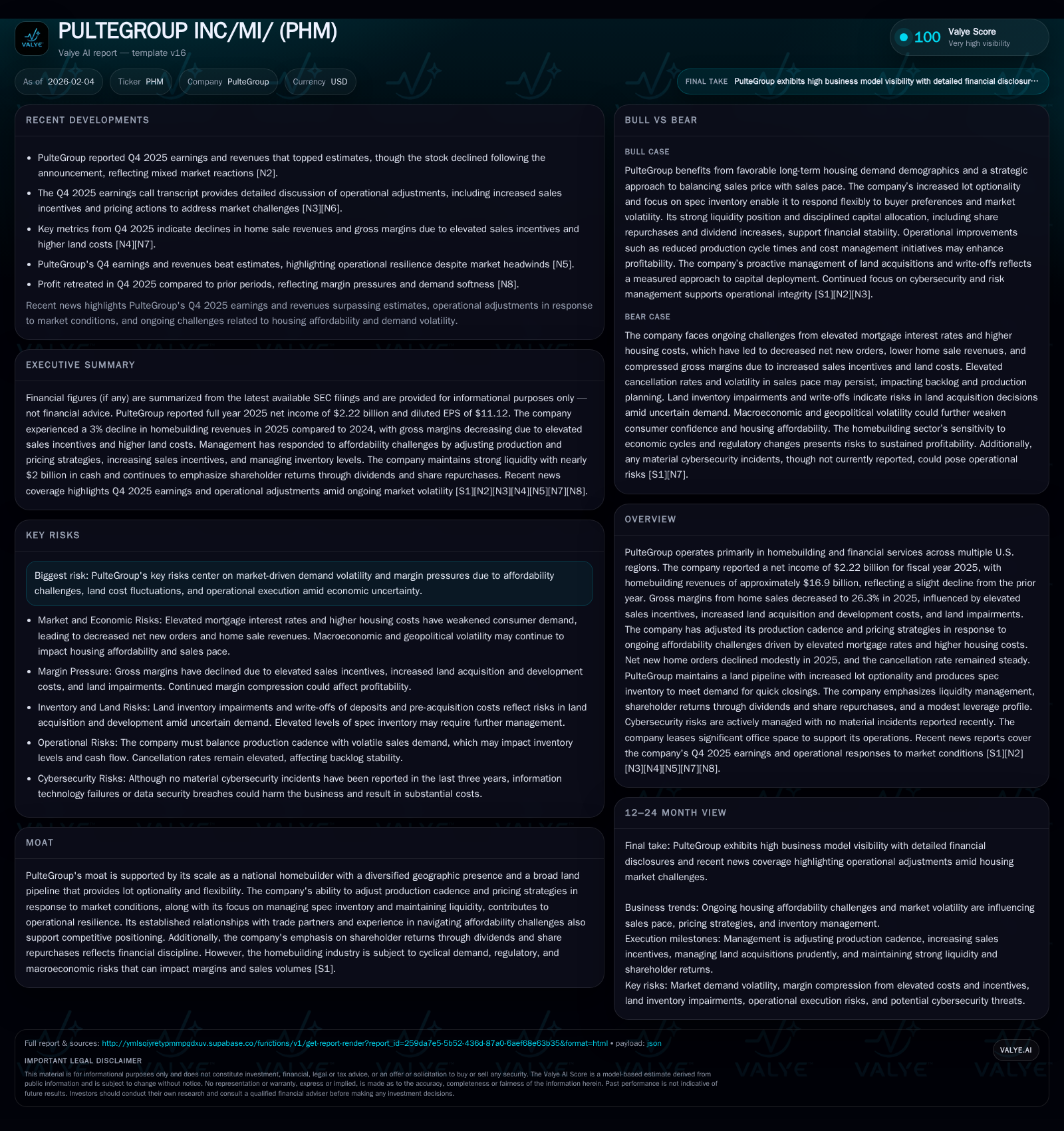

PulteGroup’s Strategic Resilience in a Challenging 2025 Housing Market

Amid persistent affordability headwinds, PulteGroup leverages land pipeline flexibility and disciplined capital management to navigate demand volatility.

In fiscal year 2025, PulteGroup faced a complex housing market typified by elevated mortgage rates and rising land costs that dampened demand and compressed gross margins. The company responded by adjusting production cadence, implementing pricing strategies focused on incentives, and enhancing lot optionality within its land pipeline to maintain operational agility. Capital discipline remained a priority with continued share repurchases and dividend increases underscoring shareholder return commitment despite margin pressures. Looking forward, demographic tailwinds support a cautiously optimistic outlook amid ongoing near-term volatility.

2025 in Review: Financial Highlights & Market Reactions

PulteGroup entered and navigated 2025 amid a U.S. housing market displaying pronounced challenges — elevated mortgage rates stifling buyer enthusiasm and cost inflation squeezing margins. The company’s full-year results disclosed a net income of $2.22 billion against homebuilding revenues of approximately $16.9 billion, registering a slight decline versus prior years [F1]. This subtle contraction masks more significant underlying pressure points that dictated the operational narrative throughout the year.

Gross margins softened to 26.3%, down from higher levels seen previously, attributable mainly to intensified sales incentives employed to attract cost-conscious buyers, rising expenses tied to land acquisition and development, and impairments recorded against certain land parcels [S2]. These factors collectively weighed on profitability despite management’s tactical responses.

Interestingly, despite PulteGroup’s Q4 earnings beating estimates in January 2026 [N2], shares experienced downward pressure post-announcement — illustrating nuanced investor concern about sustainability of margins amid ongoing macroeconomic headwinds [N13]. Earnings call insights further revealed management’s candid assessment of persistent affordability issues impacting order flows and cancellations remaining stable but not abating [N3].

Affordability Challenges and Demand Dynamics: The Crux of 2025 Performance

Affordability emerged as the dominant theme shaping buyer behavior throughout 2025. Elevated mortgage interest rates prolonged their grip on market psychology, constraining purchasing power at precisely the moment when housing costs — including labor and materials — were escalating [S2]. Consumer confidence ebbed under these pressures, translating into net new home orders declining approximately 6% to 7% versus comparable periods from the previous year [S2].

Cancellation rates did not spike significantly but held steady — an indication that while fewer buyers committed upfront, attrition among those who booked homes was controlled [N3]. This stability helped temper revenue disruption but also signaled persistent volatility in monthly sales pacing.

Management commentary underscored a cautious stance toward the evolving landscape: expecting sustained affordability challenges to keep demand oscillating in the near term, necessitating dynamic adjustments in both pricing and production cadence [S2]. Analysts had forecasted this softening trend prior to Q4 results release [N11], suggesting that market expectations broadly aligned with realized outcomes.

Strategic Land Pipeline Management: Lot Optionality and Inventory Agility

A cornerstone of PulteGroup’s strategic response lies in its sophisticated land pipeline management. The company increased lot optionality by selectively expanding land holdings through flexible option agreements while simultaneously opting out of less favorable contracts when revised underwriting did not justify acquisition [S2]. These decisions resulted in write-offs totaling $26.5 million for deposits related to walked-away options but reflected prudent capital allocation in an uncertain environment.

Moreover, recognizing shifting consumer preferences toward quicker closings amid uncertain buying conditions, PulteGroup boosted production of spec inventory — homes built without prior customer orders — enabling it to meet demands from buyers seeking shorter delivery windows [S2]. This operational agility supports a competitive edge by reducing frictional delays common in traditional homebuilding timelines.

This approach reinforces the company’s moat: its scale across multiple geographies paired with a large but selectively curated land portfolio grants flexibility unparalleled by smaller regional competitors [S1]. Consequently, PulteGroup can modulate inventory levels responsively without overcommitting capital ahead of confirmed demand.

Pricing and Incentives: Balancing Margins Amid Elevating Costs

Margins faced considerable headwinds stemming from rising land acquisition costs exacerbated by supply constraints and broader inflationary forces affecting labor and materials pricing [S2]. In turn, PulteGroup intensified use of sales incentives designed specifically to counteract price sensitivity among potential buyers — prominently including mortgage interest rate buydowns aimed at mitigating borrowing cost burdens [N3].

While such incentives enhanced order activity relative to what might have otherwise been steeper declines, they exerted downward pressure on gross margin percentages. Declines from around 28-29% seen in prior periods slipped closer to 26% during much of 2025 [S2], illustrating the delicate balance between maintaining sales volume versus profitability.

Additionally, as some communities experienced slower absorption rates due to affordability pressures, price reductions further trimmed achievable revenue per unit. Management’s transparent acknowledgment of this dynamic during earnings calls substantiated investor awareness that margin recovery would likely require stabilization of external cost drivers or significant market shifts [N3].

Liquidity and Capital Allocation: Dividends, Buybacks, and Cash Management

Despite margin compression signaling profit challenges ahead, PulteGroup sustained financial discipline that underpins confidence among shareholders and counterbalances top-line softness. The company closed 2025 holding roughly $2 billion in cash and equivalents — an ample liquidity buffer maintained even as capital expenditures and operating needs persisted [F1].

Capital allocation decisions evidenced this prudence too: share repurchase authorization expansions totaling $1.5 billion authorized in January 2025 permitted aggressive buybacks executed against depressed stock price levels throughout the year [S2]. Concurrently, quarterly dividends rose incrementally (from $0.20 to $0.22 per share early in 2025) reinforcing an ongoing commitment to shareholder returns despite earnings variability [S1].

This measured approach reflects recognition of uneven market headwinds blended with long-term confidence — balancing immediate operational exigencies without undermining investor value frameworks.

Risk Landscape: Industry Cyclicality Meets Execution Complexity

PulteGroup operates within the inherently cyclical homebuilding sector where macroeconomic conditions ripple quickly through demand metrics and margin profiles alike [S1]. Key vulnerabilities include:

- Volatile consumer demand responding abruptly to interest rate fluctuations;

- Inflationary pressures on land prices coupled with possible impairment risks;

- Legal contingencies related to residential construction defect claims posing financial uncertainty;

- Complex operational execution required amidst shifting volumes and cost structures.

Recent news coverage underscores these realities with profit retreats noted amidst external adversities even as overall revenues held firm [N13]. While reserves are provisioned adequately according to current assessments by legal experts, overstated liabilities could impact future earnings materially if risk events intensify beyond estimates [S1].

Navigating these layered risks demands nimble management paired with robust governance frameworks ensuring oversight extends beyond day-to-day operations into strategic risk monitoring.

Governance Focus: Cybersecurity Oversight in a Homebuilder’s Context

Amid mounting digital integration within homebuilding processes and financial services offered through subsidiary channels (Pulte Mortgage), information technology security has emerged as an essential governance pillar for PulteGroup [S1]. Cybersecurity risk is actively overseen by the Board’s Audit Committee supported by dedicated executive roles:

- A Chief Information Officer (CIO) overseeing enterprise-wide IT functions;

- A Chief Information Security Officer (CISO) managing cyber defense strategies;

- Quarterly updates provided internally gauging risk posture.

Formalized Cybersecurity Incident Response Plans ensure structured handling should threats materialize; notably no material cybersecurity events occurring over past three years highlights effective prevention controls implemented by seasoned IT leadership teams possessing decades-long sector experience [S1]. This governance rigor serves as both a resilience catalyst against operational disruptions and reassuring signal for investors increasingly attentive to digital vulnerabilities impacting corporate value.

The Long View: Demographic Tailwinds Versus Near-Term Volatility

While near-term turbulence persists driven primarily by macroeconomic affordability constraints impacting homebuyer willingness or ability to purchase at prevailing prices or interest rates, underlying U.S. housing demographics remain supportive over longer horizons. Factors include population growth trends favoring first-time homebuyers entering prime purchasing age cohorts alongside chronic underbuilding relative to historical norms documented industry-wide [S2].

Management acknowledges this duality candidly: optimistic about eventual normalization but committed presently to cautious pacing that preserves liquidity without excessive risk-taking amidst volatile monthly sales patterns — a prudent posture given today’s economic crosscurrents [S2]. Investor discourse around PHM stock activity illustrates continuing market engagement fueled partly by anticipation that eventual easing of rate pressures may catalyze stronger absorption moving forward despite interim softness documented through late 2025 earnings season commentary [N12].

This analysis synthesizes publicly available data from company filings alongside recent news releases without making investment recommendations or forecasts. Situations described reflect conditions as reported through early 2026 disclosures; readers should conduct additional due diligence when forming independent conclusions related to PulteGroup or the broader homebuilding market dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments