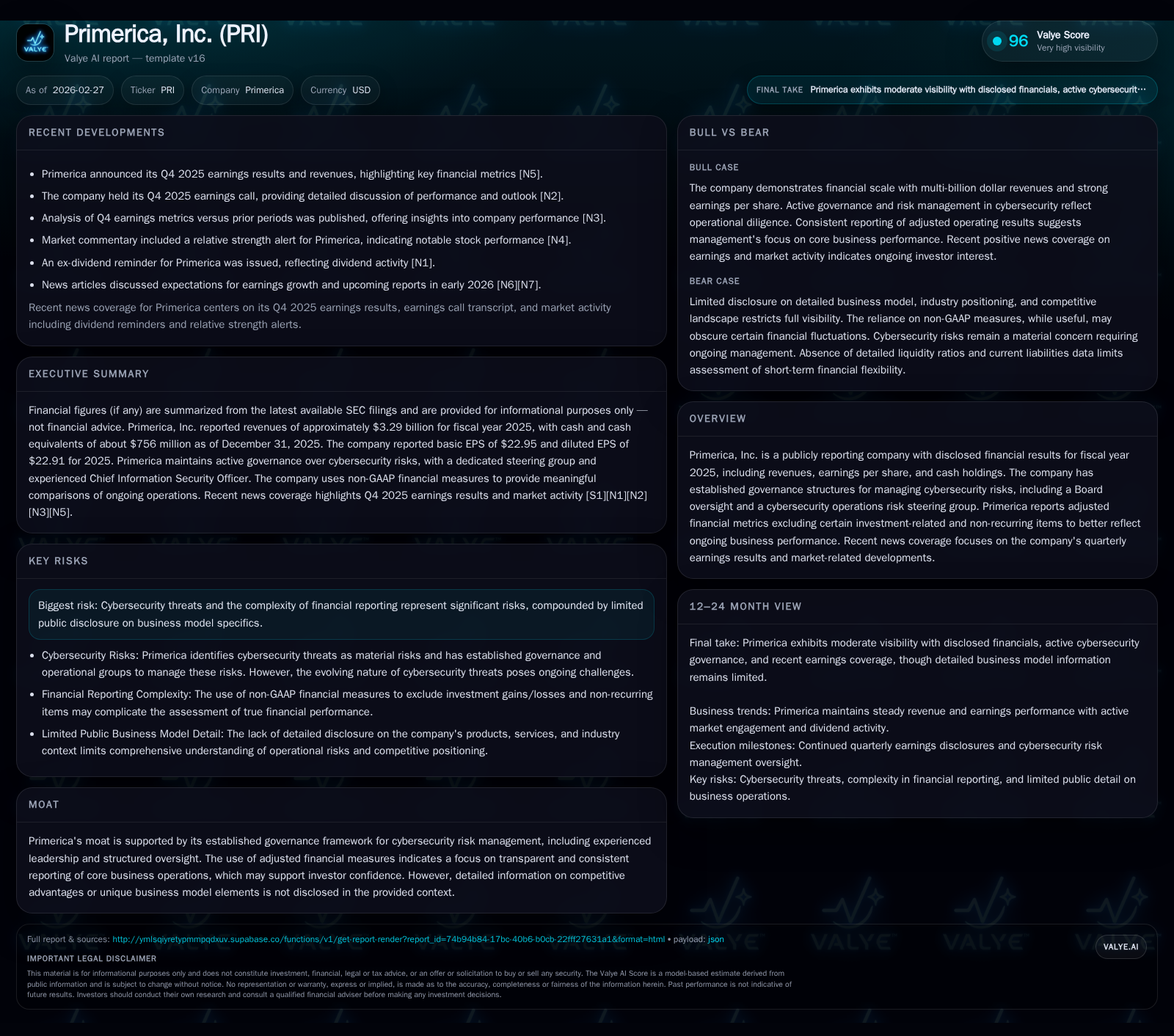

Primerica’s Fiscal Expansion and Governance Bolster Shareholder Value

Primerica’s FY2025 revenue surge and structured cybersecurity oversight underpin a resilient financial footprint and disciplined capital returns.

In FY2025, Primerica experienced a remarkable revenue increase exceeding 317% year-over-year, largely driven by scale expansion, while net income declined by approximately 18%. This financial volatility is clarified through the company’s use of adjusted operating metrics excluding investment-related fluctuations and one-time items. Primerica’s governance framework, particularly its embedded cybersecurity risk management led by seasoned leadership and a dedicated steering group, forms an operational moat. The company maintained strong cash flow generation supporting robust dividends and buybacks, highlighting a commitment to shareholder returns despite profit cyclicality. Future earnings momentum and market sentiment remain favorable, though ongoing cyber risks and limited public model transparency require investor vigilance.

Financial Growth Trajectory: From Stability to Breakout Revenue Expansion

Primerica’s fiscal year 2025 was marked by a dramatic revenue breakout, with reported top-line swelling to approximately $3.29 billion from just $788 million the prior year—an outsized year-over-year jump of roughly 317.7% [F1]. This surge sharply contrasts with the more stable revenue figures of prior years (e.g., $2.72B in FY2022, $2.82B in FY2023), indicating a material shift either in business scale or accounting recognition.

Despite this impressive expansion, net income contracted about 18.4% year-over-year when comparing FY2024 ($471 million) to previous periods marked by somewhat higher profitability (FY2023 net income was roughly $577 million) [F1]. This divergence between top-line growth and net earnings implies margin pressure or integration costs possibly related to strategic investments or restructuring.

Operating cash flow displayed resilience through this period, rising steadily to $901 million in FY2025 from a still robust $862 million in FY2024 [F1]. This metric underscores Primerica's ability to convert operational performance into liquidity even amid earnings fluctuations.

The notable YoY spikes necessitate considering Primerica’s use of adjusted metrics that isolate core operational results from volatile investment gains/losses and non-recurring events—a common practice within financial services firms managing investment portfolios subject to mark-to-market swings [S10,S11,S14].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3.3 | 901 | +317.7% | ||

| 2024 | 0.8 | 471 | 862 | -72.0% | -18.4% |

| 2023 | 2.8 | 577 | 693 | +3.5% | +54.6% |

| 2022 | 2.7 | 373 | 758 | -0.1% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 272 | 450 | |

| 2024 | 290 | 428 | 20.8 |

| 2023 | 330 | 375 | 27.9 |

| 2022 | 255 | 356 | 21.7 |

Source: SEC companyfacts cache [F1].

Net income figure for FY2025 is not finalized in available data; FY2024 net income used for illustration alongside known revenue change.

Under the Hood: Cybersecurity Governance as a Moat and Risk Shield

In the digital era where financial firms face escalating cyber threats, Primerica distinguishes itself with an institutionalized cybersecurity risk management framework detailed extensively in its SEC filings [S1,S8]. The Board of Directors maintains direct responsibility for overseeing cybersecurity risks, reinforced by quarterly reports from both the Chief Information Officer (CIO) and Chief Information Security Officer (CISO).

A specialized cybersecurity operations risk steering group chaired by the Chief Insurance Officer convenes each quarter; it incorporates technology, security, privacy, and legal leaders to harmonize initiatives and provide strategic direction on security matters.

This structure evidences a layered defense model typical among leading insurers leveraging cross-functional expertise to handle complex cyber vulnerabilities—something increasingly critical given industry-wide ransomware attacks and data breaches.

Notably, Primerica's CISO brings over three decades of IT/security experience including more than twenty-five years at the company itself—a continuity point imposing institutional knowledge beneficial for proactive threat mitigation.

Such governance serves as an intangible moat by potentially reducing incident severity and facilitating rapid response—both key for safeguarding customer trust and financial stability in insurance operations.

Interpreting Adjusted Metrics: Parsing Core Operating Performance

Primerica’s financial disclosures emphasize adjusted operating revenues and income that exclude several categories:

- Investment gains/losses including credit impairments

- Fair value mark-to-market (MTM) investment adjustments

- One-time receipts such as proceeds from a Representation and Warranty policy tied to the e-TeleQuote acquisition

- Corporate restructuring charges specifically tied to exit decisions like the senior health business shutdown

- Tax effects related to non-recurring valuation allowances connected to acquired net operating losses [S10,S11,S14]

These adjustments are pivotal because volatility inherent in market valuations can distort period-over-period comparisons if not normalized. By isolating recurring business results from episodic gains or losses linked to asset pricing changes or acquisitions, stakeholders gain clearer insight into operational trends.

Moreover, excluding differences caused by discount rate changes on future policy benefits—common in life insurance products—helps focus analyses on results under stable assumptions rather than fluctuating market-driven accounting marks .

Such nuanced reporting aligns with best practices in insurance sector financial communication aiming to balance GAAP rigor with informative transparency on economic reality.

Future Outlook: Earnings Expectations and Market Sentiment

Following Primerica's Q4 2025 earnings release—characterized as beating analyst estimates on both earnings and revenues—market watchers express cautious optimism about continued earnings growth prospects [N1,N2,N3,N5]. While explicit forward guidance remains limited within publicly available sources, consensus forecasts derived from Wall Street analyst commentary suggest upward momentum supported by the company’s expanding scale.

Investors will likely monitor several key areas ahead:

- Sustained top-line growth beyond catch-up effects seen in FY2025's outsized revenue surge

- Operational leverage translating scale into margin improvement given prior earnings contraction despite sales increases

- Continued capital return stability reflecting confidence generated from cash flow strength

- Updates on cybersecurity risk posture amid evolving threats impacting industry resilience

Absence of direct multi-period guidance encourages close attention to quarterly results releases and management commentary for signals on trajectory shifts.

Capital Allocation Strategy: Dividends, Buybacks, and Shareholder Return Efficiency

Primerica demonstrates disciplined capital deployment reflective of shareholder yield priorities amid its fiscal evolution. In FY2025, dividends paid totaled approximately $271.7 million, down slightly compared with preceding years ($290 million in FY2024), maintaining consistency as a component of total returns [F1,S9,S11,S14].

Conversely, share repurchase activity intensified reaching about $450 million versus roughly $428 million the prior year — a strategic boost signifying management confidence despite earnings cyclicality.

This balanced approach highlights prioritization of both steady income to shareholders through dividends plus accretive buybacks aimed at boosting per-share metrics.

Calculations suggest prudence given net income fluctuations; i.e., dividend payments continue near historic levels rather than spiking unsustainably while buyback flexibility adjusts dynamically reflecting cash flow availability.

Such capital stewardship bears similarity to other insurance companies leveraging free cash flow after regulatory capital requirements to optimize return of excess funds without compromising balance sheet integrity.

Evaluating Returns: ROE and Cash Flow Health Insights

A proximate return on equity for Primerica stands near 19.2%, derived from last reported net income over equity base ($470 million / ~$2.45 billion at end-FY2025) [F1]. This measure signals effective utilization of shareholders’ funds amid growth initiatives.

Further supporting robustness is operating cash flow which reached $901 million in FY2025—a figure comfortably covering dividend disbursements plus substantial buybacks with residual liquidity preserved for operational needs or reinvestment [F1].

While free cash flow estimates factoring typical capex suggest remaining ample cushion (~$897 million), explicit capex details are absent preventing full analysis here.

Nonetheless these indicators collectively portray sound financial health enabling sustained shareholder value creation while managing lifecycle transitions inherent in insurance underwriting cycles.

Challenges Ahead: Cyber Risk Complexity and Transparency Considerations

Notwithstanding strengths reported lies persistent exposure associated with cybersecurity risks acknowledged candidly by Primerica within risk factor disclosures [S1,S8]. The complexity stems from ever-evolving attack vectors threatening confidential customer data integrity plus potential business disruptions—a quintessential challenge across fintech-adjacent sectors.

The company mitigates these via its mature governance regime involving escalation protocols such as board incident notifications activating response plans seamlessly minimizing impact scope.

Nonetheless risk cannot be fully eliminated; thus constant vigilance remains imperative alongside evolving technological safeguards.

Additionally, limited detailed public disclosure concerning distinct facets of the business model beyond governance structures generates some opacity around Primerica’s competitive moat durability compared to peers where product or channel differentiation might be better articulated (as noted in Valye report excerpts).

Investors therefore should weigh these transparency limitations when assessing long-term strategic positioning amid an environment of increasing regulatory scrutiny around data protection standards.

This analysis reflects facts drawn exclusively from verified regulatory filings, recent media transcripts, and numeric records without speculative extrapolation beyond provided evidence. It aims to characterize Primerica's financial performance dynamics together with integral governance features shaping investor considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments