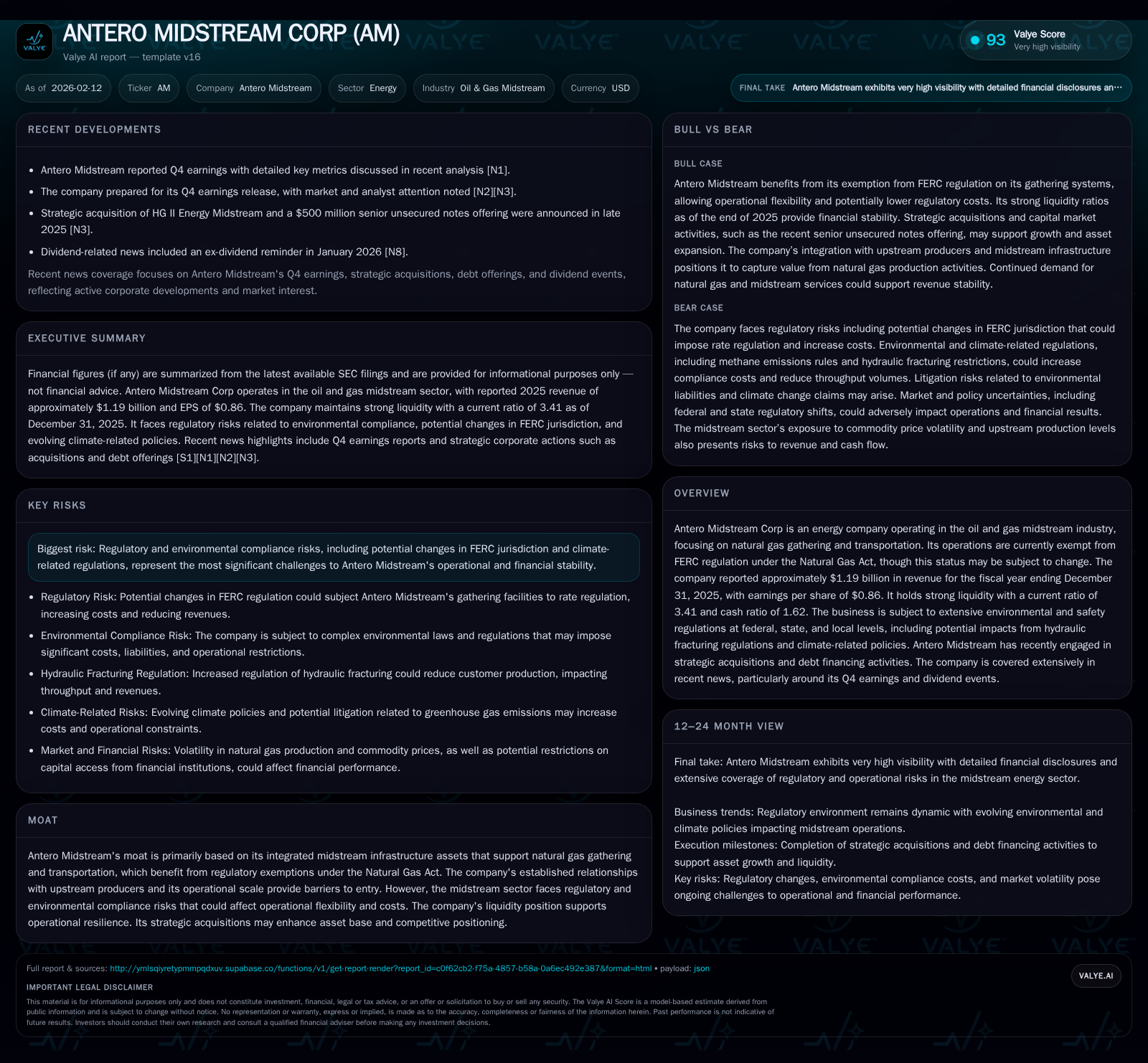

Antero Midstream Corp: Balancing Strong Earnings with Regulatory Ambiguity and Strategic Growth

Antero Midstream showcases solid Q4 financial results while navigating evolving regulatory and environmental challenges amid strategic asset expansions.

Antero Midstream Corp delivered robust fourth-quarter revenues that outpaced estimates, driven by its integrated natural gas gathering and transportation assets. However, the company faces significant regulatory uncertainty, particularly the potential loss of its Federal Energy Regulatory Commission (FERC) exemption under the Natural Gas Act, which could impose cost and operational constraints. Strategic share repurchases and dividend policies indicate shareholder value efforts even as acquisitions raise questions about leverage amid a strong liquidity backdrop. Environmental regulations, especially on hydraulic fracturing, present ongoing operational risks. Overall, Antero Midstream is managing a complex interplay of growth ambitions, risk factors, and capital discipline in a shifting energy landscape.

Robust Q4 Earnings Amid Burgeoning Regulatory Clouds

Antero Midstream’s recent fourth-quarter earnings confirmed its operational strength but also underscored mounting headwinds looming in the regulatory environment. According to official reports, the company reported revenues near $1.19 billion for 2025 — figures that outpaced several analyst forecasts [N1][F1]. Earnings per share stood at $0.86 for the full year ending December 31, 2025, reflecting sustainable profitability despite fluctuating commodity prices and midstream volume variability.

Yet, net income pressures were evident in the quarter’s bottom line [N9], a reminder that underlying conditions are less sanguine than headline numbers suggest. Central to this caution is Antero Midstream’s exempt status under the Natural Gas Act (NGA) from FERC regulation — a classification that preserves operational flexibility and shields rates from federal oversight. The company believes its gathering pipelines meet traditional tests for exemption [S1], yet the regulatory framework is far from settled. Litigation and evolving FERC positions could rescind this exemption, triggering rate regulation risks and higher compliance costs that may weigh on future results.

This juxtaposition of robust earnings momentum against an uncertain regulatory backdrop creates significant model risk for stakeholders assessing long-term sustainability.

Strategic Share Repurchases and Dividend Policies Under the Microscope

Amid these complexities, Antero Midstream has remained committed to returning capital to shareholders through dividends and share repurchases — key signals of management confidence. In 2025 alone, approximately 8 million shares were repurchased at an aggregate cost exceeding $135 million under a board-authorized $500 million buyback program that remains active [S1]. This aggressive stock buyback strategy underscores a belief in intrinsic value despite inherent sector volatility.

Dividend policy also reflects a balancing act: a quarterly dividend of $0.225 per share was declared and paid early February 2026 [S1][N11][N13]. However, dividends on the Series A Non-Voting Perpetual Preferred Stock have accumulated arrears totaling $68,750 thousand USD as of year-end 2025 [S1], highlighting the nuanced challenge of managing prioritized obligations alongside common shareholder returns.

These moves suggest an intent to maintain shareholder goodwill while navigating limited margins for capital deployment given evolving external pressures.

Decoding the FERC Exemption: A Line in the Sand for Midstream Operations

The Natural Gas Act exemption constitutes more than a regulatory footnote—it forms a structural moat protecting Antero Midstream’s business model from federal rate administration. This exemption hinges on whether the company’s pipelines are classified strictly as gathering facilities rather than transmission pipelines subject to FERC jurisdiction.

Despite no formal FERC determinations against the company’s current classification [S1], historical precedent shows this distinction has invited substantial litigation with outcomes often fluid and contingent on case specifics or legislative actions. Should FERC reclassify any facility as transmission rather than gathering, Antero would confront mandatory rate regulation under NGA or NGPA statutes.

Such an overhaul would likely reduce tariff flexibility, increase operating costs due to compliance burdens, and constrain commercial terms—potentially eroding margins substantially. Given this pivotal regulatory ambiguity persists as an overhang on corporate strategy and valuation assumptions.

Environmental Compliance Risks: The Silent Cost Pressure

Federal, state, and local environmental mandates add further layers of complexity to Antero Midstream's operations. Key among these is hydraulic fracturing regulation—affecting upstream production upstream operators rely upon—to which Antero’s midstream volumes are intrinsically tied.

Stringent controls or delays in permitting can constrict natural gas production flows entering Antero's gathering systems [S1]. Reduced throughput translates directly into lower capacity utilization rates on pipelines and processing plants, squeezing gross margins that are otherwise stable due to contractual fee structures.

Additionally, compliance expenditures associated with emissions monitoring, safety protocols, spill prevention measures, and potential penalties form variable cost components that complicate forecasting accuracy.

These environmental factors constitute a largely non-linear risk vector—sudden regulatory tightening could rapidly impair volumes where mitigation within short timeframes is not feasible.

Asset Expansion through Acquisitions: Growth or Leverage?

In pursuit of scaling its footprint and enhancing competitive positioning, Antero Midstream has actively pursued accretive acquisitions supported by fresh debt financing initiatives [valye_report_excerpt][S1]. These transactions allow consolidation of critical infrastructure assets primarily servicing prolific Appalachian Basin plays — effectively broadening service capacity and deepening customer integration.

However, with increased indebtedness comes amplified scrutiny on leverage metrics amid potentially volatile cash flows influenced by regulatory dynamics and commodity cyclicality. While current liquidity appears ample (discussed below), less accommodative financing markets or unforeseen adverse operating conditions could elevate refinancing risk scenarios.

Consequently, asset expansion strategies must be carefully balanced against prudent financial stewardship—not simply growth for scale but measured enhancement aligned with risk tolerance thresholds.

Liquidity Strength as Operational Lifeline

Supporting Antero Midstream’s navigation through this intricate environment is a notably strong liquidity profile—a rare positive in midstream sectors grappling with cyclicality. The company's current ratio sits at a robust 3.41 while cash ratio stands at approximately 1.62 [F1][valye_report_excerpt], signaling healthy short-term asset coverage relative to liabilities.

With end-of-year cash reserves north of $180 million USD cushioning day-to-day operations [F1], these metrics afford flexibility amid regulatory flux or temporary volume disruptions caused by policy or market shifts.

Liquidity strength serves not merely as a buffer but as an enabler—preserving optionality to continue strategic initiatives like share repurchases or selective bolt-on acquisitions while absorbing episodic shocks without resorting to distress financing measures.

Governance and Stakeholder Concentration Dynamics

Antero Resources owns roughly 29% of Antero Midstream's outstanding common stock [S1], placing it as a dominant shareholder capable of significant influence over governance decisions including capital allocation policies such as dividends or buybacks.

This ownership structure introduces both alignment opportunities—leveraging parent-subsidiary synergies—and potential conflicts regarding priorities between controlling interests versus minority shareholders.

The board's ongoing authorization and execution of large-scale share repurchases amidst preferred dividend arrears hint at calculated governance maneuvers balancing external perceptions against internal capital constraints.

Understanding how this stakeholder concentration shapes strategic choices will be important for observers evaluating corporate resilience and fairness across investor classes going forward.

Market Sentiment Reflected in Options and Technical Indicators

Beyond fundamentals, market sentiment indicators illustrate nuanced investor positioning around Antero Midstream’s future trajectory. Notably, surges in implied volatility within options markets point toward elevated uncertainty pricing—reflecting concerns over regulatory developments or commodity price swings [N10].

Conversely, recent technical chart analyses showed the stock crossing above key moving average thresholds suggesting tentative bullish momentum entering early 2026 [N12]. Such patterns may imply cautious optimism among traders betting on continued earnings resilience despite sector headwinds.

Taken together, these signals depict an engaged marketplace parsing complex information streams — reacting dynamically yet carefully to shifting risk-reward paradigms surrounding Antero Midstream's narrative.

Disclaimer: This report is prepared solely for informational purposes based on public disclosures and industry context available as of February 12, 2026. It does not constitute investment advice or recommendations to buy or sell securities nor reflects all possible risks associated with investing in Antero Midstream Corporation or its securities. Readers should conduct their own comprehensive analysis before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments