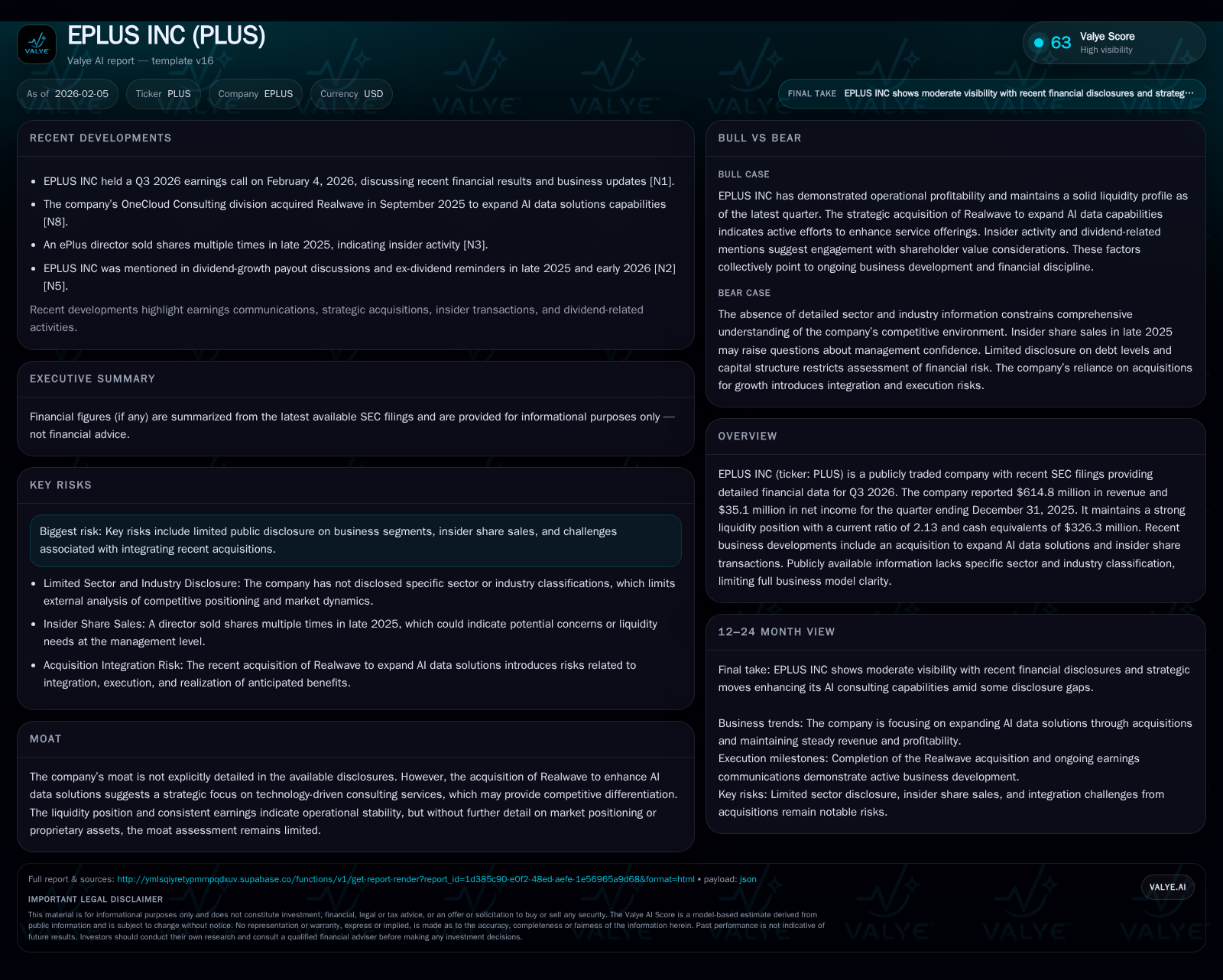

EPLUS INC's Strategic AI Acquisition Amid Strong Q3 Results and Insider Share Sales Scrutiny

EPLUS INC showcases solid quarterly financials alongside a transformative acquisition in AI data solutions, all amidst heightened insider trading attention.

EPLUS INC reported robust Q3 2026 results with revenue of $614.8 million and net income of $35.1 million, reflecting operational stability. The recent acquisition of Realwave signals a strategic pivot towards AI-driven consulting services aimed at enhancing competitive positioning, although integration risks remain. Insider share sales by company directors have raised questions, injecting a layer of complexity into the investment narrative. With limited public sector disclosure, scrutiny of financial health, strategic moves, and governance dynamics provides critical insight for stakeholders navigating EPLUS's evolving landscape.

Quarterly Financial Performance: Strengths Beneath the Surface

EPLUS INC delivered a commendable Q3 2026 financial performance with revenues reaching $614.8 million complemented by a net income of $35.1 million [F1]. These figures indicate solid gross margins and operational efficiency in the reported period ending December 31, 2025. Despite subdued market visibility on sector specifics, this consistent profitability reinforces the company's operational resilience.

Margin analysis suggests stability over prior periods, even as external economic pressures persist across broader markets. Importantly, management commentary during the February 2026 earnings call emphasized ongoing efforts to drive growth via innovation and expanding solution portfolios [N1]. The steady earnings flow provides a foundation that supports strategic growth initiatives.

Yet beneath these surface metrics lurks an analytical challenge: without clarity on business segments or industry alignment, dissecting revenue quality or sustainability is impeded. This opacity invites closer inspection of accompanying strategic moves.

Decoding the Realwave Acquisition: A Leap Toward AI-Driven Solutions

In late 2025, EPLUS announced its acquisition of Realwave—a move spotlighted for its role in augmenting AI data solutions capabilities [N1; valye_report_excerpt]. Management framed this as pivotal to transforming their consulting services toward cutting-edge technology integration, aiming to carve out differentiated market positioning.

While specific terms remain undisclosed publicly, the rationale aligns with industry-wide shifts where data analytics and AI-enhanced insights increasingly dictate competitive advantage. This suggests that EPLUS’s leadership recognizes the imperative to evolve beyond legacy frameworks toward digital-first solutions.

This acquisition potentially seeds an emergent moat centered on intellectual property and proprietary analytics tools—elements often critical in technology-driven service domains. However, the company has yet to clarify how Realwave’s technologies will be integrated or scaled within existing client engagements.

Questions linger about synergy realization timelines and operational impacts post-acquisition—areas vital for judging whether this leap truly elevates EPLUS’s strategic stature or simply introduces transitional complexities.

Liquidity and Balance Sheet Integrity: Cushion or Constraint?

From a balance sheet perspective, EPLUS maintains robust liquidity with cash and equivalents totaling approximately $326.3 million at quarter-end and a current ratio standing at an impressive 2.13 [F1; S2]. This liquidity buffer underpins both short-term obligations and financing flexibility for strategic transactions such as the Realwave acquisition.

Such financial health indicates that management is preserving option value—ensuring sufficient working capital while retaining capacity for opportunistic investments or unexpected operational demands. Importantly, the sizable cash reserves also provide a cushion to absorb integration costs or potential unforeseen expenses related to acquisition execution.

This strong liquid position mitigates certain credit risks and could enhance investor confidence amid prevailing uncertainties regarding strategic pivot outcomes.

Insider Activity Under the Microscope: What the Share Sales Signal

An area inviting deeper scrutiny is insider share-selling activity observed in late 2025 where several company directors offloaded shares multiple times [N3]. Although insider selling is not inherently indicative of negative signals, its timing near significant corporate events often prompts investor caution.

This pattern juxtaposes intriguingly against EPLUS’s solid fundamentals and growth-oriented transactions such as Realwave’s acquisition—raising questions about possible divergent internal views on future prospects or perhaps personal liquidity considerations by insiders.

Absent any explicit disclosures linking sales directly to adverse developments, these transactions nonetheless warrant attention for potential governance implications or sentiment signals which may influence market perception.

Strategic Vision Amid Limited Sector Visibility

The challenge in evaluating EPLUS is compounded by its absence from conventional sector classifications in public filings [valye_report_excerpt; S2]. This lack of straightforward categorization complicates peer comparisons and benchmarking exercises vital for investment scrutiny.

Analysts must therefore infer strategic direction primarily from managerial communications and discrete corporate actions like acquisitions rather than from externally validated market segment data.

Management appears intent on reshaping EPLUS from an opaque multi-service entity into an agile provider specializing in AI-enabled consulting solutions—a transition potentially benefiting from niche specialization but also exposing vulnerability to rapidly evolving tech landscapes.

The situation underscores a dual-edged sword: while ambiguous industry placement challenges valuation norms, it may afford strategic flexibility less constrained by legacy expectations.

Risk Vectors: Integration Challenges and Disclosure Ambiguities

Key risks highlighted in recent SEC disclosures underscore integration complexities following acquisitions alongside persistent gaps in granular segment reporting [S2; valye_report_excerpt]. Ensuring smooth assimilation of Realwave’s capabilities into existing operations looms as both an operational hurdle and a potential drag on short-term profitability.

Further muddying risk assessment is limited public disclosure regarding business lines and client concentration metrics. Such opacity makes it difficult to ascertain exposure to sector-specific downturns or competitive pressures with precision.

These factors collectively serve as caution flags suggesting stakeholders maintain vigilant observation on execution progress and forthcoming disclosure enhancements to better gauge emerging risk profiles.

Competitive Landscape and Moat Inference

Although explicit moat details are absent, clues within recent developments suggest EPLUS is cultivating competitive advantages grounded in technological innovation rather than conventional scale benefits [valye_report_excerpt; N1].

The strategic pivot toward AI-driven solutions via Realwave likely intends to differentiate through enhanced analytic capabilities and bespoke client offerings—elements critical in knowledge-intensive consulting fields where intellectual property can create durable barriers.

Nonetheless, given early-stage indications without fully disclosed proprietary assets or market share dynamics, these moat elements remain prospective rather than entrenched requiring ongoing validation through performance continuity.

The Unknown Industry Terrain: Reading Between the Lines

The absence of clear sector classification transcends mere analytical inconvenience—it materially impacts valuation modeling frameworks typically predicated on peer comparables and industry benchmarks [valye_report_excerpt].

This opacity necessitates reliance on bottom-up analysis emphasizing fundamental financial health, transaction rationale, insider behaviors, and governance conditions rather than pure top-down sector trends.

For investors accustomed to transparent categorizations, EPLUS embodies a case study in navigating uncertainty by synthesizing fragmented data points into actionable insight—a process demanding heightened due diligence rigor.

Investor Takeaways and Future Outlook

Synthesizing these threads reveals EPLUS as a company navigating transition anchored on healthy financial footing but shadowed by informational gaps and governance nuances:

- Solid Q3 financials affirm operational durability amid broader transformation efforts [F1; N1].

- The Realwave acquisition introduces promising AI capabilities yet carries integration risk requiring close follow-up [valye_report_excerpt].

- Strong liquidity ratios support continued investment capacity even as insider share sales raise interpretive caution around confidence alignment [F1; N3].

- Lack of explicit industry definition limits comparative frameworks but may allow management latitude to redefine competitive moats through innovation [S2; valye_report_excerpt].

- Risks around disclosure transparency and execution complexity necessitate ongoing monitoring before conclusive outlook judgments can be rendered [S2].

Collectively, these elements paint a picture of cautious optimism tempered by prudent vigilance—a scenario encouraging stakeholders to balance appreciation for steady underlying fundamentals against awareness of emerging strategic uncertainties inherent in evolving corporate narratives.

Disclaimer: This analysis synthesizes publicly available information without providing investment advice or recommendations. Readers should conduct their own research or consult professional advisors before making decisions related to securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments