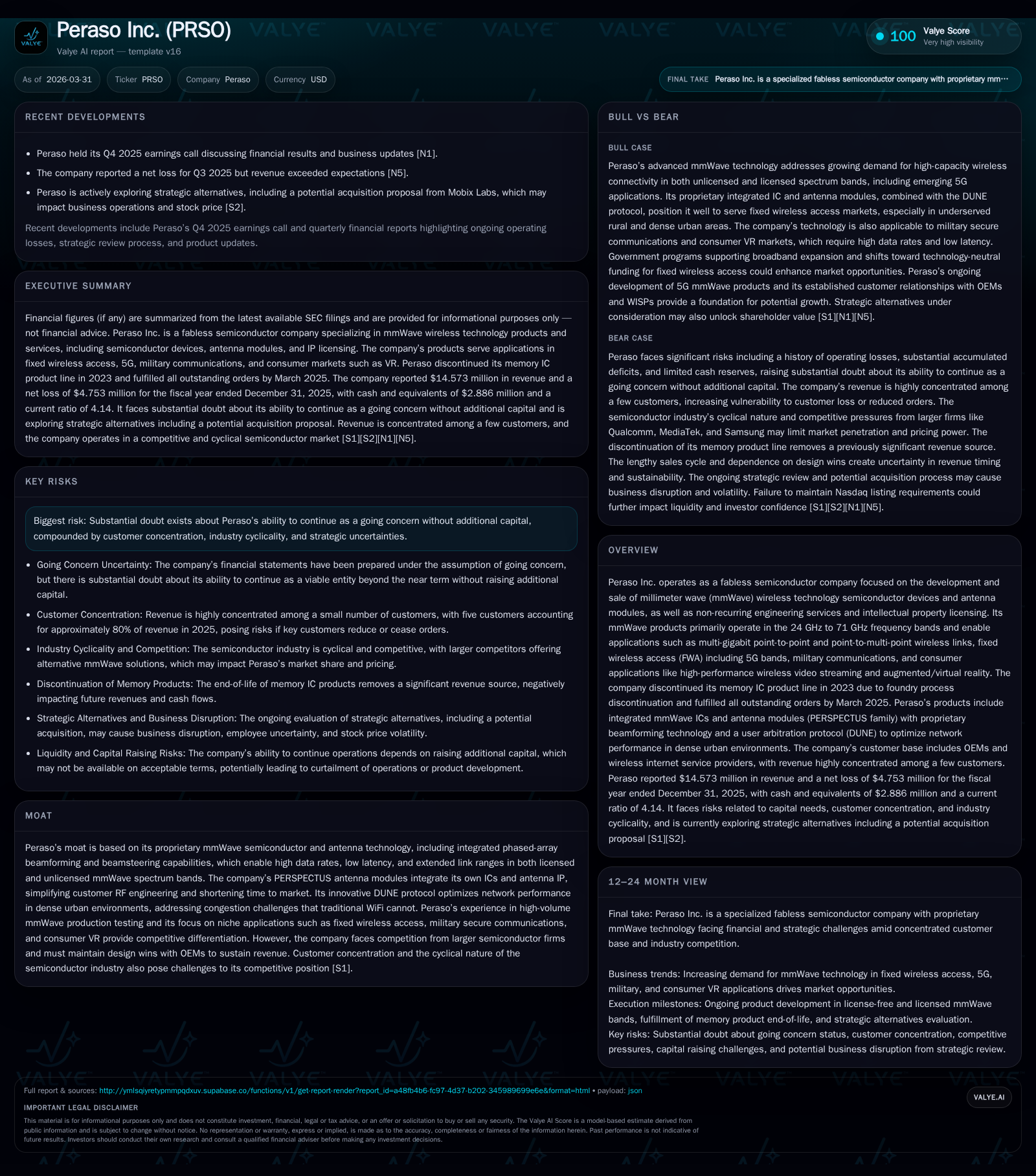

Peraso Inc. Navigates Transition to mmWave Technology Amid Revenue and Capital Challenges

Peraso Inc. focuses on millimeter wave (mmWave) semiconductor devices as it manages revenue pressures, customer concentration, and liquidity concerns.

Peraso Inc., a fabless semiconductor company specializing in integrated mmWave technology for wireless communications, has seen slight revenue decline alongside ongoing operating losses. The company fully exited its memory product line by end-2025 and now concentrates on mmWave ICs and antenna modules for applications including fixed wireless access (FWA). With a highly concentrated customer base and long sales cycles, growth depends on securing new design wins and navigating industry cyclicality. Capital adequacy remains a key risk with modest cash reserves and significant accumulated deficits, underscoring the importance of additional financing to sustain operations.

Business Overview and Historical Performance

Peraso Inc., formerly MoSys Inc. prior to its December 2021 acquisition of Peraso Technologies, operates as a fabless semiconductor company focused on developing millimeter wave (mmWave) technologies primarily for wireless communications [S1][S4]. Its product portfolio includes integrated mmWave ICs and phased-array antenna modules that operate mainly between 24 GHz and 71 GHz. These products enable applications such as multi-gigabit point-to-point (PtP) links up to 25 km, point-to-multipoint (PtMP) fixed wireless access (FWA), military communications, and consumer applications like high-performance wireless video streaming and augmented/virtual reality (AR/VR) [S4][S20].

Historically reliant on a memory IC product line serving cloud networking and data center markets, Peraso ceased production of these memory products in 2024 due to the discontinuation of the wafer fabrication process by its sole foundry, TSMC. Remaining orders were fulfilled by March 2025, ending meaningful revenue contributions from this segment [S1][S6][S17].

Financially, revenue decreased slightly from approximately $14.87 million in fiscal year (FY) 2022 to about $14.57 million in FY 2024, reflecting a roughly -2% change over this period as the company transitioned fully toward mmWave products [F1]. Operating losses narrowed significantly from -$32.3 million in FY22 to -$12.4 million in FY24 and further improved to -$4.8 million in FY25 despite continued unprofitability [F1]. Net losses followed a similar trend.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | -6 | -5 | +55.7% | |

| 2024 | 15 | -11 | -5 | -12 | +36.1% |

| 2023 | -17 | -5 | -21 | +48.2% | |

| 2022 | 15 | -32 | -16 | -32 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -102.5 |

| 2024 | -5 | -309.5 |

| 2023 | -5 | -411.3 |

| 2022 | -17 | -212.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue for FY23 is not explicitly reported but other financial metrics provide performance continuity.

Growth Prospects

Peraso’s growth prospects focus on expanding adoption of its proprietary mmWave technology by original equipment manufacturers (OEMs) targeting unlicensed and licensed spectrum applications such as fixed wireless access using its PERSPECTUS antenna module family [S20]. These modules combine internally developed ICs with phased-array beamforming antennas designed to deliver high data rates, low latency, and extended range communication at frequencies where signal attenuation is challenging [S18][S20].

The company's DUNE arbitration protocol aims to alleviate network congestion issues typical in dense urban environments where traditional WiFi protocols underperform [S20]. This innovation could differentiate Peraso as urban FWA deployments increase.

Additional target markets include military communications requiring secure, reliable mmWave links and emerging consumer AR/VR segments demanding cable-free high-throughput wireless connections [S1][S4].

However, challenges temper these opportunities:

- Sales cycles are lengthy—ranging from one to three years from design win to volume shipments—adding unpredictability [S7][S26].

- Customer concentration risk is high; five customers represented approximately 80% of revenue in FY25 while two customers accounted for over 90% of trade receivables as of year-end [S5][S22].

- Competition is intense with large semiconductor firms like Qualcomm dominating licensed 5G RF front-end markets; Peraso’s unique dual-band solutions focus on FWA niche segments [S18][S21]. MediaTek and Samsung are also notable competitors.

- Market acceptance risks include potential supplier switching by OEMs or bundling strategies by competitors that could limit Peraso’s penetration [S16][S25].

- Semiconductor industry cyclicality continues to pose operational risks via downturns impacting R&D spending and customer procurement timing [S10][S19].

Milestones and Outlook

While explicit forward guidance is not provided, Peraso emphasizes priorities such as winning new OEM design contracts with partners including Ubiquiti and multiple Wireless Internet Service Providers (WISPs), particularly in Africa deploying unlicensed spectrum solutions [N1][S7][S21]. Key milestones involve ramping volume shipments following design wins after customer validation processes that can span multiple years.

The completion of the memory product exit by end-2025 represents an important milestone that eliminates variability from legacy product lines but also increases dependence on mmWave innovations for future revenues [S6][S17]. Retention of existing customers such as WeLink/Ketsen Networks alongside securing new ones will be critical indicators of progress.

Potential strategic transactions under evaluation—including a non-binding acquisition proposal from Mobix Labs—may influence future scaling or liquidity options [S23]. Progress within licensed mmWave markets where integration barriers are higher will also provide insight into longer-term prospects.

Returns and Capital Allocation

Peraso reported an approximate negative return on equity of -102.5% for FY25 based on net losses relative to equity value at year-end, reflecting ongoing operating deficits [F1]. Operating cash flow remained negative at about -$5.6 million with free cash flow near -$5.7 million after modest capital expenditures around $0.1 million annually, indicating limited investment outside core research and development activities [F1].

At December 31, 2025, cash and cash equivalents totaled approximately $2.9 million against current liabilities near $1.3 million, resulting in a current ratio exceeding four which signifies short-term liquidity sufficiency but overall constrained capital given sustained cash burn and an accumulated deficit surpassing $181 million [F1][S6].

No recent share repurchases or dividends have been reported; management prioritizes conserving cash for operational sustainability and growth investments [F1]. The company acknowledges substantial doubt regarding its ability to continue as a going concern without additional capital raises—critical for sustaining operations—highlighting the importance of equity or debt financing despite dilution or restrictive covenant risks [S2][S6][N1].

Competitive Positioning and Risks

Peraso’s proprietary phased-array beamforming technology enables integration advantages at challenging mmWave bands by combining internally developed ICs with antenna modules that simplify system designs while reducing costs for customers [S18][S20]. The DUNE protocol further enhances network performance addressing interference issues common in dense deployment scenarios.

Nonetheless, competition remains strong with established semiconductor conglomerates leveraging scale advantages—Qualcomm notably offers aggregated mobile RF solutions though sometimes requiring compromises that Peraso’s FWA-focused approach seeks to avoid [S18][S21]. Success heavily depends on securing early design wins given long development timelines detailed by management [S7][S26].

Key risks include:

- Ongoing funding uncertainty which may limit execution capabilities or necessitate workforce reductions causing strategic disruption.

- High customer concentration exposing credit risk alongside dependency on key partners such as Ubiquiti and select WISPs whose loss would materially impact revenue stability [S7][S22].

- Supply chain vulnerabilities centered around sole-source foundries and contractors risking delays amid global chip shortages affecting timely order fulfillment [S19].

- Intellectual property enforcement challenges within crowded patent landscapes potentially diverting resources through litigation if claims arise [S11][S12].

- Semiconductor industry cyclicality exacerbating operating fluctuations especially during downturn periods impacting R&D investment levels [S10].

Summary

Peraso Inc.’s strategic pivot toward advanced mmWave wireless semiconductor solutions presents compelling technological advantages supported by proprietary phased-array antenna modules tailored for growing fixed wireless access markets among others. Despite this positioning, the company faces persistent challenges translating innovation into stable profitability or consistent revenue growth due to legacy product discontinuation impacts, concentrated customer bases, ongoing operating losses near $5 million annually despite progress, extended sales cycles limiting near-term visibility, coupled with capital adequacy concerns raising going concern flags absent external financing. Effective execution over coming quarters requires maintaining client design momentum amid competitive pressures while prudently managing cash flows against supply chain constraints characteristic of semiconductor manufacturing globally. Investors should monitor developments including new design wins across licensed/unlicensed bands alongside funding initiatives essential for operational continuity.

Disclaimer: This analysis is based exclusively on publicly available information without investment advice or forecasts regarding Peraso Inc.'s future financial results or stock performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments