Decoding Woodbridge Liquidation Trust: Navigating Its Complex Legal Framework and Asset Wind-Down

An in-depth exploration of Woodbridge’s liquidation legal structure, asset management, and distribution complexities amid inherent uncertainties.

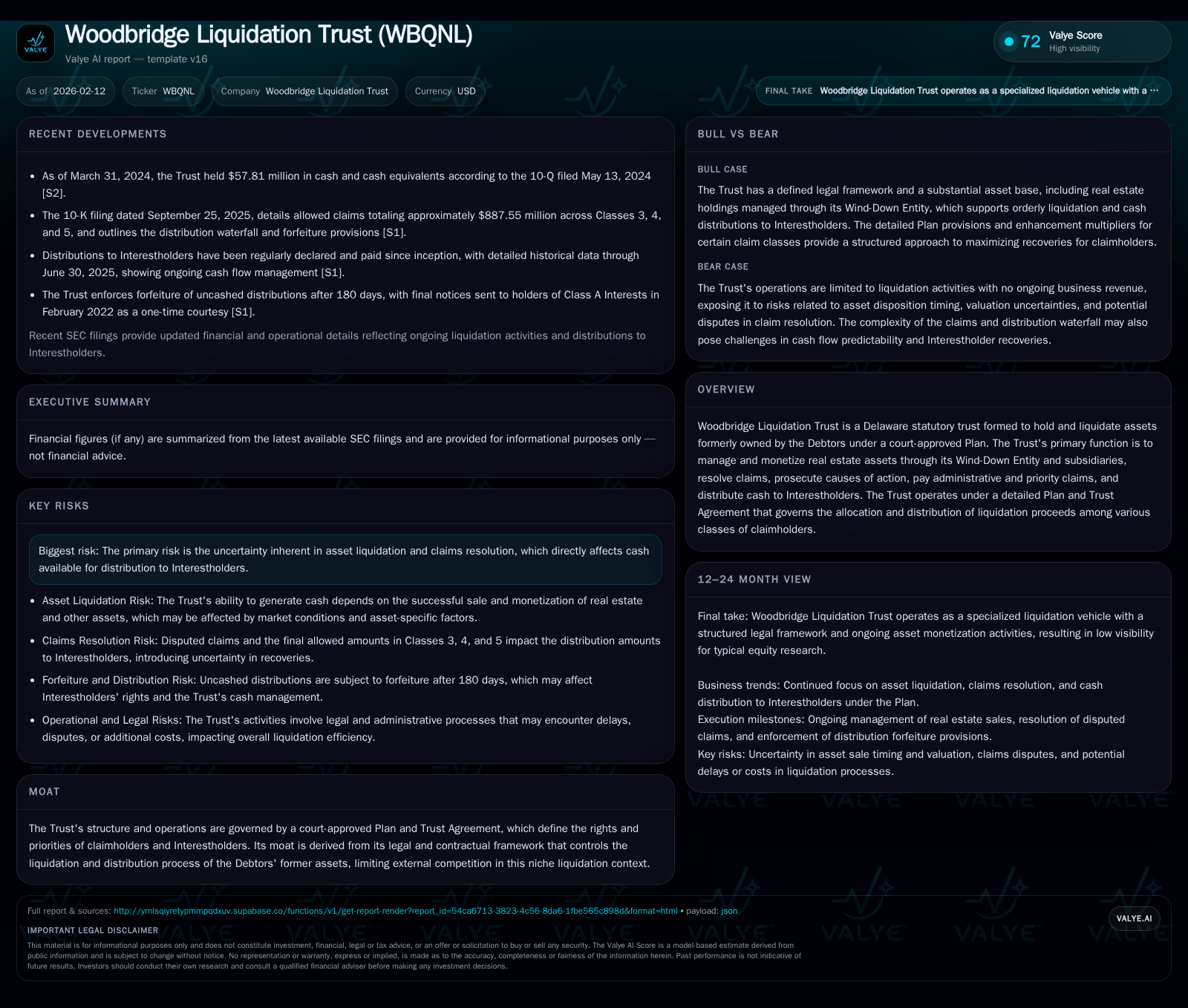

Woodbridge Liquidation Trust (WBQNL) operates under a unique Delaware statutory trust framework designed to liquidate the former debtors' real estate and other assets according to a court-approved plan. Its operations pivot exclusively on monetizing transferred real estate assets through subsidiaries, managing claims, and distributing proceeds based on a detailed claim and interestholder hierarchy. Key risks stem from asset value estimation challenges, unresolved litigation recoveries, and governance complexities within a judicially constrained environment. Investors must grasp the layered waterfall distribution structure and the tenuous yet protective legal moat that governs the trust’s niche liquidation role.

Inside the Core: Understanding Woodbridge’s Legal and Structural Framework

Woodbridge Liquidation Trust stands apart from conventional operating companies; it is not engaged in providing products or services but exists solely to unravel the financial entanglements of the former Woodbridge debtors. Formed as a Delaware statutory trust pursuant to a court-approved Plan of liquidation, WBQNL inherits a web of contractual obligations and rights carefully codified to govern its pursuit: managing and liquidating assets, resolving claims, prosecuting causes of action, disbursing funds, all within narrowly defined legal parameters [S2].

This is not corporate governance reshaped but an architecture mandated by bankruptcy law combined with detailed Plan provisions. The Trust Agreement supplements this foundation with precise instructions that prevent external interference—the ‘customers’ here are claimholders rather than retail consumers—and sharply restrict actions to those prescribed by the Plan. This creates what might be called a ‘legal fortress,’ designed more to orderly distribute residual value than to compete for new value creation.

Such a niche existence carries both benefits and burdens. While there's no traditional market competition eroding potential recoveries—the Trust’s claimholders face no rivals for their slices beyond each other—the rigid legal framework also binds management choices tightly, limiting flexibility to pivot operations or valuations outside court-sanctioned bounds.

The Wind-Down Engine: How Assets Are Managed and Monetized

Central to unlocking value within WBQNL's specialized environment is its Wind-Down Entity—a wholly owned subsidiary charged with directly holding real estate formerly owned by the Debtors [S2]. Each property was assigned on the Plan Effective Date into one of several Wind-Down Subsidiaries fashioned specifically for this task.

Operationally, this shifts Woodbridge from developer or operator into executor—monitoring market conditions, facilitating sales or development where applicable, marketing assets for liquidation proceeds. The pace, strategy, and success here determine cash inflows fundamentally impacting distributions available to Interestholders.

Yet this transition is fraught: real estate markets are inherently cyclical; properties encumber various legal or physical encumbrances; timing liquidity extraction requires balancing between maximizing asset price realization versus expediting wind-down timelines under cost pressures [S2]. These factors combine to create a challenging operational pivot where market acumen meets fiduciary duty under judicial oversight.

Priorities on Paper: The Complex Claim and Interestholder Hierarchy

Investors seeking clarity on their position within WBQNL’s capital structure must navigate a multi-layered claim classification system embedded in the Plan [S1]. Claims fall principally into three classes relevant here:

- Class 3 (Standard Note Claims): Repaid at one Class A Interest per $75 of net claim,

- Class 4 (General Unsecured Claims): Similarly converted at one Class A Interest per $75,

- Class 5 (Unit Claims): More complex, converted into fractional interests — roughly 0.725 Class A plus 0.275 Class B per $75 net claim.

Moreover, holders who elected to contribute their causes of action for prosecution received enhancement multipliers increasing their effective claim amounts by approximately 5%, reflecting incentive alignments embedded in the Plan [S1].

This complexity signals how groundbreaking this Trust arrangement is relative to traditional equity or debt holders — these synthetic constructions define not only recovery size but priority rights in cash flow waterfalls.

| Claim Class | Conversion Rate | Interest Classes | Enhancement Multiplier |

|---|---|---|---|

| Class 3 | $75 Claim = 1 Class A Interest | Class A | 105% if contributed causes of action |

| Class 4 | $75 Claim = 1 Class A Interest | Class A | None |

| Class 5 | $75 Claim = 0.725 Class A + 0.275 Class B Interest | Classes A & B | 105% if contributed causes of action |

Understanding these allocations is essential because ultimate payouts depend on these ratios interacting with total realized liquidation proceeds.

Risks Behind the Curtain: Accounting Estimates, Claims Uncertainties, and Cyber Threats

At the heart of WBQNL’s risk profile lies uncertainty — the use of Liquidation Basis accounting demands forward-looking assumptions around asset realizations and expense timings [S1]. Management must estimate when liquidation will conclude, future cash flows from sales or recoveries using market yield curves extrapolated forward.

Such estimates carry dangers; actual sales may lag expectations; legal claims may extend timelines; administrative costs such as payroll or professional fees could escalate unexpectedly. Notably, reserves for potential construction defect claims pose material unknowns that might inflate expenses beyond projections thus shrinking distributable cash [S1].

Beyond these classic uncertainties lurk more novel risks: IT infrastructure underpins critical operational processes including accounting data integrity. Woodbridge’s reliance on third-party providers introduces exposure to cyber threats—whether hack attempts or data breaches—that could disrupt operations or damage reputations [S1]. Although administrative controls exist, rising sophistication in cyberattacks renders zero risk impractical.

Finally, unresolved Causes of Action pending prosecution remain off-balance sheet items until they meet stringent recognition criteria including final court approvals. Their ultimate realization could materially alter outcomes but remains opaque currently [S1,S2].

Financial Snapshot: Cash Position and Reserve Realities

As of March 31, 2024, Woodbridge reported approximately $57.8 million in cash and equivalents—an essential liquidity cushion supporting ongoing wind-down activities [F1]. However, this figure must be considered alongside accrued reserves earmarked for anticipated contingencies such as construction defect liabilities or protracted claim resolutions documented in filings [S1].

These reserved amounts reduce immediately available funds for distribution; coupled with operating costs necessary to maintain Wind-Down Entities’ activities, they form critical constraints on cash flow timing. While sizable liquid balances suggest near-term payment capacity exists for Administrative Claims and some priority obligations, the scale of liabilities — particularly from less predictable claims — tempers any assumption that distributions will flow swiftly or fully without delay.

Prosecuting Recoveries: The Lingering Causes of Action Puzzle

The Plan permitted certain creditors — mainly Standard Noteholders and Unitholders — to contribute their prepetition Causes of Action against non-released parties into the Trust for pursuit [S1]. This gives the Trust potential access to additional funds above straightforward asset sales if such litigation succeeds.

However, current financial statements exclude expected recoveries from these unresolved litigations because revenue recognition criteria are stringent—agreements must be executed, courts must approve actions where applicable and there must be reasonable assurance collectability follows [S1]. Thus what might amount to sizable contingent assets today remain invisible numerically.

This prosecutorial role injects unpredictability in timing and quantum of recoveries—dependent on complex litigation outcomes far beyond pure asset sales dynamics—and underscores an intangible value layer that could shift investor recoveries materially upward if successful.

Dissecting Distributions: What the Waterfall Means for Investors

Any cash collected by WBQNL cascades through a prescribed priority distribution cascade known as the Liquidation Trust Interests Waterfall [S1]. This waterfall ensures systematic allocation among holders of Class A and B Interests based on claim class rules established at formation.

The mechanics are key:

- Payments first cover Administrative and Priority Claims,

- Then distribute to Interestholders following conversion formulas,

- Fractional interests are rounded following prescribed mathematical rules,

- Multipliers adjust effective claim sizes reflecting contribution choices made pre-liquidation.

Understanding these mechanisms reveals nuanced asymmetries—for example how Unit Claimholders receive combined interests versus single-class holders’ allocations—and influences expectations about timing delays as thresholds must be met before lower tiers receive distributions.

Such waterfall structures typify complex bankruptcy restructurings but take on heightened importance here given liquidity variability.

Governance in Limbo: Roles of the Liquidation Trustee and Supervisory Board

Oversight falls chiefly on the Liquidation Trustee acting under supervision by a Supervisory Board both appointed consistent with Plan terms [S2]. These entities manage daily wind-down activities including assets monetization decisions, claims litigation management, administrative payments coordination while remaining compliant with judicial mandates.

While serving critical strategic roles akin to executive management in active companies,their authority operates within restrictive boundaries consented by bankruptcy courts making governance inherently ‘soft’. Decisions often require court notifications or approvals limiting unilateral strategic shifts but ensuring transparency/protections for interest holders.

This governance limbo adds layers both preventing rash decisions but potentially slowing responsiveness when market opportunities arise requiring swift action—a double-edged sword influencing performance outcomes.

The Moat in a Melting Ice Cube: Competitive and Legal Barriers in Liquidation

Unlike traditional moats based on consumer loyalty or technology advantages Woodbridge’s moat derives purely from its entrenched legal-contractual framework underpinning liquidation process control [valye_report_excerpt]. External competitors cannot intervene in asset disposition directly nor challenge distribution entitlements without going through drawn-out legal proceedings—a formidable barrier protecting existing Interestholders’ slices.

Yet this moat resembles ice slowly melting rather than solid rock; it exists as long as litigation channels remain intact but fragile operational execution can rapidly erode ultimate realizations. Unlike operating businesses seeking growth defensibility this moat simply sets boundaries that constrain rather than propel value creation resulting in limited competitive dynamics but persistent fragility tied directly to underlying asset conditions.

Hence valuation perspectives should treat this moat cautiously recognizing its protective nature against outside competition yet exposed vulnerability caused by dependency on external economic factors affecting recovery magnitude/timing.

Looking Ahead: Potential Outcomes and Investor Takeaways

Long-term results for WBQNL hinge crucially on uncertain variables – duration until full liquidation completion; real estate market volatilities impacting realized prices; efficacy prosecuting Causes of Action; evolving reserve needs tied to claims resolution timelines; adherence to strict waterfall distribution protocols all frame possible outcomes ranging dramatically between modest gains distributed slowly versus protracted timelines suppressing near-term payments [S1,S2,valye_report_excerpt].

Investors must therefore orient expectations cautiously—while ultimate distributions are plausible over horizon given sizeable underlying assets plus latent legal recoveries prospects,timing unpredictabilities impose challenges embedding risk premiums accordingly.

A keen appreciation for woodboarding’s unique trust-based liquidation mechanics coupled with vigilant monitoring of ongoing filings especially relating to reserves changes or litigation developments will better inform stakeholders about evolving payout prospects. Ultimately understanding how this legal-financial hybrid vehicle functions provides clarity whether approaching from creditor recovery standpoint or secondary market interest holder perspective.

Disclaimer: This analysis is intended solely for informational purposes describing Woodbridge Liquidation Trust's operations based on publicly available disclosures as of early 2026. It does not constitute investment advice nor an endorsement or recommendation concerning securities issued by WBQNL.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments