OneMeta’s VerbumSuite Amplifies Real-Time AI Translation Amid Enterprise Privacy Push

OneMeta advances its AI-driven multilingual platform targeting enterprises demanding secure, on-premise solutions despite significant liquidity pressures.

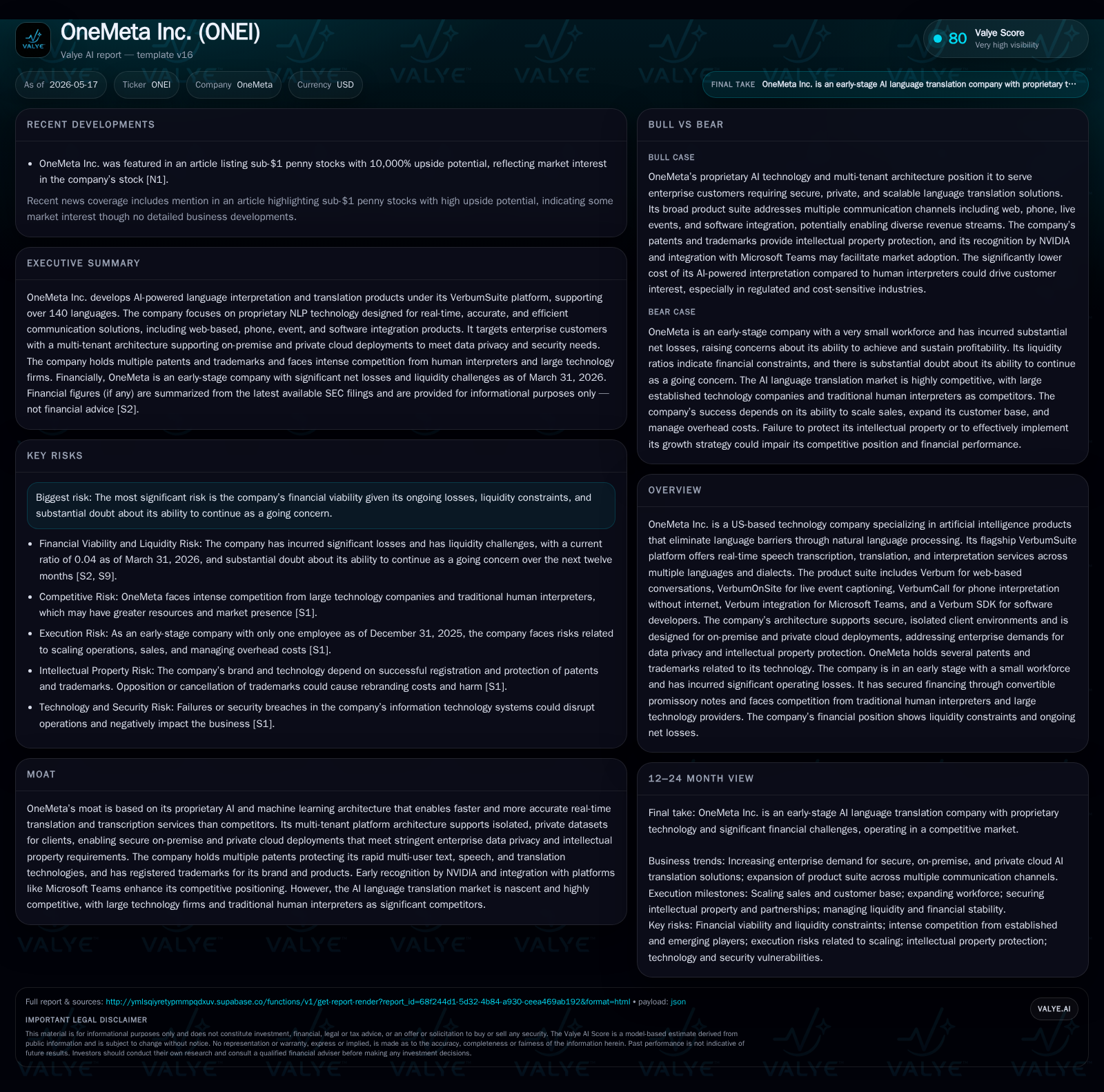

The latest 10-Q filing reveals OneMeta’s issuance of a warrant to Avaya as a capital-raising effort amid ongoing financial challenges. The company’s VerbumSuite leverages proprietary AI to provide real-time translation and transcription with a focus on data privacy and secure deployments tailored for regulated industries. Despite an early moat supported by patented technology and strategic partnerships, the company faces substantial liquidity constraints and intense competition from both established tech giants and emerging startups. Key growth drivers include enterprise demand for sovereign AI solutions and SDK expansion, but execution risks remain elevated. Upcoming milestones center on customer traction validation and effective capital management.

Latest Operating Developments: Capital Moves and Market Signals

In an April 9 transaction detailed in an 8-K filing, the Company issued a warrant to Avaya LLC granting rights to purchase over 22 million common shares at an exercise price of $0.135 per share exercisable over ten years [S2][S3]. This low exercise price combined with demand and piggyback registration rights signals an urgent need for capital infusion during persistent financial strain. The warrant extends Avaya observer rights at the board level—a strategic alignment that may open further collaboration opportunities but also denotes investor oversight under pressure.

While no direct refinancing or debt restructuring was reported in the quarter, ongoing mentions of substantial doubt about OneMeta’s ability to continue as a going concern stress the precarious nature of its capital position [S1]. This context frames all operational strides against a backdrop of significant financing risk.

Business Model & Product Suite: VerbumSuite as a Language AI Bridge

Originating from Metalanguage Corp’s IP acquired mid-2022, OneMeta operates primarily through its VerbumSuite—an AI-powered language services platform aiming to eliminate communication barriers via cutting-edge natural language processing (NLP) [S1]. The product family includes Verbum for web conversations, VerbumOnSite for live event captioning, VerbumCall offering phoneline interpretation without internet dependency, an integration module for Microsoft Teams, plus a software development kit (SDK) allowing third-party platforms to embed Verbum functionalities seamlessly

Revenue generation fundamentally relies on enterprise clients subscribing or licensing these AI services to handle real-time multilingual transcription, translation, and interpretation across more than 140 languages. Pricing likely incorporates factors such as volume usage in minutes or events, pricing tiers based on deployment method (cloud versus on-premise), and bespoke contractual arrangements considering complexity or privacy needs. Margins depend heavily on maintaining proprietary model efficiency and optimizing hosting costs while scaling user adoption.

Differentiation springs from deeply integrated AI models designed for speed and accuracy exceeding general-purpose translation APIs. Customer verticals targeted include regulated environments—government agencies, financial services, healthcare—as well as education institutions and customer support centers where lapses in timely translation can degrade operational effectiveness or compliance.

Enterprise Demand Shapes Secure On-Premise and Private Cloud Deployments

Enterprise customers are increasingly wary of third-party cloud solutions due to rising concerns over data sovereignty, intellectual property leakage risks, and unpredictable costs tied to large public cloud vendors deploying AI workloads. OneMeta has architected its platform from inception to accommodate multi-tenant environments segmented into isolated datasets per client or sub-client—a capability vital for clients handling sensitive information [S1].

This architectural choice enables secure on-premise installation or deployment within private clouds, aligning well with sovereign AI trends where localized data processing complies with regulatory frameworks mandating strict control over data residency and usage.

This emphasis not only meets stringent security standards but also provides cost predictability by leveraging dedicated infrastructure rather than shared public cloud billing models sensitive to request volume spikes common in AI inference workloads.

Competitive Positioning: Early Moat in Proprietary AI and Data Isolation

OneMeta’s IP portfolio includes several key patents governing rapid multi-user NLP workflows for text-to-speech translation services distinguishing it technologically from commoditized translation APIs offered by large cloud providers or open-source projects [S1]. These protections underpin its claim of superior speed and accuracy.

The company has attracted acknowledgment from NVIDIA specifically referencing its technological approach within broader initiatives centered on AI media localization ecosystems—this offers third-party validation endorsing OneMeta’s technical credibility.

Yet this moat sits atop an intensely competitive landscape where entrenched tech giants possess extensive R&D budgets; additionally, traditional human interpreters still dominate complex scenarios resisting full automation. Smaller startups also threaten disruption with niche capabilities or aggressive pricing.

Growth Drivers: Enterprise Adoption, Sovereign AI Trends, and SDK Ecosystem Expansion

Demand drivers strongly reflect macro trends driving enterprise AI investment generally but filtered through the lens of data privacy requirements unique to multilingual communication services. Increasing regulatory focus heightens urgency among target clients to adopt solutions hosting critical information inside controlled environments rather than exposing it externally.

Moreover, growing interest in sovereign AI frameworks requiring localized model training runs dovetails effectively with OneMeta’s platform architecture supporting such segmentation.

From an ecosystem perspective, the Verbum SDK empowers software developers to embed language capabilities directly into their applications fostering network effects as more platforms become interoperable with OneMeta’s core NLP engines thereby reinforcing customer retention through embedded switching costs.

Near-term KPIs worth monitoring include securing contracts within regulated sectors signaling trust in security features; ramping usage volumes evidencing genuine adoption; expanding product integrations; and possible new releases enhancing functionality or improving user experience metrics.

Risks & Constraints: Financial Viability, Intense Competition, and Adoption Hurdles

Despite promising technology positioning, OneMeta remains financially fragile. Its net losses approached $3.8 million in 2025 with minimal top-line revenue accumulating slowly during early commercialization phases [F1][S1]. The financial snapshot as of March 31, 2026 reveals cash equivalents at approximately $186 thousand balanced against current liabilities over $6.3 million reflecting acute liquidity stress that impairs operational flexibility [F1].

Competition from resource-rich incumbents deploying massive scale NLP models could undercut pricing power while accelerating feature innovation.

Additionally, transitioning from an early-stage development entity into a sustainable commercial operation involves overcoming hurdles related to market education on novel deployment architectures (on-prem/private cloud), customer acquisition costs higher than typical SaaS models due to implementation complexities, plus managing overhead prudently under constrained funding conditions.

Next Steps for Investors: Key Milestones and Market Validation Indicators

Critical near-term milestones providing validation will revolve around demonstrable increases in recurring revenue from enterprise accounts particularly those in regulated industries which reflect acceptance of secure deployment models.

Closely linked are success metrics regarding SDK uptake signaling widening ecosystem footprints enhancing competitive resiliency.

Capital structure developments including potential conversions or exercises related to the recently issued warrants will materially affect cash availability moving forward. Monitoring quarterly bookings progression versus operating expense trends will further illuminate pathway viability.

Financial Overview: Liquidity Profile and Loss Trends Highlight Viability Challenges

The financial snapshot as of March 31, 2026 reveals cash equivalents at approximately $186 thousand balanced against current liabilities over $6.3 million reflecting acute liquidity stress that impairs operational flexibility [F1]. Net income remains negative at roughly -$3.8 million for calendar year 2025 consistent with early-stage companies focusing on product development over profitability [F1][S1]. In sum, despite advanced technology offerings and strategic positioning within niche enterprise segments emphasizing privacy-sensitive deployments, the company faces a precarious capital situation necessitating tangible progress on revenue growth coupled with careful expense management if it is to transform toward sustainable operations.

Disclaimer: This analysis is based solely on publicly filed regulatory documents up through May 17, 2026. It aims to provide a comprehensive understanding of OneMeta Inc.’s recent developments and business context without offering investment research views or forecasts.

Financial position in context

Current assets of $243,519 and current liabilities of over $6.3 million imply a current ratio near 0.04x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments