Antero Resources: Strategic Asset Base and Regulatory Dynamics Shaping Financial Resilience

A detailed analysis of Antero's recent earnings, regulatory challenges, competitive advantages, and financial health against the backdrop of evolving market sentiment.

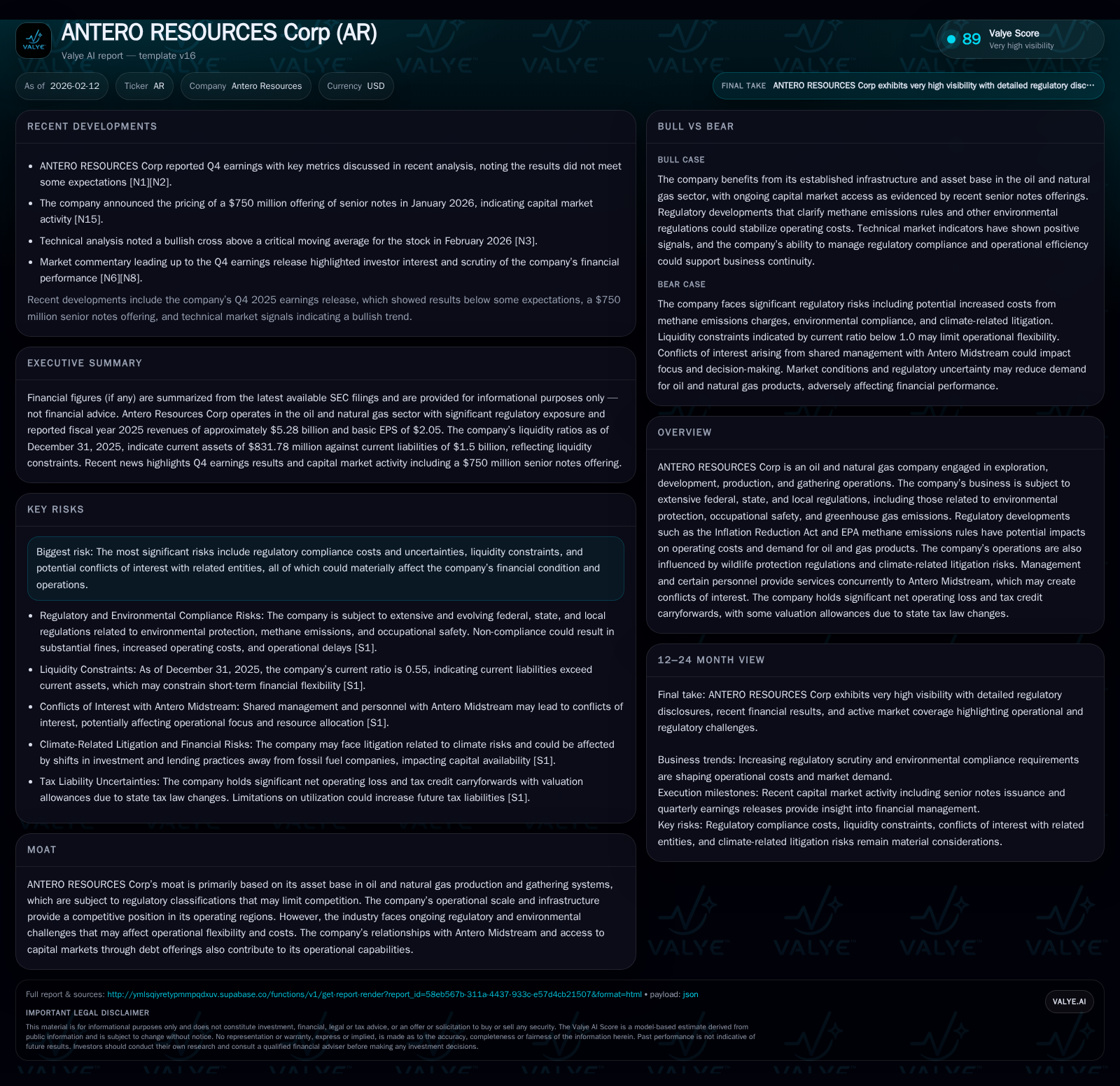

Antero Resources reported a notable Q4 earnings miss amid heightened regulatory scrutiny and operational cost pressures tied to EPA methane rules and the Inflation Reduction Act. Despite these headwinds, the company’s extensive asset base in oil and natural gas production and gathering infrastructure anchors its competitive moat, although potential FERC regulatory changes loom. Antero’s liquidity picture remains strained as evidenced by its low current ratio and ongoing share repurchases constrained by credit facility covenants. The dual relationship and overlapping management with Antero Midstream introduces governance complexities that investors must weigh alongside environmental litigation risks and broad energy sector dynamics driving mixed market sentiment.

Unpacking Antero's Q4 Earnings: Expectations vs. Reality

Antero Resources' Q4 2025 financial results released February 11 presented a clear divergence from market expectations. Analysts had anticipated a moderate decline in earnings but were caught off guard by the magnitude of the miss [N2]. Revenue pressures were driven in part by softer commodity prices observed through late 2025 as well as higher variable costs tied to increased regulatory compliance [N1][N6]. Operational expenses rose notably due to adaptations for methane emissions rules mandated by the EPA, alongside inflationary impacts on field services and materials. While this earnings shortfall disappointed near-term investors, it underscores the volatility inherent in Antero's operating environment shaped by external policy factors.

Navigating Regulatory Crosswinds: How Policy Shapes Operations

Regulatory complexity plays an outsized role in Antero’s business calculus. The company's natural gas gathering assets benefit historically from a non-FERC jurisdictional status under Section 1(b) of the Natural Gas Act (NGA), exempting them from federal regulation — an important operational advantage that keeps costs lower [S1]. However, growing administrative scrutiny and ongoing litigation blur these boundaries with potential reclassification looming. Such reclassifications would subject gathering infrastructure to FERC oversight, introducing reporting requirements, penalties, and increased costs [S1].

The Inflation Reduction Act (IRA) compounds this pressure. Signed into law in August 2022, IRA implemented for the first time a federal methane emission fee on oil and gas operators [S1]. Although subsequent executive orders paused some IRA funding disbursements, underlying compliance burdens remain intact with uncertain timing and scope [S1]. Additionally, state-level regulations related to greenhouse gas emissions further amplify cost variability.

Collectively, these evolving regulatory landscapes create a challenging backdrop where Antero must balance compliance expenditure without detrimentally impacting profitability or operational agility.

Competitive Moat: Beyond Reserves – Infrastructure and Market Positioning

Antero’s moat extends beyond mere resource volumes—it rests heavily on its integrated gathering infrastructure synergy with production assets [valye_report_excerpt.moat]. The company’s scale in key basins affords it advantages in logistics efficiency, reducing per-unit transportation expense relative to competitors reliant on third-party midstream providers.

This vertically aligned operation limits exposure to market fluctuations affecting pipeline tariffs but is not immune to shifting regulatory regimes. Should FERC impose classification changes on these gathering systems, anticipated increases in operating expenditures could erode this advantage over time [S1]. However, as things stand, regulatory classification shields provide a quasi-barrier to entry for new competitors lacking such infrastructure.

Moreover, Antero’s access to capital markets through debt offerings complements infrastructure investments that sustain its positioning—though this linkage also enforces dividend restrictions (discussed later). The interplay between infrastructure control and financing channels cements a sustainable competitive edge amidst sector headwinds.

Analyzing Financial Health: Liquidity, Debt, and Capital Allocation

From a balance sheet perspective, Antero exhibits tension points worthy of close attention. Its current ratio at year-end 2025 measured approximately 0.55 (current assets $832 million vs. current liabilities $1.5 billion) highlighting near-term liquidity pressure [F1]. This low ratio limits flexibility in meeting short-term obligations without recourse to capital markets or asset sales.

Simultaneously, management has executed sizeable share repurchases—roughly $1.1 billion spent retiring nearly 32 million shares since program inception—reflecting confidence in undervaluation but also consuming significant cash flow [S1]. Such capital deployment underscores strategic prioritization of shareholder value enhancement via buybacks rather than dividends; however, it must be balanced against pressing liquidity constraints.

Debt facilities further complicate capital choices. Covenants within Senior Notes and credit agreements restrict dividend distributions while allowing discretionary stock repurchases subject to availability of excess cash flow after debt servicing [S1]. This structural constraint has resulted in no dividends declared or paid to date.

The company also holds material net operating loss (NOL) carryforwards that partially shield taxable income but valuation allowances applied due to state tax law changes reduce this benefit visibility [valye_report_excerpt.overview]. Overall, Antero’s financial architecture reflects a delicate navigation between aggressive capital return policies and constrained liquidity buffers.

Conflict and Collaboration: The Dual Mandate with Antero Midstream

A nuanced element influencing corporate governance is the dual role played by certain officers serving both Antero Resources Corp and affiliated entity Antero Midstream. This shared management structure fosters operational integration—providing synergies across upstream production and midstream gathering assets—but generates conflict of interest risks flagged explicitly in the company’s filings [valye_report_excerpt.overview][valye_report_excerpt.risks].

Such conflicts could influence decision-making priorities concerning allocation of resources or strategic initiatives potentially favoring one entity over the other. Conversely, aligned leadership supports coordinated infrastructure development efforts essential for throughput optimization.

Investors monitoring governance dynamics should consider this dual mandate as both a source of operational strength reliant on collaboration but also an area requiring vigilant oversight for conflicts potentially adverse to minority shareholder interests.

Shareholder Value Actions: Repurchases and Dividend Policy in Focus

Antero’s board authorized its initial $1 billion share repurchase plan in February 2022 followed by an additional $1 billion increase later that year—totaling up to $2 billion capacity—with execution ongoing into late 2025 [S1]. Approximately $1.1 billion has been spent repurchasing shares at average prices around $32 per share over recent quarters demonstrating active engagement with capital return policies even amidst earnings volatility.

Contrastingly, no dividends have been declared or paid given contractual restrictions imposed by credit agreements and senior notes indentures limiting distributions absent sufficient excess cash flow tests being met [S1]. The board retains discretion over future dividend declarations contingent on financial performance and strategic priorities.

This approach indicates management favors flexible deployment of free cash flow currently skewed toward buybacks rather than fixed income streams for shareholders—a stance likely influenced by balancing debt covenants with intent to maintain leverage targets.

Technical Spotlight: Interpreting Recent Bullish Signals

Intriguingly juxtaposing fundamental challenges are recent technical market signals pointing toward renewed investor optimism around AR's equity prospects. Reports document a bullish moving average crossover occurring just days following the Q4 earnings report release near February 11—a timing suggesting buyers may be positioning ahead of anticipated operational improvements or sector momentum [N9].

Additionally, supportive macro drivers including record natural gas draws hint at tightening supply fundamentals which can underpin price appreciation longer term [N10]. While these technical cues do not negate structural risks faced by Antero, they highlight speculative appetite possibly fueled by perceived valuation mispricing or anticipation of regulatory clarity easing.

Thus far we see IT-driven momentum coexisting uneasily alongside fundamental volatility—a pattern observed elsewhere within select energy peer sets.

Risks on the Horizon: Environmental Litigation and Compliance Costs

Antero’s disclosures articulate explicit risk factors tied closely to environmental regulations—particularly methane emissions fees federally introduced under the IRA—and related compliance expenditures expected to rise materially [valye_report_excerpt.risks][S1].

Legal proceedings arising from climate-change litigation pose additional financial contingencies that could impair operating results if adverse judgments occur or remediation mandates escalate costs disproportionately.

Furthermore, potential reclassification of midstream assets under FERC jurisdiction adds penalty exposure risk (daily fines potentially exceeding $1.5 million per violation) plus incremental approvals burdening capital projects [S1]. These multi-pronged environmental litigations and enforcement risks necessitate prudent reserve allocations impacting reported net income stability.

Such layered legal-regulatory frameworks contribute significantly to downside case scenarios meriting sustained investor scrutiny given their capacity to disrupt cash flows suddenly or shift business economics unfavorably.

Market Sentiment in Context: Comparing Energy Peers and External Commentary

Against broader sectoral currents, AR's performance sits amid mixed narratives. Peers like Magnolia Oil & Gas (MGY) delivered Q4 beats bolstering positive comparisons while SM Energy also reported gains sparking cautious optimism among small-cap energy investors [N5][N12]. Yet prominent voices such as David Einhorn issue warnings about elevated valuation risks broadly across equities including energy stocks considering macroeconomic uncertainties [N13].

US manufacturing data supporting economic growth adds further complexity by encouraging risk-on behaviors contrasted against global energy transition debates fueling skepticism [N14]. Antero thus occupies a contested space where technical buying interest overlaps with fundamental caution reflective of policy uncertainty alongside corporate-specific factors examined herein.

This dual sentiment matrix frames near-term trading behavior more than long-term fundamental repositioning at present.

This analysis is based solely on publicly available data as of February 12, 2026. It does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments