OptimumBank Holdings' Strategic Growth Through Niche Lending and Digital Expansion

OptimumBank leverages its South Florida real estate focus and targeted digital upgrades to navigate competitive pressures and regulatory demands.

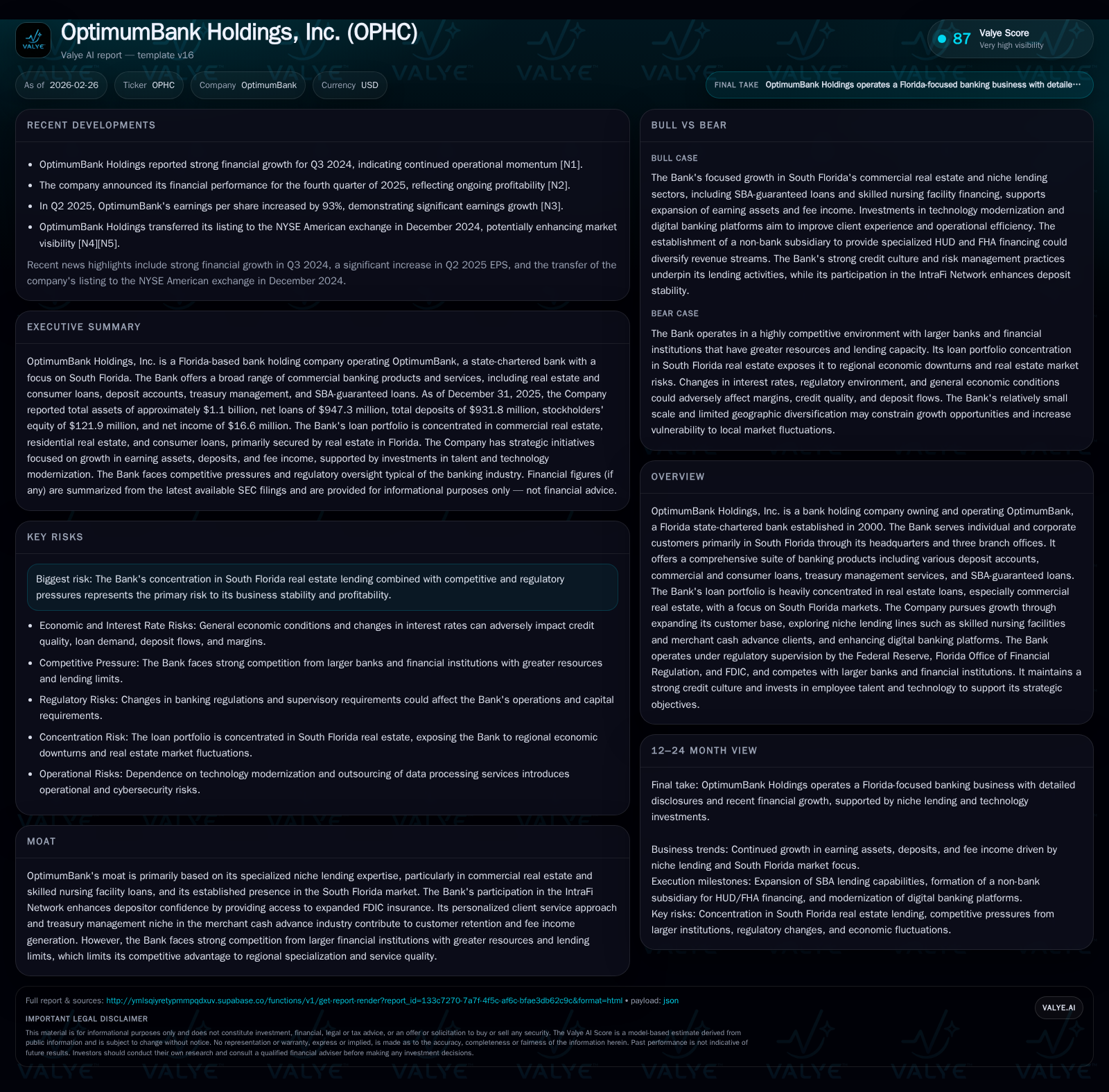

OptimumBank Holdings, Inc., a Florida state-chartered bank holding company, has demonstrated robust financial growth driven primarily by its specialized niche lending in commercial real estate, skilled nursing facilities, and merchant cash advance clients. The bank’s strategic investment in digital banking modernization aims to enhance customer experience and operational efficiency, supporting its efforts to expand deposit bases and diversify loan portfolios within and beyond South Florida. While the concentrated geographic exposure poses risks amid intensifying competition and regulatory scrutiny, OptimumBank maintains solid capital adequacy and efficient equity utilization reflected in a 13.7% ROE for 2025.

Historic Financial Performance: Robust Growth Amidst Regional Exposure

Since its establishment as a Florida state-chartered bank in 2000, OptimumBank has steadily grown its financial base with a keen focus on niche lending markets in South Florida. The company realized net income of $16.6 million in fiscal year (FY) 2025, marking a significant 26.9% increase over the prior year’s $13.1 million [F1]. This acceleration accompanied a 14.3% rise in operating cash flow, which reached $17.8 million in the same period [F1], underscoring strong core cash generation.

Despite this growth momentum, capital expenditures remained restrained at under $900,000 in FY2025, representing a slight decline of approximately 9.3% compared to the previous year [F1]. This moderation suggests operational efficiencies or limited need for major physical expansion amid ongoing technology investments elsewhere in the bank’s footprint.

Equity growth was particularly striking—rising from about $70 million at end-2023 to just under $122 million at end-2025 [F1]. Coupled with the sustained rise in net income, this expansion pushed an approximate return on equity (ROE) of 13.7% for the latest fiscal year [F1], indicative of effective deployment of shareholder capital.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 17 | 18 | 896000 | +26.9% |

| 2024 | 13 | 16 | 988000 | +108.9% |

| 2023 | 6 | 7 | 668000 | +56.2% |

| 2022 | 4 | 10 | 322000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 17 | 13.7 |

| 2024 | 15 | 12.7 |

| 2023 | 6 | 9.0 |

| 2022 | 10 | 6.4 |

Source: SEC companyfacts cache [F1].

This table encapsulates OptimumBank's strong trajectory across profitability metrics alongside sizable equity build-up supporting asset growth.

Niche Lending Expertise as the Growth Engine: Skilled Nursing and Merchant Cash Advances

At the core of OptimumBank's competitive advantage lies its concentration on real-estate-backed lending within South Florida’s commercial property sector—70% of its $947 million total loan portfolio comprises commercial real estate loans as of December 31, 2025 [S6]. Overall mortgage-secured loans represented approximately 95% of total loans funded [S6], underscoring reliance on collateralized credit.

Of particular note is the bank’s expertise serving skilled nursing facilities through specialized loan products including owner-occupied commercial real estate mortgages and asset-based lines of credit secured by accounts receivable [S10]. Management’s deep involvement bolsters underwriting quality tailored to this healthcare subsector.

Further extending portfolio diversification and fee-based revenue streams is the bank’s engagement with Small Business Administration (SBA) guaranteed loans since late 2023—earning Preferred Lender status early in 2025—which supports broader SME client penetration within South Florida’s economic landscape [S10]. The SBA segment aids diversification beyond traditional CRE exposure.

Complementing lending specialization is OptimumBank's unique position providing treasury management services focused on merchant cash advance (MCA) providers—a niche segment requiring handling of high-volume ACH transactions tied to alternative funding sources [S5]. This vertical contributes low-cost core deposits alongside noninterest fee income.

The MCA line entails complex operational demands; hence ongoing investments aim to automate these processes further to drive incremental efficiency gains throughout calendar year 2026 [S5].

Digital Modernization: Upgrading Core Systems for Customer Experience and Efficiency

To underpin both growth ambitions and tighten risk controls amidst evolving credit administration requirements [S6], OptimumBank has embarked on upgrading its core banking infrastructure along with enhancing mobile and online banking platforms.

These modernization efforts bolster several fronts: expanding branch utilization efficiencies; facilitating seamless remote deposit capture; improving electronic funds transfer security through soft token technologies; and better servicing treasury management clients particularly within MCA operations involving large ACH volumes [S6],[S8].

Given that regional banks like Optimum rely heavily on personal relationships but must also compete technologically against larger peers with sophisticated digital offerings—these initiatives will be critical for client retention and attracting digitally savvy small business customers.

Balancing Opportunities and Constraints: Competitive Landscape and Regulatory Outlook

OptimumBank operates within a highly competitive environment characterized by established multi-branch institutions possessing significantly greater resources and lending capacity; alongside nonbank competitors benefiting from lighter regulatory oversight [S8]. This dynamic constrains pricing power especially on loan yields amid fluctuating interest rate environments.

Furthermore, geographic concentration risk remains material: over three-quarters of lending exposure centers within South Florida's cyclical real estate market—including Broward and Miami-Dade counties—with notable sensitivity to regional economic shifts [S4],[S14]. This exposes OptimumBank to potential credit quality deterioration should local downturns materialize.

On the regulatory front the Bank is supervised by both the Federal Reserve as parent company holding entity and Florida Office of Financial Regulation at the bank level [S13]. It adheres to stringent capital adequacy guidelines showing capital ratios safely above well-capitalized thresholds as of December 31, 2025 [S7]. Compliance demands extend into extensive anti-money laundering controls mandated under USA Patriot Act provisions affecting customer verification systems [S21].

Interest rate volatility poses earnings margin risk given substantial variable-rate mortgage components adjusting annually after three-to-five year floors—a feature typical of community bank CRE portfolios but susceptible to rate shocks impacting borrower repayment capacity [S4].

Capital Structure Strength and Deployment: Equity Growth, Cash Flows, and Capital Allocation

Capital adequacy forms a pillar supporting sustainable lending practices at OptimumBank. Tier 1 capital ratio versus total assets reached roughly 11.4% at end-2025 versus regulatory minimum near 9%, highlighting solid buffer against stress scenarios [S7]. Total stockholders’ equity rose significantly from ~$70 million at end-2023 to nearly $122 million two years later reflecting profitable reinvestment strategies combined with limited dividend distribution activity [F1],[S26].

Dividend payments have been negligible with only one-time payout totaling $500k recorded during FY25 from the bank to holding company level—illustrating retained earnings allocation toward balance sheet fortification rather than shareholder returns currently constrained by regulator-imposed dividend limitations under FDIC rules when capital levels or earnings are stressed [S26].

Operating free cash flow approximated $16.9 million last fiscal year calculated as operating cash flow less capex represents ample internal liquidity generation capable of funding incremental loan growth without recourse to costly external financing or dilutive equity raises [F1].

Absent explicit buyback programs reported through SEC filings highlights continued preference for strengthening capital metrics while investing selectively across business development teams particularly targeting experienced talent procurement aligned with strategic lending initiatives [S6].

What Investors Should Monitor: Future Catalysts and Risk Factors

Looking forward key milestones include:

- Execution progress on digital platform modernization expected to drive improved fee income capture especially within merchant cash advance treasury services that depend heavily on scalable transaction automation capacities [N2],[S6].

- Expansion trajectory into diversified loan sectors beyond core South Florida CRE markets potentially via out-of-area lending subject to stringent due diligence protocols seeking yield enhancement without compromising credit quality standards established internally over decades of regional market experience [S10],[N1].

- Deposit base diversification efforts extending into interstate markets achieving greater resilience against localized economic cycles—a vital consideration given current ~103% loan-to-deposit ratio signaling lean liquidity cushions requiring careful funding management [S6].

- Any shifts emerging from evolving federal or state regulatory frameworks impacting interest rate margins or compliance costs particularly consumer financial protection mandates monitored continuously due to their potential impact on operational expense profiles [S18].

- Maintaining rigorous underwriting discipline amid intensifying competition highlighted by cautious credit administration processes emphasizing risk-adjusted returns balanced against growth objectives communicated throughout recent annual disclosures [S5],[N2].

Investors may also track developments related to OptimumFunding LLC—new wholly owned non-bank subsidiary launched early 2026 designed to unlock bridge HUD/FHA multifamily financing capabilities enabling longer-term refinancing solutions for healthcare-related real estate supporting niche skilled nursing facility loans previously emphasized as strategic growth pillars by management [S3],[S10],[N2].

In conclusion OptimumBank Holdings manifests a classic regional community bank leveraging domain expertise in real estate-centric lending complemented by nascent yet strategic diversification into SBA-guaranteed credit lines plus business-focused treasury management niches sustained through meaningful digital investments. While concentrated exposure tempers risk appetite amid aggressive market competition compounded by regulatory complexities,the firm exhibits prudent capital stewardship combined with operational agility which could underpin continued profitability stability provided execution risks remain contained.

This analysis is based solely on publicly available information referenced herein up to February 26th, 2026. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments