Aurora Innovation’s Bold Transition: From Autonomous Trucking Pioneer to Passenger Mobility Challenger

Aurora Innovation embarks on commercializing its Aurora Driver platform, balancing breakthrough technology with formidable operational and financial challenges.

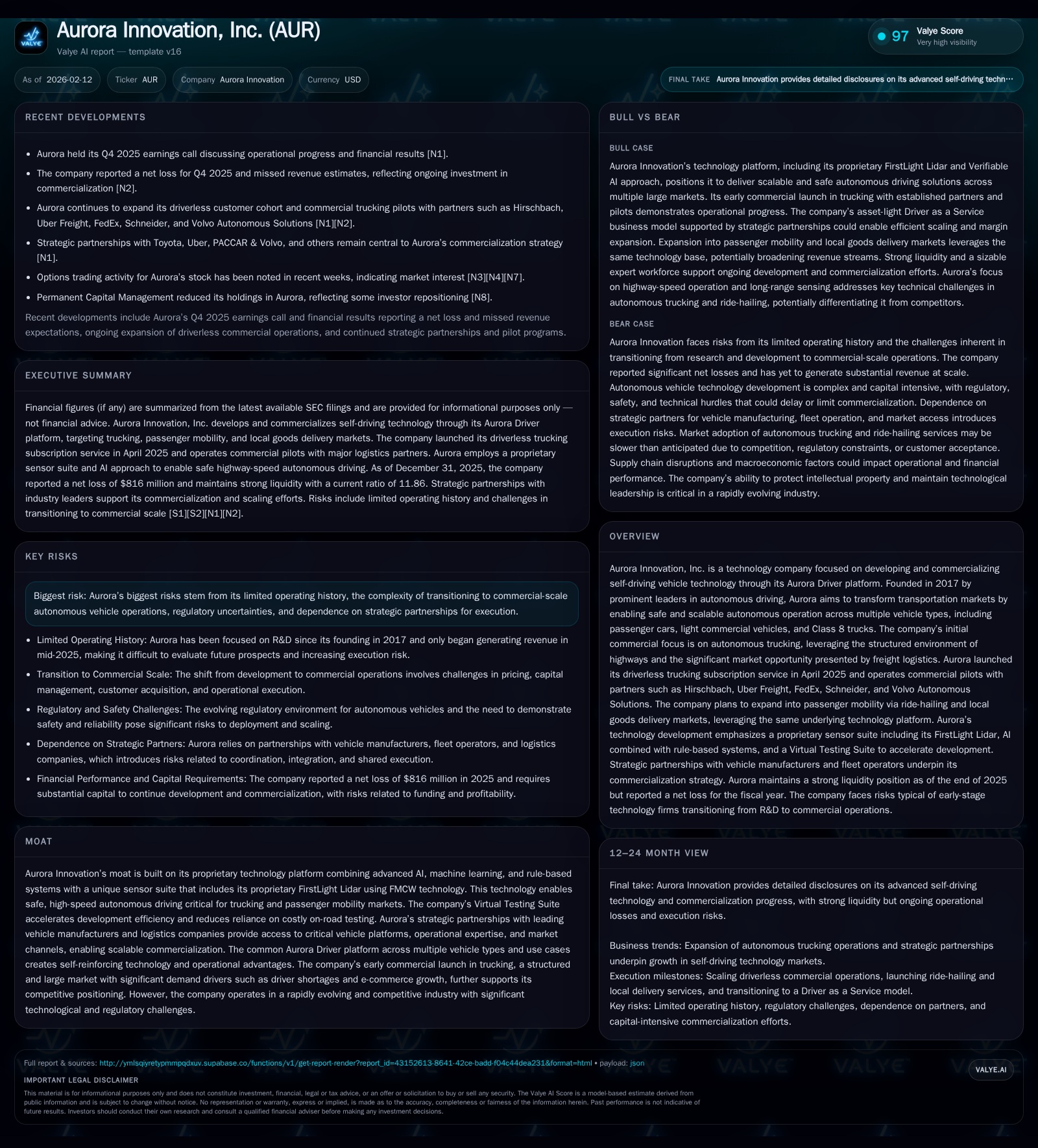

Founded in 2017 by leading autonomous vehicle technologists, Aurora Innovation has shifted from R&D to launching its Aurora Driver for Freight, pioneering driverless trucking at scale. Though the company’s proprietary AI-driven platform and partnerships position it uniquely in a competitive landscape, its steep operating losses and limited history underscore execution risks. Looking ahead, Aurora aims to expand into passenger ride-hailing and local delivery markets, leveraging extensibility of its technology amid ongoing regulatory complexities and capital demands.

From Visionary Roots to Commercial Reality: Aurora’s Evolution

Aurora Innovation emerged in 2017 from the minds of three trailblazers—Chris Urmson, Sterling Anderson, and Drew Bagnell—all renowned for their contributions to autonomous driving. This leadership pedigree fueled Aurora’s mission to fundamentally transform global transportation through self-driving technologies. Rather than narrowly focusing on a single vehicle segment or use case, Aurora engineered the Aurora Driver as a versatile platform capable of interoperating seamlessly across diverse vehicle categories—from passenger cars to heavy-duty Class 8 trucks [S1].

This strategic breadth fosters a technological feedback loop where innovation in one domain cascades benefits across others. For instance, highway driving algorithms refined for freight translate directly to passenger ride-hailing applications on similar road types. The founding team’s vision recognized early-on that scalability and adaptability would be critical levers to unlock widespread autonomous adoption.

Decoding the Aurora Driver Platform: Technology That Drives Multiple Markets

At its core lies the Aurora Driver—a proprietary system synthesizing advanced artificial intelligence (AI), machine learning (ML), and rule-based reasoning into a singular software stack. This hybrid approach balances the adaptability of AI with the predictability verified rule sets needed for safety-critical environments.

Complementing the software is Aurora's unique sensor suite featuring FirstLight lidar based on Frequency Modulated Continuous Wave (FMCW) technology. This innovation enables superior range detection and velocity measurement compared to conventional lidars—a vital advantage in high-speed highway scenarios common in freight [valye_report_excerpt]. The platform also leverages a Virtual Testing Suite that enhances development throughput by simulating myriad real-world conditions digitally, reducing reliance on costly physical road tests.

This modularity allows Aurora to deploy one driver system across multiple vehicle architectures efficiently. As such, technological advances in one vertical create shared competitive advantages company-wide [S1].

Road to Revenue: Launching Driverless Freight at Scale

April 2025 marked a pivotal milestone when Aurora launched Aurora Driver for Freight—its subscription-based driverless trucking service. Initial revenue recognition began in Q2 2025 as commercial pilots rolled out with marquee partners including Hirschbach Transportation Services, Uber Freight, FedEx, Schneider Logistics, and Volvo Autonomous Solutions [S1][N1].

These collaborations provide validation amid a structured operational environment: long-haul highway routes that benefit from predictable conditions suited for autonomy. Though this first generation service targets the enormous freight logistics market given its unit economics and scale potential, recent earnings revealed revenue missed analyst expectations in Q4 2025—highlighting early-stage commercialization headwinds [N2].

Yet these deployments establish essential playbooks for scaling operations securely while refining the platform under live network conditions.

Financial Snapshot: Cash Flows, Capital Raises, and Operating Losses

Despite promising commercial starts, Aurora remains deep in investment mode. The fiscal year ending December 31, 2025 closed with an $816 million net loss underscoring ongoing costs tied to product development, pilot operations, and infrastructure scale-up [F1]. Meanwhile, cash reserves stood at $221 million but were bolstered by robust liquidity—the company reported current assets nearly twelvefold higher than current liabilities (current ratio ~11.9), signaling effective working capital management.

Capital raising has been aggressive; since February 2025 the company executed an At-The-Market (ATM) equity offering program which yielded nearly $900 million through issuing over 150 million shares at an average price below $6 each [S1][N2]. This infusion underpins continued R&D spending and supports runway but also dilutes shareholder value amid mounting losses.

The financials reflect the inherent tension between pioneering technology investments against uncertain near-term revenue streams characteristic of nascent autonomous service providers.

Partnerships as the Cornerstone: OEMs, Logistics Giants, and Their Strategic Value

Aurora’s approach extends beyond proprietary tech—it is deeply partnership-driven. Collaborations with incumbents like Volvo Autonomous Solutions tether hardware integration know-how directly into vehicle manufacturing channels critical for scale. Similarly, logistics leaders Uber Freight and FedEx provide not only customer validation but operational insights facilitating route selection and fleet deployment strategies [valye_report_excerpt][S1].

These alliances streamline complexity around supply chains, maintenance services, fleet management financing arrangements—all pivotal elements catalyzing mass adoption. Moreover partnering mitigates capital intensity by leveraging external parties’ infrastructure rather than building end-to-end service ownership internally.

This ecosystem approach differentiates Aurora from competitors attempting vertically integrated models struggling under similar commercialization burdens.

Navigating Regulatory and Market Headwinds: Risks in Autonomous Scale-Up

Despite technological strides and strategic partners, multiple layers of risk temper near-term prospects. Regulatory frameworks remain unsettled globally; shifting safety standards along with state-by-state permit variances complicate planning horizons [S2].

Management candidly outlines risks tied to their limited operating history coupled with transitioning from R&D into commercial operations—a phase fraught with scaling execution challenges including pricing models formulation, workforce expansion particularly retaining specialized talent pools, supply chain reliability under pressure from chip shortages or component lead times [S2].

Market dynamics add another layer; macroeconomic trends could delay partner fleet expansions or dampen transportation demand during downturns affecting load volumes essential for subscription revenue growth.

Looking Ahead: Scaling Passenger Mobility and Expanding Use Cases

Leveraging freighting as foundational traction aligns with an ambitious horizon where passenger mobility becomes the next frontier—“Aurora Driver for Rides” envisages deploying autonomous ride-hailing services tapping into urban demand sectors [valye_report_excerpt]. Success here requires adapting systems from predominantly highway contexts toward more unpredictable city environments involving dense traffic patterns.

Additionally longer-term plans involve capturing local goods delivery markets characterized by last-mile complexity where smaller vehicle platforms equipped with the same core software can capture incremental addressable market share.

Cross-pollination of capabilities developed within freight—such as high-speed situational awareness—is expected to smooth transition into these adjacent spaces accelerating time-to-market advantages relative to competitors confined within narrower scopes.

Investment Thesis: Balancing High Growth Potential Against Execution Risks

Aurora embodies a high risk/high potential profile typifying autonomous vehicle startups moving beyond concept into monetization attempts [N2][F1]. Its clear strengths include deep technical moat evidenced by unique sensor fusion innovations plus widespread partner engagement validating market interest [valye_report_excerpt]. Yet unrelenting capital consumption paired with early revenue shortfalls dampen near-term profitability outlook.

Moreover competition is intensifying as well-funded rivals jockey for differentiated positioning while regulators remain cautious stalling more rapid rollout timelines. Stakeholders must weigh the promise inherent in an extensible DaaS model delivering scalable fees-per-mile revenues alongside realistic commercial scaling hurdles compounded by tangible financial pressures documented in recent filings [S2].

Options market activity around key expiry dates further signals concentrated investor attention on potential volatility driven by upcoming execution milestones [N3][N4].

Aurora’s Moat in a Crowded Autonomous Landscape: What Sets It Apart

What distinguishes Aurora amid numerous autonomous driving contenders is its holistic platform approach unified around core technical pillars: proprietary FMCW Lidar offering enhanced environmental perception coupled with integrated AI-rule hybrid software designed explicitly for verifiable safety compliance [valye_report_excerpt][S1].

This combined hardware-software synthesis paired with an expansive Virtual Testing Suite enables rapid iteration cycles critical when adapting across different vehicle classes or regional regulations.

Additionally maintaining one codebase serving trucks as well as passenger vehicles ensures efficiency gains absent in segmented competitors pursuing vertically siloed solutions.

Strategic collaborations round out this moat—investment dollars do not merely buy product development but also embed deeply within existing industrial ecosystems accelerating scaling hurdles otherwise inhibitive for pure startups either focused solely on technology or isolated fleet operation models.

This analysis is based on publicly available information including SEC filings dated February 11th, 2026 ([S1]), October 28th 2025 ([S2]), alongside recent news coverage ([N1], [N2]). It aims to objectively explore Aurora Innovation's business trajectory without offering investment advice. Market participants are encouraged to conduct additional due diligence considering dynamic regulatory developments and evolving commercial outcomes inherent in early-stage autonomous vehicle ventures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments