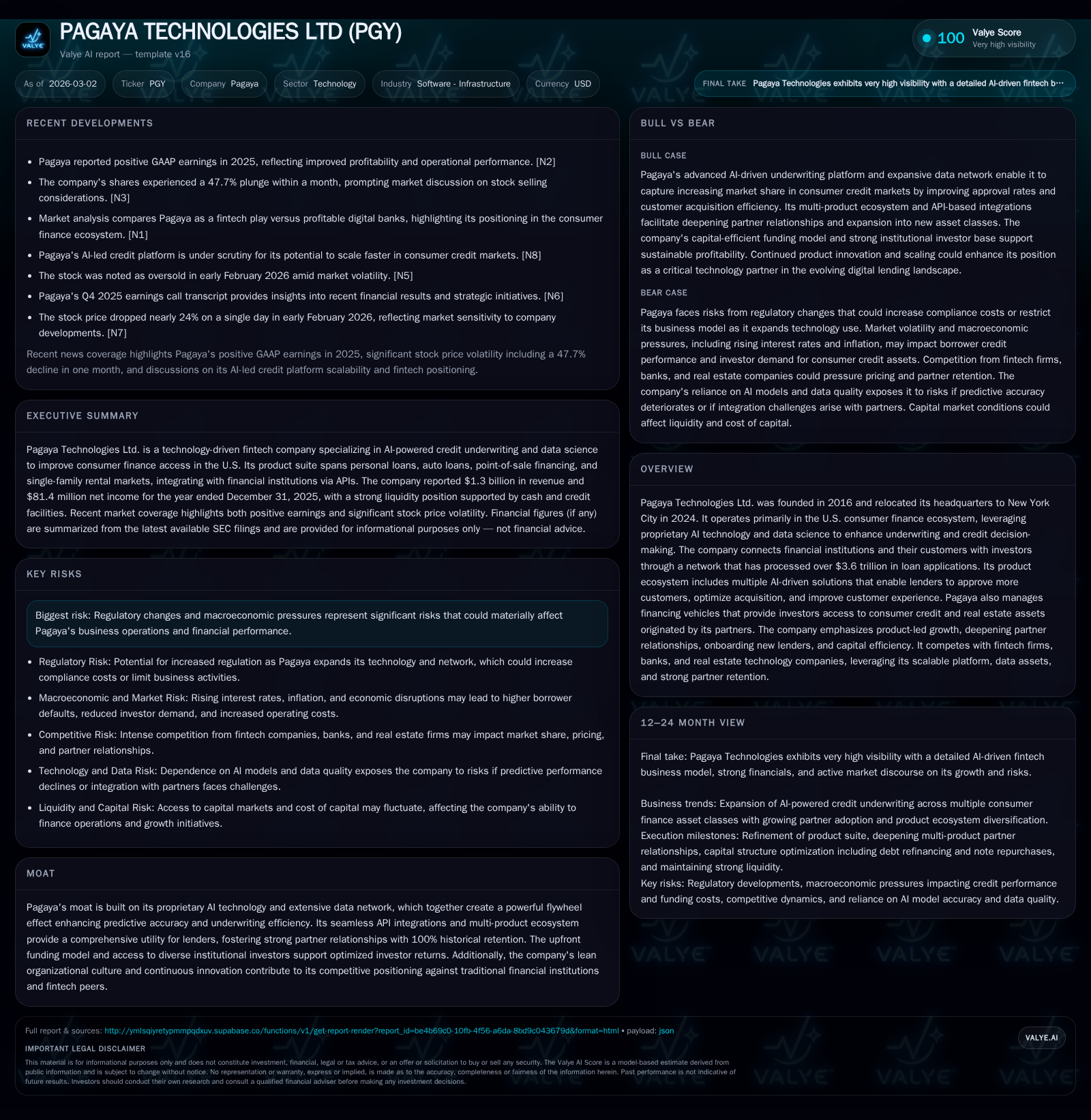

Pagaya Technologies’ AI-Driven Expansion Boosts Revenue and Profitability with Capital Efficiency Tradeoffs

AI-powered underwriting platform leverages network effects in consumer finance while managing rising capital commitments and regulatory risks.

Pagaya Technologies Ltd. has transitioned from significant losses to solid profitability by scaling its AI-driven lending technology within the U.S. consumer finance ecosystem. Its expansive partner network and product suite drive robust revenue growth and operating leverage, while its strong capital structure and diversified funding underpin continued expansion. However, growth is balanced against increased capital deployment requirements and external uncertainties such as evolving regulations and credit market dynamics.

Company Overview

Founded in 2016 and relocating its headquarters to New York City in 2024, Pagaya Technologies Ltd. occupies a unique niche at the intersection of AI technology and consumer finance [S15]. The company operates a proprietary AI platform designed to revolutionize underwriting by enabling lenders—ranging from fintech startups to large banks—to approve a greater volume of creditworthy borrowers with improved risk assessment accuracy. This technological edge is supported by Pagaya’s expansive network that has collectively processed substantial loan volumes [S17].

Pagaya’s business model combines software infrastructure through AI-driven products with capital-intensive financing via managed securitizations and investment vehicles. This dual approach allows it to generate fee income by facilitating asset origination for lender Partners while optimizing investor access to diversified consumer credit portfolios through its Financing Vehicles [S17][S23].

Historical Performance

Pagaya has demonstrated consistent revenue growth alongside expanding operations across multiple lending verticals including personal loans, auto loans, point-of-sale financing, and single-family rentals (SFR) [S15]. The company shifted from prior years of losses due primarily to upfront investments in technology and network-building to reporting solid financial milestones during FY2025:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1301 | 81 | 239 | 264 | +26.1% | +120.3% |

| 2024 | 1032 | -401 | 67 | 67 | +27.1% | -212.5% |

| 2023 | 812 | -128 | 10 | -24 | +8.4% | +57.5% |

| 2022 | 749 | -302 | -40 | -252 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 225 | 17.0 |

| 2024 | 49 | -122.9 |

| 2023 | -11 | -22.9 |

| 2022 | -62 | -54.6 |

Source: SEC companyfacts cache [F1].

Revenue growth accelerated on strong adoption of AI-enabled underwriting solutions across an expanding partner base exceeding thirty lenders [S12][S17]. Operating leverage became evident as operating income turned positive and surged nearly threefold year-over-year in FY2025.

Net income swung from significant losses in previous years to profitability in FY2025 — signaling improved cost management and pricing power within its network fee streams [F1][S21]. Operating cash flow's substantial increase reflects genuine cash-generative capacity alongside controlled investment spending.

Capital Structure & Cash Flows

As of December 31, 2025 Pagaya held approximately $235 million in cash and equivalents [F1], maintaining liquidity to support ongoing operations. In mid-2025 the company issued $500 million aggregate principal amount of senior unsecured notes due in 2030 at an interest rate of 8.875%, using proceeds primarily to retire prior term loans totaling $332 million [S4][S6][S14]. This refinancing extended debt maturities while materially lowering borrowing costs compared to prior revolving credit facility rates up to SOFR plus 7.5%, now reduced to margins between approximately 2.5%–3.5% on new facilities [S9].

Additional highlights include:

- Establishment of a new revolving credit facility providing committed borrowing capacity of $132 million under improved terms.

- Opportunistic repurchases of outstanding notes at discounts during favorable market conditions as part of liability management [S7][N1].

Free cash flow—defined as operating cash flow less capital expenditures—approximated $225 million for FY2025 underscoring substantial organic funding capacity without reliance on external equity or incremental leverage [F1][S24]. Capital expenditures decreased modestly reflecting platform maturation but remain focused on advancing core AI capabilities [F1][S25].

Business Model & Products

Pagaya’s AI technology leverages extensive datasets encompassing economic trends and consumer behavior patterns often unavailable or underutilized by traditional lenders. This digital advantage enables seamless real-time decisioning through API-driven integration into lenders’ workflows—reducing latency while broadening approval windows without materially increasing risk exposure [S12][S17].

Key product offerings include:

- Direct Marketing Engine: Enhances customer acquisition by identifying profitable prospects.

- Affiliate Optimizer: Streamlines referral channel efficiency.

- FastPass: Accelerates approval processes while maintaining rigorous credit standards.

This modular plug-and-play approach facilitates deeper adoption within partner institutions transitioning from single-solution use toward multi-product engagement — cementing longer-term contractual relationships that mitigate cyclical credit appetite fluctuations [S17][S19].

The company’s financing arm operates asset-backed securitizations alongside forward flow agreements with institutional investors who gain diversified exposure sourced through Pagaya’s underwriting expertise [S21]. Network Volume—the gross value of assets originated via Pagaya’s technology—serves as both an operational metric and revenue driver encompassing origination fees plus contract- and capital markets-derived fees [S20].

Growth Outlook & Strategy

Future growth drivers include:

- Scaling penetration within existing partners by cross-selling additional solutions addressing multiple lending lifecycle stages.

- Onboarding new enterprise lenders seeking scalable AI underwriting validated by pre-built APIs.

- Expanding asset classes beyond consumer credit into real estate financial products leveraging SFR platform capabilities.

- Maintaining lean organizational structures emphasizing innovation investments to sustain product relevance amid competitive fintech dynamics.

These efforts are balanced against macroeconomic cycles affecting loan performance as well as evolving regulatory scrutiny around AI applications in credit underwriting—a rapidly changing environment requiring robust compliance frameworks overseen at senior management levels [S11][S1].

Returns & Capital Allocation

Pagaya posted an approximate return on equity near 17%, calculated from FY2025 net income of $81 million against equity of about $480 million — indicating effective capital deployment toward profit generation [F1].

Capital allocation priorities encompass:

- Deleveraging via repayment of higher-cost debt.

- Opportunistic note repurchases yielding accounting gains.

- Moderate reinvestment focused on R&D supporting product-led growth.

- No explicit dividend policy disclosed.

Strong cash flows provide flexibility for sustained investment or potential shareholder returns aligned with strategic priorities [F1][S18].

Competitive Positioning & Moat

Pagaya’s competitive advantage derives from proprietary algorithms trained on diverse longitudinal financial data combined with an extensive lender-investor network creating barriers for competitors reliant on legacy systems or smaller datasets [S12][S17]. Improved predictive accuracy enhances partner satisfaction contributing to near-perfect historical retention since inception.

End-to-end integration via APIs reduces switching costs and supports multi-product cross-selling initiatives expanding ecosystem footprint—key differentiators versus incumbents hesitant on modernization or smaller fintechs lacking scale [S12].

Risks & Challenges

Regulatory developments may impose constraints on AI-based lending models necessitating costly adaptations or market limitations [S11]. Macroeconomic headwinds such as rising interest rates or economic uncertainty could impact loan defaults affecting fee revenues or requiring higher risk reserves within Financing Vehicles [S21]. Competition remains intense from fintech innovators and traditional banks pursuing digital transformation.

Liquidity risks persist if capital markets tighten unexpectedly despite recent facility improvements—requiring agile funding strategies including possible equity issuance which would dilute existing shareholders [S16]. Cybersecurity threats are managed through dedicated executive oversight but remain inherent risks given sensitive data handling responsibilities [S1].

Conclusion & Watch Points (Analysis)

Key areas for ongoing monitoring include:

- Growth trajectory for Network Volume especially across new asset classes,

- Margins on fee revenue relative to production costs,

- Partner onboarding pace particularly among larger financial institutions,

- Macro impacts on loan performance embedded within forward flow agreements,

- Debt refinancing opportunities or note repurchase activities,

- Regulatory developments affecting AI usage norms,

- Investments relative to productivity gains within technology teams. These factors will shape whether Pagaya successfully converts technological advantages into sustainable financial outcomes amid evolving market conditions.

This analysis strictly reflects publicly filed data points complemented by relevant sector context based solely on verified regulatory disclosures as of March 2nd, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments