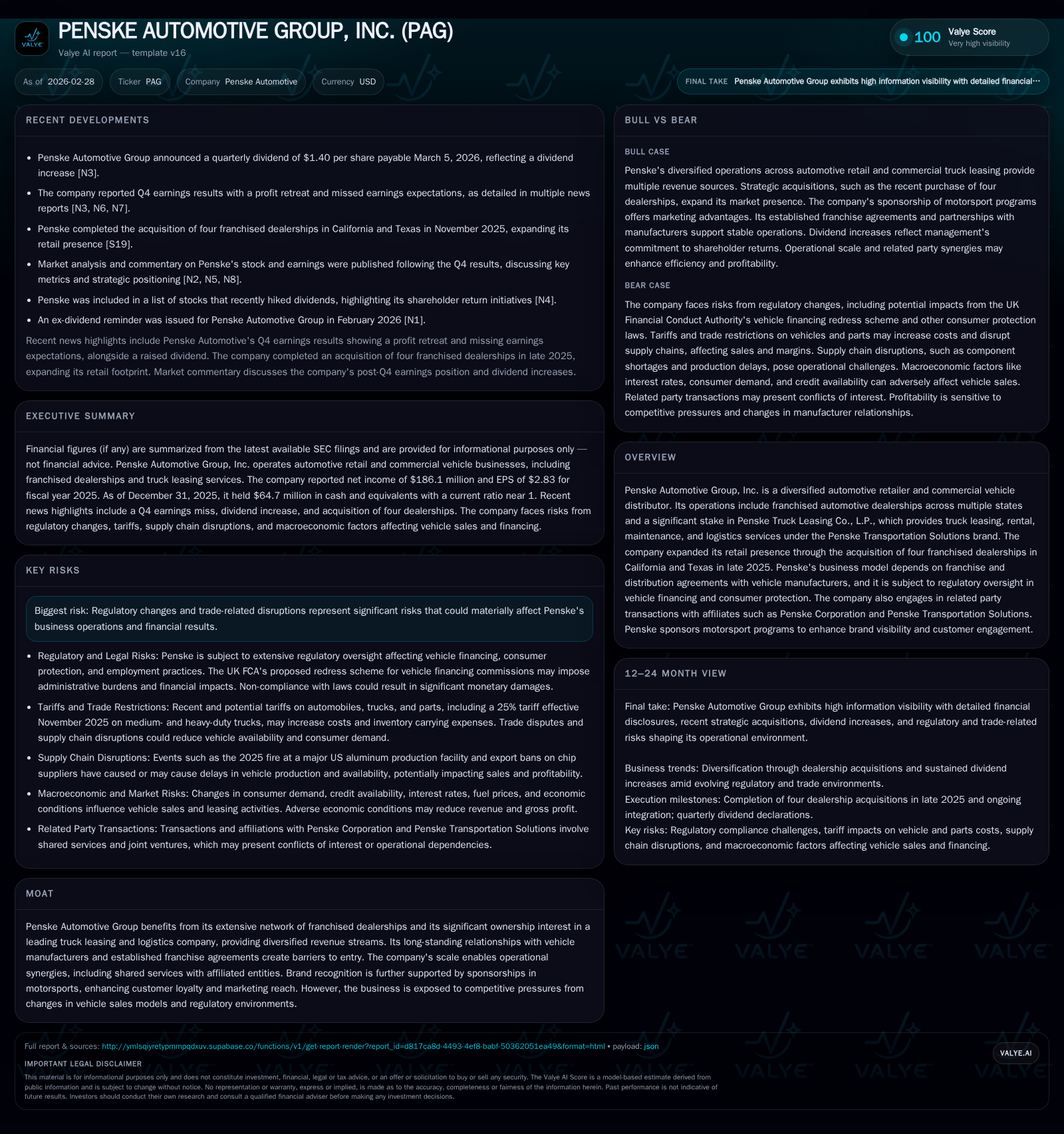

Penske Automotive Group's Financial Crossroads and Growth Path in 2026

Analyzing how Penske’s dealership acquisitions and diversified truck leasing stake sustain growth amidst regulatory and market challenges.

Penske Automotive Group posted revenue growth in 2025 driven by acquisitions, reaching $31.8 billion, but faced marked declines in net income amid margin pressures. The company strategically expanded its franchised dealership footprint across key U.S. markets, notably acquiring premium brand dealerships including Lexus locations in Florida, to diversify geographically and enhance revenue streams. Regulatory changes affecting EV incentives and commercial truck emissions present headwinds, particularly for the UK and heavy-duty sectors, impacting profitability and operational costs. Penske Transportation Solutions remains a critical earnings buffer with its large leased fleet, accounting for complementary stable revenue amid vehicle sales cyclicality. The company maintained solid cash flow generating positive free cash flow despite earnings softness, while adopting a cautious capital return approach with increased dividends but reduced share repurchases. Going forward, integration of recent acquisitions, adaptation to evolving regulatory landscapes, and management of financing and inventory will be key indicators of performance trajectory.

2025 Performance Snapshot: Revenue Gains, Profit Margin Pressures

In its full-year 2025 results, Penske Automotive Group reported total revenues of approximately $31.8 billion, up significantly due to acquisition activities including the late-year purchase of Penske Motor Group and several Lexus dealerships in Florida [S1]; this represented a notable expansion beyond the core retail automotive segment.

However, operating income declined by about 2.7% year-over-year to roughly $1.28 billion, while net income contracted nearly 80% to approximately $186 million [F1]. This dramatic profit retreat was attributed primarily to margin pressures across segments including retail automotive dealerships and heightened operational costs discussed in quarterly earnings commentary [N2][N13]. Revenue gains were thus accompanied by profitability headwinds stemming from a more challenging retail environment.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 186 | 975 | 1281 | 325 | -79.7% |

| 2024 | 919 | 1180 | 1317 | 369 | -12.8% |

| 2023 | 1053 | 1352 | 375 | -23.7% | |

| 2022 | 1380 | 1488 | 283 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 344 | 159 | 651 |

| 2024 | 274 | 59 | 811 |

| 2023 | 189 | 359 | |

| 2022 | 154 | 869 |

Source: SEC companyfacts cache [F1].

Sources: [F1]

Dealership Growth and Geographic Diversification: Acquisition Highlights

Penske’s strategic acquisitions underpinning volume growth include the acquisition on November 19, 2025 of Penske Motor Group LLC (PMG), comprising two Lexus and two Toyota dealerships in California and Texas with an expected annualized revenue contribution near $1.5 billion [S1]. Additionally, early in February 2026 the company acquired two Lexus dealerships in Orlando metropolitan area further strengthening its premium brand presence [N9].

The portfolio features over 40 vehicle brands with a premium mix—71% of dealership revenue in retail automotive comes from luxury brands like Audi, BMW, Lexus, Mercedes-Benz, Porsche—while geographical revenue split remains roughly balanced at about 61% U.S./Puerto Rico to 39% international (mainly UK) operations [S1]. This mix reflects Penske's focus on high-margin franchises complemented by continued expansion in select U.S. states crucial for volume capture.

The common-control acquisition accounting of PMG highlights internal alignment yet also means historical performance is consolidated from acquisition dates impacting comparability [S17]. Alongside new openings (eight franchise locations for Geely/Chery brands at existing UK sites), these moves illustrate ongoing footprint rationalization aimed at optimizing matched capacity between premium demand areas and localized brand appeal.

Regulatory Impact on EV Adoption and Commercial Truck Markets

Regulation represents a significant operational factor altering Penske’s vehicle mix economics both domestically and abroad. The U.S. phased out its $7,500 federal EV tax incentive as of September 30, 2025 [S1], suppressing electric vehicle sales momentum during Q4 and shifting manufacturer production towards combustion engines.

Conversely, the UK enforces progressively tighter mandates requiring that by early 2026 at least one-third of new car sales be electric vehicles under penalty schemes targeting non-compliance [S1]. The UK also plans bans on new ICE vehicles starting from model years ending between 2030-2035 with some hybrid allowances extending longer which pressures profitability margins within those retail operations impacted by evolving compliance costs.

Commercial heavy-duty trucks—a substantial product line for Premier Truck Group (PTG)—will face increasingly stringent emissions standards effective model year 2027 onward affecting both PTG dealership sales profiles and Penske Transportation Solutions' (PTS) rental/leasing fleets [S1][S4]. These regulations introduce risks via elevated maintenance expenses due to complex powertrain technologies plus residual value uncertainty as electrification accelerates fleet turnover assumptions.

Sector terminology critical here includes 'floor plan financing' typical for new vehicle inventory funding across dealerships; Penske’s UK franchise units partially operate under an 'agency sales model' where vehicles are sold directly by manufacturers through dealers earning fees rather than holding inventory liability [S1]. This evolution mitigates carrying costs but compresses revenue recognition profiles posing margin management challenges.

Penske Transportation Solutions: Key to Revenue Diversification

Holding approximately a 28.9% interest in Penske Truck Leasing Co., L.P., known collectively as Penske Transportation Solutions (PTS), Penkse Automotive secures diversified revenues complementary to cyclical retail automotive operations [S1]. PTS oversees one of North America’s largest tractor-trailer fleets totaling over roughly ~397,000 units providing leasing, rental maintenance along with logistics outsourcing [S19].

Though PTS operates independently with majority ownership by Penske Corporation (PC), PAG’s minority equity stake grants meaningful governance rights including board representation by PAG executives [S19]. PTS offers resilience amid wholesale vehicle sales volatility by deriving steady earnings through contractual fleet services offering predictable cash flow streams even during downturns.

Operational synergies emerge from shared services agreements between PAG dealerships and PTS subsidiaries facilitating efficiencies such as cross-utilization of maintenance facilities or leveraged procurement leveraging group scale advantages [S16]. Notably PTG facilitates finance arrangements for certain used truck sales centers generating incremental commissions supporting segment margins further illustrating interbusiness connectivity within the group.

Financial Health Analysis: Cash Flow Trends, ROE, and Capital Structure

Despite pressure on net earnings margins during fiscal year ending December 31 2025,[F1] shows Penske generated solid operating cash flow (CFO) of approximately $975 million against capex spending near $325 million yielding positive free cash flow around $650 million.

Cash flow intensity is heavily influenced by fluctuations in 'floor plan notes payable,' short-term liabilities used extensively for dealer inventory finance typically recorded within operating activities but functionally linked to working capital movements complicating pure CFO interpretation [S1][S11]. The company presents reconciliations clarifying adjusted operating cash flows including all floor plan impacts showing slight moderation YoY consistent with tighter industry financing availability.[F1]

Balance sheet liquidity measures a current ratio just under one – approximately .99 – signifying close matching of short term assets against liabilities reflective of lean working capital deployment necessitated by inventory financing requirements albeit signaling limited buffer against liquidity shocks.[F1]

Equity base advanced steadily from roughly $4.15 billion in FY22 to over $5.56 billion at end-FY25 demonstrating retained earnings accumulation augmented by equity issuances tied to acquisitions.[F1] Approximate Return on Equity (ROE) based on trailing year figures stands low near mid-single digits (~3.3%) on compressed net income despite solid operating returns evidencing shrinkage due primarily to extraordinary items or amortization arising from deals.[F1]

Capital Allocation Strategy: Dividends, Share Repurchases, and Capex Discipline

Penske maintained disciplined capital allocation during rising uncertainty; dividends paid increased strongly reaching nearly $344 million in FY25 up almost a quarter versus prior year reflecting confidence in long-term cash generation ability even as core earnings dipped substantially.[F1][N2]

Conversely share repurchases scaled down materially compared with preceding years falling back from highs of hundreds of millions annually down to around $159 million reflecting a more conservative stance amid margin pressure backdrop limiting excess free cash availability.[F1][N2][S8]

Capital expenditure trended downward modestly after peaking around mid-300-million-dollar range reflecting selective investment primarily focused on dealership facility upgrades or new construction aligned with newly acquired properties ensuring infra supports operating scale without unnecessary expansion risk.[F1]

Collectively these moves suggest stewardship balancing shareholder returns against preservation of financial flexibility recognizing regulatory headwinds as well as integration demands accompanying aggressive dealership acquisition program.

Outlook and Market Signals: What to Watch in Upcoming Quarters

Post Q4 earnings commentary emphasizes that key performance indicators will hinge on efficacy integrating recent acquisitive expansions especially PMG Lexus/Toyota dealerships plus Central Florida Lexus additions expected to contribute materially starting mid-2026 cycles [N4][N9].

Critical variables include the trajectory of dealer count expansion aligned with franchise renewals or contraction risks offsetting attrition; responsiveness adapting retail models ahead of continuing UK FCA redress scheme implementation addressing allegedly unfair commissions within vehicle finance brokering that could impose administrative burdens or indirect cost offsets on dealers impacting profitability [S4][S5].

Further scrutiny warranted toward Penske Transportation Solutions’ adaptation to upcoming heavy-duty truck emission standards beginning model year ‘27 regulating fleet composition costs which poses dual challenge controlling expenses while meeting customer demand amid freight rate recessions.[S6][N1]

Inventory cycle management amidst constrained floor plan financing environments alongside semiconductor supply disruptions remain risk factors influencing new vehicle availability hence cascading through retail sales volumes warranting monitoring benchmarks on order fulfillment rates going forward.

This analysis synthesizes SEC filings and verified news sources without expressing investment recommendations or price targets. Financial metrics derive explicitly from reported data ensuring grounded assessment free from speculation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments