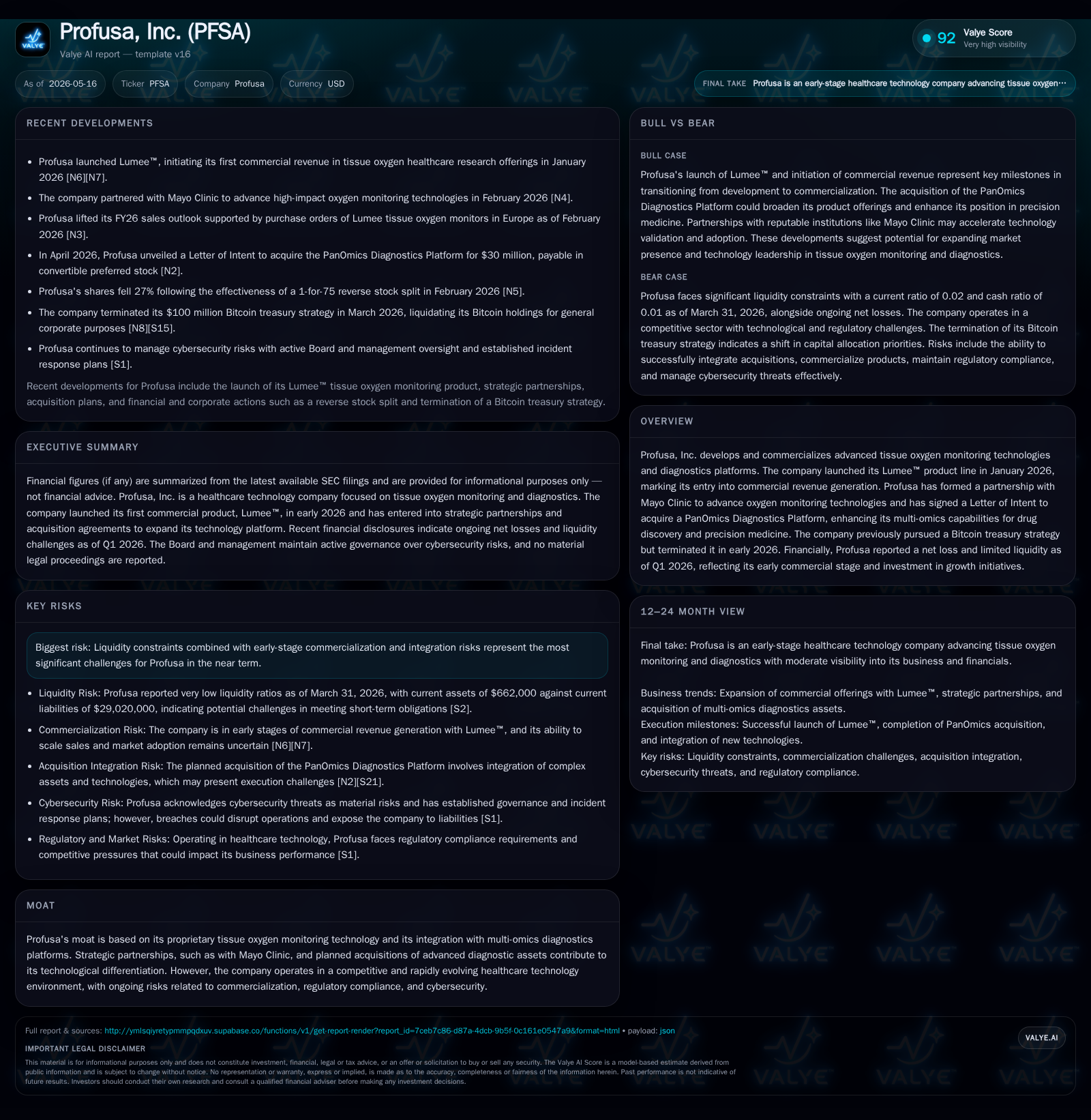

Profusa Accelerates Commercial Launch of Lumee™ Tissue Oxygen Monitor with Strategic Diagnostics Expansion

Profusa enters early commercialization with Lumee™ while navigating financial and Nasdaq compliance challenges amid multi-omics platform acquisition plans.

In Q1 2026, Profusa began generating its first commercial revenues with the launch of the Lumee™ tissue oxygen monitoring system, marking a pivotal shift from research to sales. This commercial phase is complemented by strategic moves such as partnering with Mayo Clinic and signing a Letter of Intent to acquire a PanOmics Diagnostics Platform, positioning Profusa to expand in precision medicine diagnostics. Despite technological differentiation driven by proprietary biosensor innovations and multi-omics integration, the company faces critical near-term risks including acute liquidity constraints and Nasdaq listing compliance pressures. Monitoring the progress of regulatory clearances, commercial traction, and financing efforts will be essential to assess Profusa’s path toward sustainable growth.

Recent Operational Milestones and SEC Filing Highlights

Profusa’s most recent quarterly report (Form 10-Q for period ending March 31, 2026) marks a watershed moment as the company initiates generation of commercial revenues tied directly to its Lumee™ tissue oxygen monitoring product line launched earlier in January 2026 [S2]. This transition from predominantly developmental R&D spending to actual sales represents a foundational pivot toward business model validation amidst early market entry challenges.

Additionally, a May 13, 2026 Form 8-K reported receipt of a Transfer Confirmation Letter from Nasdaq confirming that Profusa has complied with requirements to transfer its listing to The Nasdaq Capital Market by May 11 deadline, an essential step in maintaining its public exchange status amid prior non-compliance issues stemming from bid price rule adherence [S3]. The company concurrently terminated its previously pursued Bitcoin treasury strategy in early 2026 signaling refocus on core bio-monitoring technology commercialization [N1].

These developments underscore operational progress blended with ongoing corporate governance remediation efforts that set the context for Profusa's near-term trajectory.

Profusa’s Business Model: Tissue Oxygen Monitoring Technology and Product Portfolio

Profusa generates revenue primarily through sales of its Lumee™ biosensor devices designed for continuous tissue oxygen monitoring—a technologically differentiated offering leveraging proprietary hydrogel-based implantable sensors that provide real-time localized oxygen measurements into tissue microenvironments. This represents a departure from intermittent pulse oximetry or blood-based assessments common in clinical settings.

The business model includes direct sales to healthcare providers initially focusing on clinical diagnostic applications, alongside collaboration with pharmaceutical partners leveraging multi-omics data outputs surrounding oxygen levels for drug discovery or precision treatment adjustments. This revenue is driven by unit sales volumes of implants coupled with ancillary service fees related to data connectivity or analytics platforms integrated within Lumee™’s ecosystem.

Product quality centers on sensor accuracy, biocompatibility, longevity within the body, and seamless integration with digital health platforms—factors crucial for physician adoption and patient retention. Profusa’s technology uniquely fills a niche for continuous metabolic monitoring supporting chronic disease management such as peripheral artery disease or wound healing scenarios, differentiating it from wearables or spot-check diagnostics historically constrained by intermittent data points [S1].

Competitive and Industry Context: Diagnostic Technology Market Dynamics

Within the broader healthcare diagnostics landscape, Profusa operates at the intersection of implantable biosensing technologies and advanced diagnostics platforms incorporating omics data. Competitors encompass developers of wearable oxygen sensors or implantable monitors; however, few combine continuous tissue-level sensing with multi-omics molecular profiling in one integrated product line.

Regulatory environment remains stringent as FDA clearance pathways for implantable sensor devices necessitate robust clinical validation demonstrating safety and efficacy. Concurrently, reimbursement frameworks for novel diagnostic tools are evolving but often lag behind innovation deployment, presenting pricing pressure and adoption hurdles.

Pricing models are likely designed around device sales plus recurring software or data service subscriptions, though payer coverage remains an area requiring ongoing engagement. Industry fragmentation in biosensor offerings means Profusa must continuously prove superior clinical utility and cost-effectiveness to secure provider preference [S1].

Growth Drivers: Commercial Launch, Strategic Partnerships, and Platform Expansion

Key drivers underpinning Profusa’s growth include the ramp-up following Lumee™’s commercial launch which begins capitalizing on prior R&D investments and clinical trial validations. Early-stage commercial revenue generation evidences initial market acceptance though scale remains modest at this stage [F1].

Strategically meaningful is the established partnership with Mayo Clinic supporting advanced research agendas that validate oxygen monitoring’s clinical impact and broaden application scenarios potentially facilitating faster physician buy-in through trusted institutional endorsement [S1].

Further growth impetus comes from Profusa’s April 2026 Letter of Intent to acquire Bio Insights LLC’s PanOmics Diagnostics Platform for $30 million [N1], constituting a major expansion into multi-omics capabilities—enabling the company to augment its breath of diagnostics beyond oxygen sensing into integrated molecular analytics supporting drug discovery clients and precision medicine use cases.

Collectively these elements position Profusa toward cross-selling opportunities across pharma partnerships and healthcare provider segments creating potential revenue diversification beyond single-device sales.

Risks and Watchpoints: Liquidity Constraints, Regulatory Compliance, and Market Adoption

Despite technological potential, Profusa confronts sizeable near-term risks primarily anchored around financial health. As of March 31, 2026 balance sheet data indicates cash reserves stand at a scant $375K against current liabilities totaling approximately $29 million—yielding an extremely constrained current ratio near 0.02 reflective of urgent funding needs absent rapid revenue growth or external capital infusion [F1].[S2]

Nasdaq listing maintenance remains uncertain despite recent Transfer Confirmation Letter acknowledgment since ongoing compliance with bid price rules hinges on meeting prescribed milestones within tight timelines posing risk of delisting consequences impacting capital access [S3],[S7].

Operational risks include typical early-stage medtech challenges: scaling commercialization efforts effectively amid complex healthcare buying cycles; regulatory approval processes potentially delaying market expansion; cybersecurity threats due to sensitive biometric data handled; plus integration uncertainties upon consummation of diagnostic platform acquisition which introduces organizational complexity [S1].[S2]

Market adoption will be contingent on educating providers regarding bio-sensing benefits amid entrenched workflows plus convincing payers on cost-benefit metrics enabling reimbursement codes.

Near-Term Catalysts: Regulatory Updates, Commercial Rollout Progress, and Financing Events

Looking ahead milestones worth watchful attention include updates on FDA clearances relevant to Lumee™ expansions or new diagnostic indications which can materially influence market penetration pace.

Continued advancement on Nasdaq listing compliance through completion of transfer-related filings or reverse stock split actions can stabilize trading liquidity providing crucial capital markets access which are likely prerequisites for anticipated $10 million equity raise hinted in proxy disclosures [S23].

Progress reports on partnered pilot programs particularly via Mayo Clinic collaborations may serve as proof points enhancing credibility among healthcare practitioners accelerating adoption rates.

Similarly successful closing and integration of the PanOmics acquisition will represent a significant event potentially broadening product portfolio enabling higher-margin offerings targeting pharma-driven customers thereby diversifying revenue streams [N1,S1].

Latest Financial Snapshot and Liquidity Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $375000 | |

| 2026-03-31 | ||

| Current assets | $662000 | |

| 2026-03-31 | ||

| Current liabilities | $29mm | |

| 2026-03-31 | ||

| Current ratio | 0.02x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The latest available financial snapshot as per Q1 2026 filings presents:

| Metric | Value | Period Ending |

|---|---|---|

| Cash & Equivalents | $375K | |

| 2026-03-31 | ||

| Current Assets | $662K | |

| 2026-03-31 | ||

| Current Liabilities | $29.02M | |

| 2026-03-31 | ||

| Net Debt (est.) | $338K | Approx. recent |

| Revenue | $100K | End of FY 2024* |

*Latest recognized revenue figure is dated; first commercial revenues recognized Q1 2026 but exact Q1 revenue not separately disclosed yet.[F1]

This snapshot highlights acute working capital pressure exacerbated by operating losses consistent with early-stage medtech firms investing heavily in commercialization infrastructure without immediate scale benefits.[F1] Costs related to R&D continuation alongside general administrative expenses contribute to negative operating margins stressing the need for prompt cash replenishment through financings or accelerated sales growth.[S2]

The low direct debt level reduces immediate borrowing risk but offers limited liquidity buffer given cash scarcity.[F1] Overall financial profile reinforces capital adequacy as a critical watchpoint alongside operational execution during this nascent commercialization phase.

Disclaimer: This analysis is based solely on information publicly available as of May 16, 2026 including SEC filings and verified news sources. It does not contain investment advice or recommendations. Investors should conduct their own due diligence considering risks involved with early-stage medical technology companies such as Profusa.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments