Pioneer Bancorp, Inc./MD Capitalizes on Local Market Strength and Diversified Services Amid Legal Headwinds

Pioneer Bancorp leverages deep regional roots and expanding financial offerings while navigating risks from ongoing litigation.

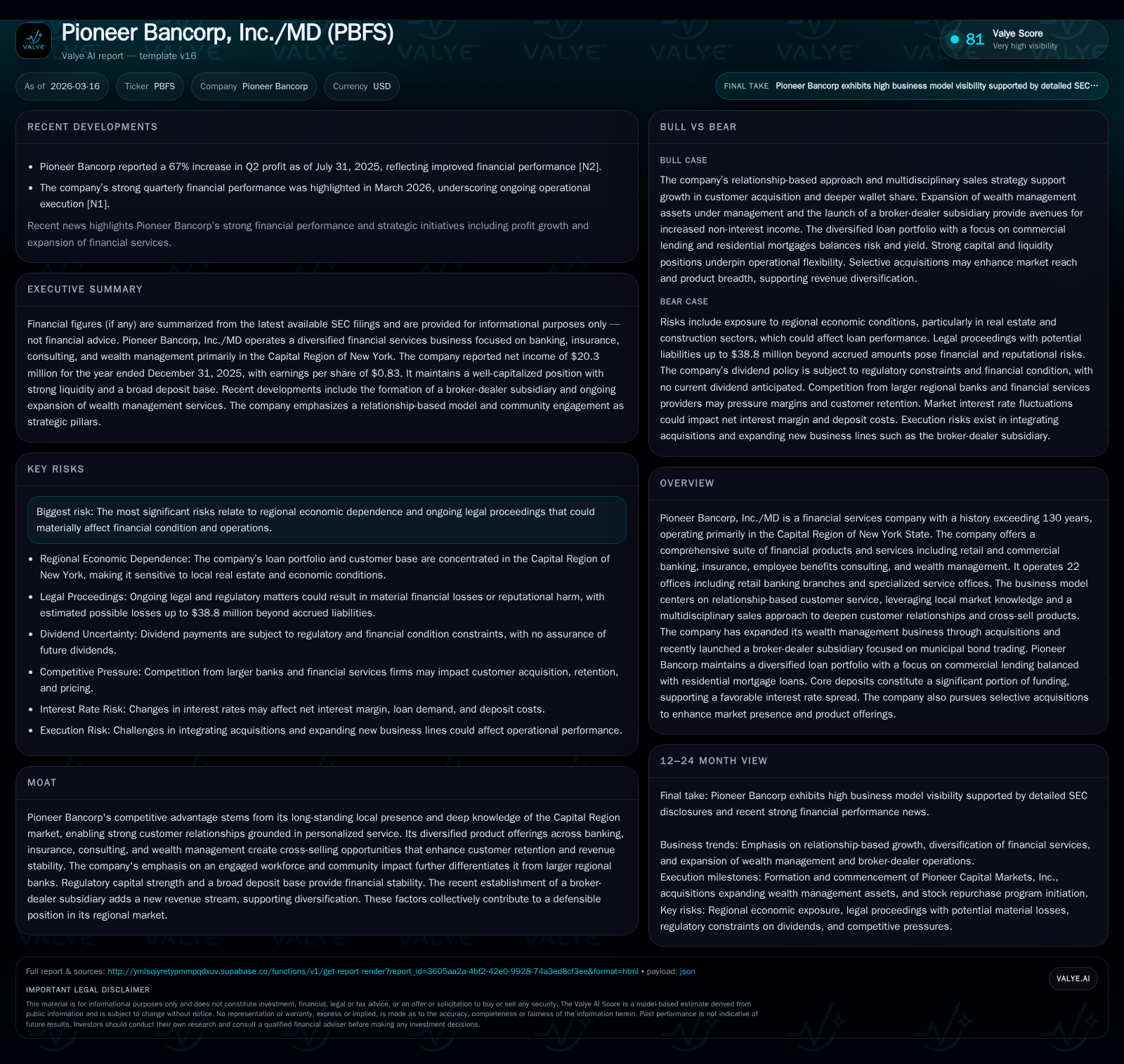

Pioneer Bancorp, a well-capitalized financial institution serving New York's Capital Region, has demonstrated robust growth driven by its relationship-based business model and expansion into wealth management and municipal bond trading. Despite significant gains in net income and deposit growth through 2025, the company faces material risks tied to legal proceedings and regional economic dependencies. Its capital allocation strategy includes prudent stock repurchases without dividends, underpinned by strong regulatory capital ratios. Monitoring how the legal exposures evolve will be key to assessing stability going forward.

Company Overview and Market Position

Pioneer Bancorp, Inc./MD is a century-plus established regional financial services company headquartered in Albany, New York. It operates primarily within the six-county Capital Region encompassing Albany, Greene, Rensselaer, Saratoga, Schenectady, and Warren counties [S1]. The company delivers a wide-ranging portfolio including retail and commercial banking, insurance products, employee benefits consulting, wealth management services through acquisitions in that space, and a recently formed broker-dealer subsidiary focusing on municipal bond trading—a niche aligned with local government finance demands [S21].

The firm's competitive advantage stems from its long-standing community presence combined with a relationship-driven customer engagement model. This approach supports cross-selling opportunities across its diversified services while fostering high employee engagement.

Historical Performance Drivers

The fiscal year ended December 31, 2025 marked a notable inflection point with strong net income growth but mixed cash flow trends:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 20 | 11 | +111.3% | |

| 2024 | 10 | 17 | 753000 | -56.3% |

| 2023 | 22 | 26 | 451000 | +113.5% |

| 2022 | 10 | 50 | 780000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | 6.3 | |

| 2024 | 3 | 16 | 3.2 |

| 2023 | 26 | 8.2 | |

| 2022 | 49 | 4.2 |

Source: SEC companyfacts cache [F1].

Net income more than doubled in FY2025 compared to the prior year due to effective revenue strategies including higher net interest income driven by improved asset yields and volume expansion [F1][S15]. However, operating cash flow decreased by about one-third reflecting working capital dynamics or timing effects [F1]. Capital expenditures increased notably but remain modest relative to total assets—indicative of targeted investments primarily for branch or IT infrastructure improvements [F1]. The company's equity base expanded steadily alongside earnings retention.

Revenue Composition and Loan Portfolio Development

Pioneer’s loan portfolio is diversified across residential mortgages—augmented through partnerships—as well as commercial real estate (CRE), commercial & industrial (C&I), home equity loans, and consumer lending segments [S20]. Key trends include:

- Growth in residential mortgage loans supported by collaboration with third-party mortgage companies.

- CRE and C&I loan increases fueled by funding exceeding payoffs.

- Moderate growth in home equity lines.

- Deposit balances increased nearly 10% to approximately $1.74 billion at December 31, 2025 [S12][S20], underpinning funding stability.

Deposit composition shifted towards higher-yield money market accounts and certificates of deposit amid competitive interest rate environments [S12][S15]. Loan portfolio quality remained solid with annualized net charge-offs near zero despite some increase in provision expense linked to portfolio growth [S16][S25].

Liquidity & Capital Structure

At fiscal year-end 2025, Pioneer maintained strong liquidity with $133.7 million in cash and cash equivalents plus a securities portfolio available for sale valued at $220.4 million [S4]. Access to liquidity includes Federal Home Loan Bank advances up to $622 million with only $50 million utilized at year-end [S11]. Regulatory capital ratios comfortably exceeded OCC "well capitalized" thresholds ensuring balance sheet resilience [S4].

On the liabilities side, certificates of deposit maturing within one year totaled approximately $263.8 million or about 15% of total deposits—a manageable concentration requiring ongoing monitoring for rollover risk or cost pressures [S4][S12]. Commitments to extend credit totaled around $350 million including commercial loan lines and standby letters of credit totaling approximately $27 million carrying typical credit risk managed under consistent underwriting policies [S7][S14].

Capital Allocation Strategy

Pioneer Bancorp has not paid dividends recently but retains flexibility subject to earnings results and regulatory constraints [S6]. Since May 2024 it has executed two stock repurchase programs authorizing roughly 2.55 million shares cumulatively—about 10% of outstanding shares at those times—with repurchases made at average prices below recent trading levels illustrating a shareholder value focus while maintaining financial flexibility [F1][S10].

Risks: Litigation Exposure & Regional Dependence

A significant risk factor involves ongoing legal proceedings related to alleged fraudulent activities involving associated parties (the "Mann Entities") dating back several years. Claims currently seek damages potentially exceeding $38.8 million beyond accrued reserves; these actions entail substantial legal expenses and uncertain outcomes that could materially affect financial results and reputation [S14][S27].

Additionally, geographic concentration exposes Pioneer Bancorp to economic fluctuations specific to the New York Capital Region real estate market cycles which could impact asset quality or loan demand during downturns.

Future Growth Considerations

Going forward Pioneer Bancorp is positioned to leverage:

- Deep regional penetration with longstanding local expertise,

- Cross-functional product mix enhancing wallet share capture,

- Expansion into municipal bond brokerage providing new fee income streams,

- Relationship-focused sales enablement expected to enhance customer retention and acquisition.

However, litigation uncertainties may divert resources or impact capital availability if settlements materialize significantly. Macroeconomic factors such as interest rate volatility or regional real estate softness could also constrain loan growth or compress margins.

Monitoring developments around legal cases outcomes alongside deposit behavior—especially certificate rollovers amid competitive rates—will be critical.

What To Watch Next

Investors should monitor:

- Updates or resolutions regarding pending litigation claims affecting provisions or contingencies,

- Quarterly indicators of loan growth pace relative to credit quality trends,

- Shifts in deposit composition influencing cost of funds,

- Contributions from municipal bond brokerage operations,

- Regulatory disclosures on capital adequacy amidst external pressures.

Summary Table: Key Financial Highlights

| Metric | FY2025 | FY2024 |

|---|---|---|

| Net Income (USD Million) | 20.3 | 9.6 |

| Operating Cash Flow (USD Million) | 11.1 | 16.9 |

| Equity (USD Million) | 324 | 305 |

| Total Deposits (USD Billion) | 1.74 | ~1.59 |

| Provision for Credit Losses (USD Million) | ~3.7 | ~2.7 |

| Non-performing Loans (%) | <0.30% | <0.40% |

| Stock Repurchases (USD Million) | ~11.3 | ~3.1 |

Note: All figures reflect reported fiscal year periods unless otherwise noted.

Conclusion

Pioneer Bancorp exemplifies a well-rooted regional bank blending traditional retail banking strengths with modern wealth management expansions underpinned by personal relationships within its markets. Its positive trajectory evidenced by doubling net income in FY2025 coincides with enhanced deposit gathering sustaining asset growth. Nonetheless persistent legal challenges introduce caution given contingent liabilities that could impact financial resilience depending on litigation outcomes. The company's focused capital deployment prioritizing buybacks over dividends combined with vigilant liquidity management positions it well within regulatory frameworks but underscores balancing growth ambitions against emerging risks. Ultimately Pioneer’s long-term success hinges on maintaining trust within its communities while navigating external disruptions impacting smaller banks concentrated regionally.

This analysis is based solely on publicly available information as of March 16, 2026, including SEC filings [S#], recent news sources [N#], and validated company facts data [F1]. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments