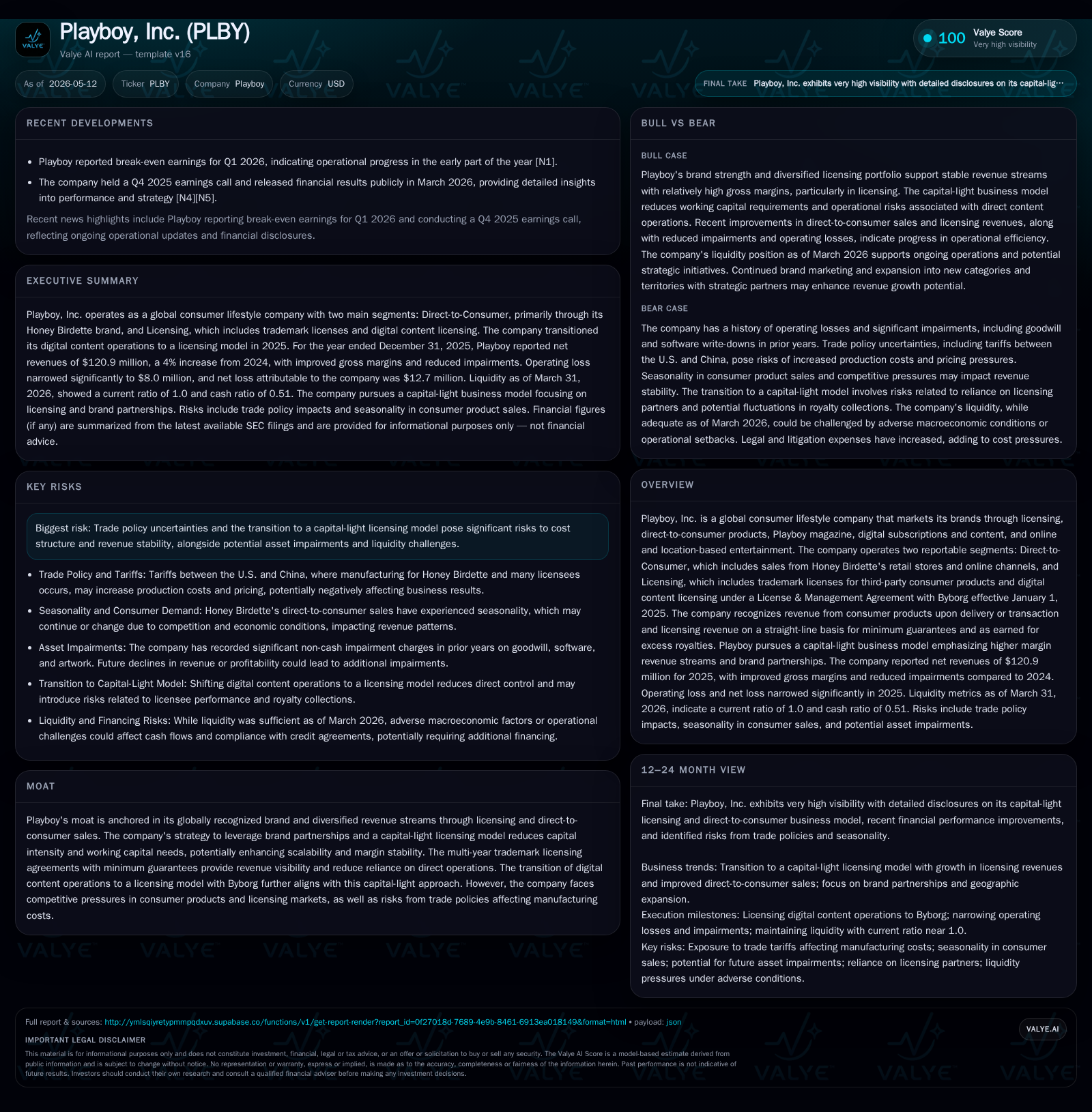

Playboy, Inc. Advances Capital-Light Model with Licensing Expansion and Q1 Break-Even Result

Q1 2026 results reflect strategic shifts toward licensing-led growth amid trade-related risks and legacy retail challenges.

Playboy, Inc. reported break-even earnings for Q1 2026, marking a pivotal step in its transition toward a capital-light business model centered on licensing revenues, particularly under its long-term agreement with Byborg. The company’s dual-segment structure leverages direct-to-consumer sales via Honey Birdette alongside broad trademark licensing, including digital content licensed to Byborg and an evolving China joint venture. While global brand recognition and diversified licensing agreements underpin revenue visibility, Playboy faces margin pressures from U.S.-China trade uncertainties and must monitor execution risks related to JV integration and competitive consumer markets.

Q1 2026 Operating Update Highlights

In its latest quarterly filing dated May 11, 2026 [S2], Playboy disclosed a break-even operational performance for Q1 2026—a significant inflection from prior quarters characterized by operating losses. This improved result reflects the ramp-up of guaranteed royalties under the License & Management Agreement (LMA) with Byborg which commenced January 1, 2025, contributing stable cash flows from the digital content licensing segment. Additionally, Honey Birdette's direct-to-consumer (DTC) operations showed resilience with enhanced full-price product sales supporting gross profit. A material event filing [S3] confirmed progress on the formation of a new China joint venture (JV) with UTG scheduled to close by March-end 2026, aiming to solidify Playboy's presence in a key licensing market that generated approximately 10% of total revenues historically.

The quarter’s break-even results underscore early benefits from the capital-light business transition while highlighting still-evident legacy cost pressures amid cautious macroeconomic conditions [N1]. The detailed SEC narrative emphasizes stable revenue recognition—with consumer product revenues booked upon delivery and licensing fees recognized over time based on minimum guarantees plus excess royalties—offering clarity on cash flow dynamics underpinning this shift [S2].

Business Model and Revenue Streams Driving Brand Growth

Playboy has strategically repositioned itself as a global lifestyle consumer brand primarily monetized through two reportable segments [S1]:

Direct-to-Consumer (DTC): Encompasses sales of Honey Birdette products via its omnichannel platform—51 physical stores across three countries as of late 2025 combined with e-commerce channels. This segment generates revenue upon product delivery and faces inherent seasonality impacting sales cadence.

Licensing: Central to Playboy's capital-light pivot is its robust licensing portfolio spanning trademark licenses across apparel, accessories, hospitality venues, digital gaming platforms, location-based entertainment venues, and notably digital media subscriptions licensed exclusively to Byborg under the long-term LMA. This contract includes minimum guaranteed royalties amounting to $20 million annually plus additional performance-linked excess royalties.

The LMA also grants Byborg exclusive rights to develop Playboy-branded adult content services—a strategic expansion reflecting evolving consumer engagement models away from direct operational involvement toward partnership-driven growth [S1]. Concurrently, the divestment of certain digital assets into licensing agreements underscores management’s intent to reduce capital requirements while leveraging brand strength.

Moreover, the company actively expands into new international territories supported by franchise-like arrangements such as the Chinese JV with UTG set for completion by March 31, 2026—a move intended to increase localized market penetration and capture rising consumer demand in Asia [S1]. This JV evolution follows termination of the prior arrangement with CTL and aims to enhance operational control and scalability.

Competitive Positioning in Licensing and Direct-to-Consumer Retail

Playboy enjoys a distinct competitive moat built on its globally recognized trademark—arguably one of the world’s most iconic lifestyle brands—and diversified monetization avenues. Licensing arrangements benefit from scale effects whereby fixed intellectual property assets generate recurring income streams across multiple categories without proportional increases in capital outlay or working capital needs.

In lifestyle brand licensing markets marked by fragmentation and intense competition for shelf space and consumer mindshare, Playboy's heritage brand recognition provides pricing leverage with third-party licensees who gain marketing cachet by association. However, consumer product retail remains challenging amid inflationary cost pressures exacerbated by U.S.-China tariff regimes impacting manufacturing inputs for Honey Birdette products as well as many licensees sourcing from China [S1]. These factors pressure gross margins within DTC sales despite increased full-price selling.

Honey Birdette’s omnichannel footprint—including flagship brick-and-mortar stores complemented by online sales—is strategically positioned but exposed to discretionary spending cycles and retail industry headwinds that demand continuous innovation in product mix and customer experience to maintain relevance [S1]. Switching costs remain modest for consumers in fashion-adjacent categories where brand loyalty is fluid.

Sector Tailwinds and Obstacles Affecting Growth Trajectory

Several tailwinds underpin Playboy’s growth outlook:

- The Byborg LMA provides royalty minimum guarantees that deliver predictable top-line revenue,

- The China JV targets one of the fastest growing lifestyle markets globally,

- The relaunch of Playboy magazine in 2025 bolsters brand engagement through editorial content supporting licensing categories,

- Expansion into emerging consumer goods verticals, including gaming and experiential entertainment.

These drivers align well with observed KPIs such as increased licensing fee receipts disclosed through minimum guarantees plus excess royalties payments exceeding baseline targets [N1]. Additionally, stabilizing DTC volumes at Honey Birdette indicate improving consumer perception aiding full-price sell-through rather than discount-driven clears [S7].

However, obstacles linger:

- Macroeconomic uncertainty persists post-pandemic altering discretionary budgets,

- Tariff-induced cost inflation raises risk of price escalation that may compress volumes,

- Regulatory environments in target markets like China can impose access complexity,

- Competitive landscape for premium branded lingerie/niche experiential entertainment narrows pricing power margins.

These risks suggest growth prospects are neither purely structural nor immune to cyclical hiccups but require disciplined execution and agile market adaptation.

Key Risks from Trade Policy and Asset Impairments

U.S.-China trade tensions represent one of the most tangible risks highlighted by Playboy’s disclosures given its reliance on Chinese manufacturing for Honey Birdette products as well as many licensee supply chains [S1]. Tariffs have recently fluctuated but remain elevated in some pathways affecting input costs directly or indirectly passed onto consumers potentially constraining demand.

Financially significant asset impairments affected prior years—$22 million charge mostly in 2024 driven by goodwill/write-downs—but no impairments were recorded during fiscal year 2025 indicating some stabilization [S1]. Nonetheless, management acknowledges continued vulnerability should revenue or profitability deteriorate anew triggering further non-cash charges.

Leverage remains substantial: total debt stands around $144.9 million end-Q1 2026 against cash approximating $30.2 million yielding a net debt position near $114.7 million [F1]. The company’s credit facility was amended multiple times suspending leverage ratio testing until June 30, 2026 reflecting lender accommodations amid financial constraints [S4]. Interest rates approximate double digits including payment-in-kind components elevating financing expense risk.

Cost rationalization measures such as headcount reduction expenses evidenced during model transition reveal short-term margin headwinds tied to restructuring efforts [S7]. Physical footprint lease expenses benefit slightly from sublease income yet overall corporate costs including legal continue exert pressure partially offsetting gains elsewhere.

Financial Snapshot and Balance Sheet Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $30mm | |

| 2026-03-31 | ||

| Total debt | $145mm | |

| 2026-03-31 | ||

| Net debt | $115mm | |

| 2026-03-31 | ||

| Current assets | $59mm | |

| 2026-03-31 | ||

| Current liabilities | $60mm | |

| 2026-03-31 | ||

| Current ratio | 1x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) | Date |

|---|---|---|

| Cash & Equivalents | 30,167,000 | |

| 2026-03-31 | ||

| Total Debt | 144,915,000 | |

| 2026-03-31 | ||

| Net Debt (Approx.) | 114,748,000 | |

| 2026-03-31 | ||

| Current Assets | 59,458,000 | |

| 2026-03-31 | ||

| Current Liabilities | 59,692,000 | |

| 2026-03-31 | ||

| Operating Income* | -8,028,000 | |

| FY ended |

The balance sheet portrays a leveraged entity balancing ongoing investments against the exigencies of model evolution. Continued focus on working capital management due to seasonality inherent in consumer retail will be critical alongside monitoring digital licensing flows linked to Byborg performance milestones.

Near-Term Catalysts and Execution Watchpoints

Upcoming milestones warrant close observation:

- Successful establishment of the New China JV with UTG targeted for March-end closure marking a strategic foothold for Asian market expansion,

- Renewal terms evaluation for Byborg license agreement including any forecast updates tied to excess royalty upside beyond minimum guarantees,

- Seasonal performance trends at Honey Birdette during key retail periods shaping inventory management approaches,

- Evolving trade policy developments between U.S. and China that could materially affect cost structure assumptions,

- Execution effectiveness regarding overhead reduction plans alongside potential impairment triggers if organic growth falters.

Tracking these markers will clarify whether Playboy can capitalize sustainably on brand equity while mitigating legacy operational risks intrinsic in past models.

This analysis synthesizes recently filed SEC disclosures alongside company commentary contextualized within broader industry dynamics known up to mid-2026. It does not constitute investment advice but aims to illuminate operational transitions at Playboy refining its positioning as a lifestyle branding leader navigating modern financing constraints and market realities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments