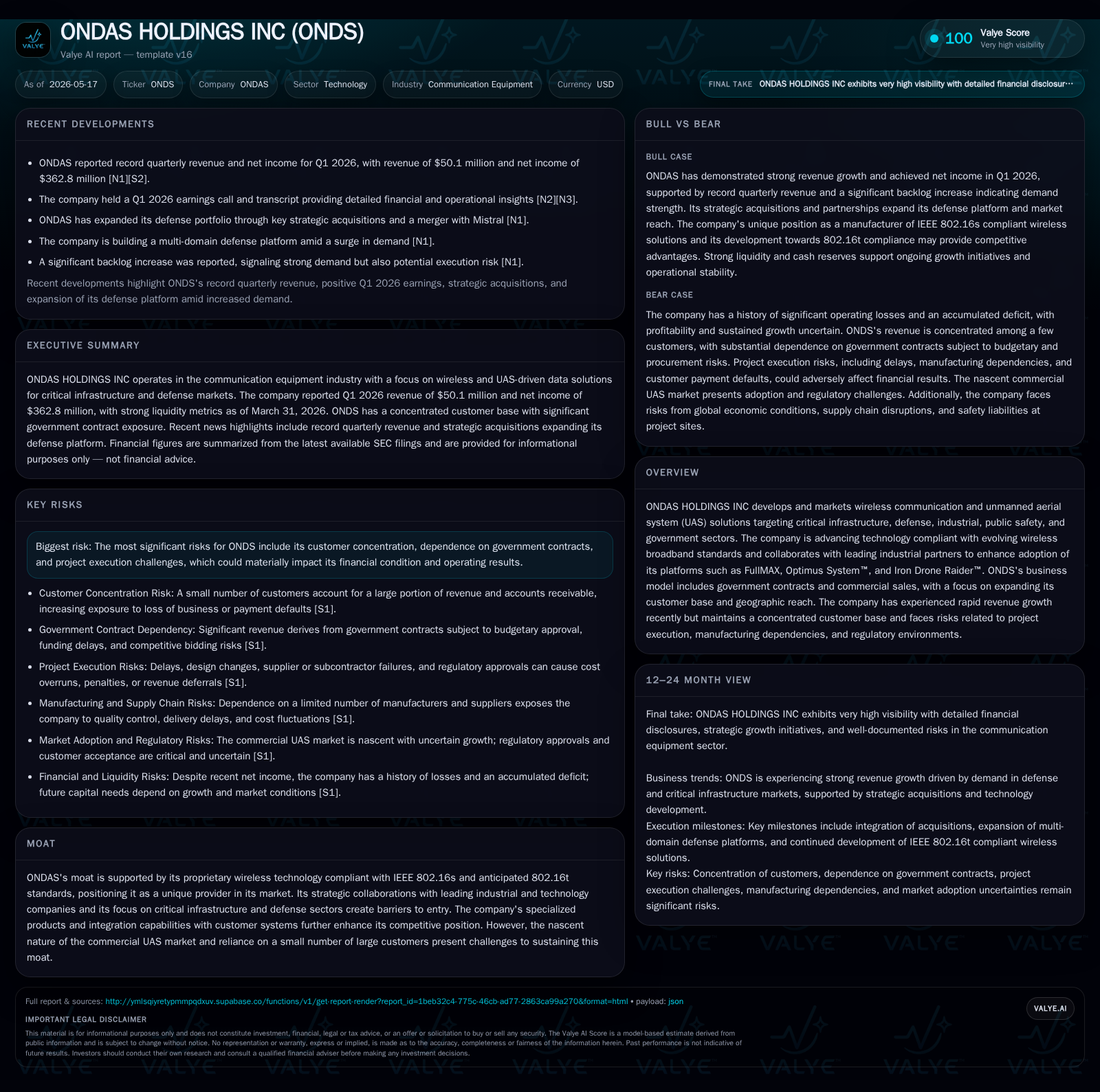

ONDAS HOLDINGS Accelerates Growth with Proprietary Wireless Solutions Amid Concentration Risks

Strong revenue growth driven by unique technology and strategic government contracts underscores ONDAS's market positioning.

ONDAS HOLDINGS INC's latest quarterly filing reveals robust momentum through expanding adoption of its wireless broadband and UAS platforms targeting critical infrastructure and defense sectors. The company's proprietary FullMAX technology and Iron Drone Raider systems underpin its competitive moat, supported by specialized applications and strict compliance with evolving industry standards. However, dependence on a limited set of large governmental customers and project execution risks remain significant challenges. Future growth hinges on diversifying the customer base, scaling manufacturing capabilities, and navigating regulatory landscapes while capitalizing on expanding demand for industrial wireless communications and autonomous drone solutions.

Recent Operating Update

ONDAS HOLDINGS INC's first quarter 2026 10-Q filing dated May 15, 2026 ([S2]) signals continued growth momentum with record quarterly revenue that beat analyst estimates [N1][N3]. This recent surge underscores increasing adoption of ONDAS’s wireless broadband communication platforms and unmanned aerial system (UAS) solutions by its core government and industrial clients. While precise Q1 revenue figures are not itemized in the filing excerpt, the demonstrated expansion in customer engagements across transportation, defense, public safety, and critical infrastructure markets is clearly articulated [S2][N3]. Concurrently, an 8-K filed same day ([S3]) disclosed unregistered share issuances under Regulation D exemption, possibly funding ongoing capex or strategic initiatives.

This latest update confirms no material changes to previously disclosed risk factors ([S2]), reaffirming ongoing exposure to concentrated client dependence and project execution challenges as key near-term constraints.

Business Model Overview

ONDAS operates as a developer and marketer of specialized wireless communication systems leveraged primarily within mission-critical environments spanning defense, infrastructure utilities, public safety agencies, and government entities ([S1],[S4]). The company’s revenue model derives from hardware/software product sales (such as FullMAX radios), system integration services including Optimus System™, as well as UAS platforms exemplified by its Iron Drone Raider™ tactical drone solutions. These products are sold through government contracts often awarded via competitive bids alongside direct commercial engagements.

Revenue mechanics hinge on sizeable unit shipments coupled with recurring service contracts for maintenance and upgrades—all driven by volume demands primarily from large-scale critical infrastructure operators. Pricing dynamics reflect significant customization needs alongside adherence to stringent wireless broadband standards like IEEE 802.16s for secure long-range connectivity. This tailored approach creates relatively high switching costs for customers embedded into operational safety-networks.

Margins are influenced by mix shifts between hardware-intensive deployments versus higher-margin software-service components. Operationally, ONDAS invests heavily in R&D to maintain technology leadership while managing supplier relationships during semiconductor component scarcity ([S28]). Strategic partnerships with leading industrial entities augment product capabilities enhancing ONDAS’s value proposition.

Industry Structure and Competitive Position

The Communication Equipment industry segment ONDAS occupies is characterized by rapid technological evolution alongside intense regulatory oversight. Within this niche—wireless broadband for critical infrastructure combined with UAS—the company occupies a distinct competitive space due to its proprietary FullMAX technology compliant with IEEE standards ([F1],[S1]). This positioning offers a moat bolstered by integration complexity and sector-specialized design tuned for harsh operating conditions.

Competitively, ONDAS contends with established network equipment manufacturers as well as emerging drone technology firms. Its advantage lies in vertically integrated offerings uniquely tailored to government procurement requirements coupled with extensive field support capabilities ([S4],[S5]). Nonetheless, the nascent commercial UAS market introduces both opportunity and uncertainty given evolving standards and customer adoption curves.

Customer concentration remains a structural issue; two customers accounted for approximately 66% of revenue during 2025 ([S4],[S5]), exposing financial vulnerability should large contract renewals falter. Government procurement cycles exert additional pressure requiring sustained investment in proposal development and compliance readiness.

Growth Drivers

- Expanding Government Spending on Infrastructure Security: Heightened focus on securing energy grids, transportation networks, and border areas fuels demand for robust wireless communication gear tailored for critical operations ([F1],[S4]).

- Advancing UAS Integration: ONDAS’s Iron Drone Raider™ platform taps growth in autonomous surveillance/detection missions increasingly prevalent across defense/public safety domains.

- Broadening Geographic Footprint: Strategic market entry into international regions with unmet infrastructure communication needs represents a medium-term growth vector.

- Technology Leadership: Continuous enhancement of proprietary standards-compliant wireless systems supports upselling opportunities and long-term customer retention.

- Partnership Ecosystem: Collaborations with industrial partners enhance solution breadth enabling cross-market penetration beyond existing governmental anchors.

Key KPIs to monitor include backlog expansion reflecting booked contracts ([N14]), new customer acquisitions metrics against retention rates ([S4]), order pipeline growth from commercial segments ([N3]), as well as successful deployment milestones in new territories.

Risks and Watchpoints

- Significant Customer Concentration: Heavy reliance on a handful of clients poses revenue volatility risk if contracts are delayed or cancelled ([S4],[S5]).

- Project Execution Challenges: Complex integration projects lead to potential schedule slips or cost overruns impacting margins ([N14]).

- Manufacturing Dependencies: Supply chain disruptions especially semiconductor shortages could delay product deliveries compromising contractual obligations ([S28]).

- Regulatory Compliance Burden: Product safety laws, data protection statutes covering AI-enabled drones impose continuous compliance costs which may intensify with evolving global norms ([S22],[S27],[S28]).

- Operating Losses Despite Growth: Historical net losses remain substantial limiting cash flow generation despite strong liquidity buffer ([F1],[S1]).

- Litigation Exposure: Intellectual property risks inherent to communications tech could result in costly disputes impacting reputation or product availability ([S26]).

What To Watch Next

Investors should track forthcoming contract awards announced in government spending budgets responsive to infrastructure modernization trends [N11], progress on reducing single-customer dependency through pipeline diversification efforts [N14], updates on deployment outcomes from new geographic markets [N3], cadence of product innovation announcements especially around IEEE standard enhancements [N2], potential acquisitions aimed at broadening technical capabilities or distribution reach [S10]. Financially, quarterly releases will shed light on margin trajectory improvements amid scale-up [N3], cash burn trends relative to operating activities [F1], as well as any changes in capital structure via equity issuance or debt draws [S3].

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1026mm | |

| 2026-03-31 | ||

| Current assets | $1629mm | |

| 2026-03-31 | ||

| Current liabilities | $149mm | |

| 2026-03-31 | ||

| Current ratio | 10.91x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | 1,026,003,000 | |

| 2026-03-31 | ||

| Total Debt | 500,000 | |

| 2023-03-31 | ||

| Current Assets | 1,629,196,000 | |

| 2026-03-31 | ||

| Current Liabilities | 149,317,000 | |

| 2026-03-31 | ||

| Current Ratio | ~10.9 | |

| 2026-03-31 |

The notable cash reserve exceeding $1 billion provides a substantial runway for ONDAS's aggressive R&D investments despite the continuing operating losses reported through FY2025 of approximately $58 million operating income loss ([F1]). The negligible debt load indicates low leverage risk but also reflects the company's reliance on equity financing for growth capital. The exceptional current ratio signals strong short-term liquidity mitigating immediate solvency concerns [F1].

This analysis synthesizes publicly available filings without providing any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments