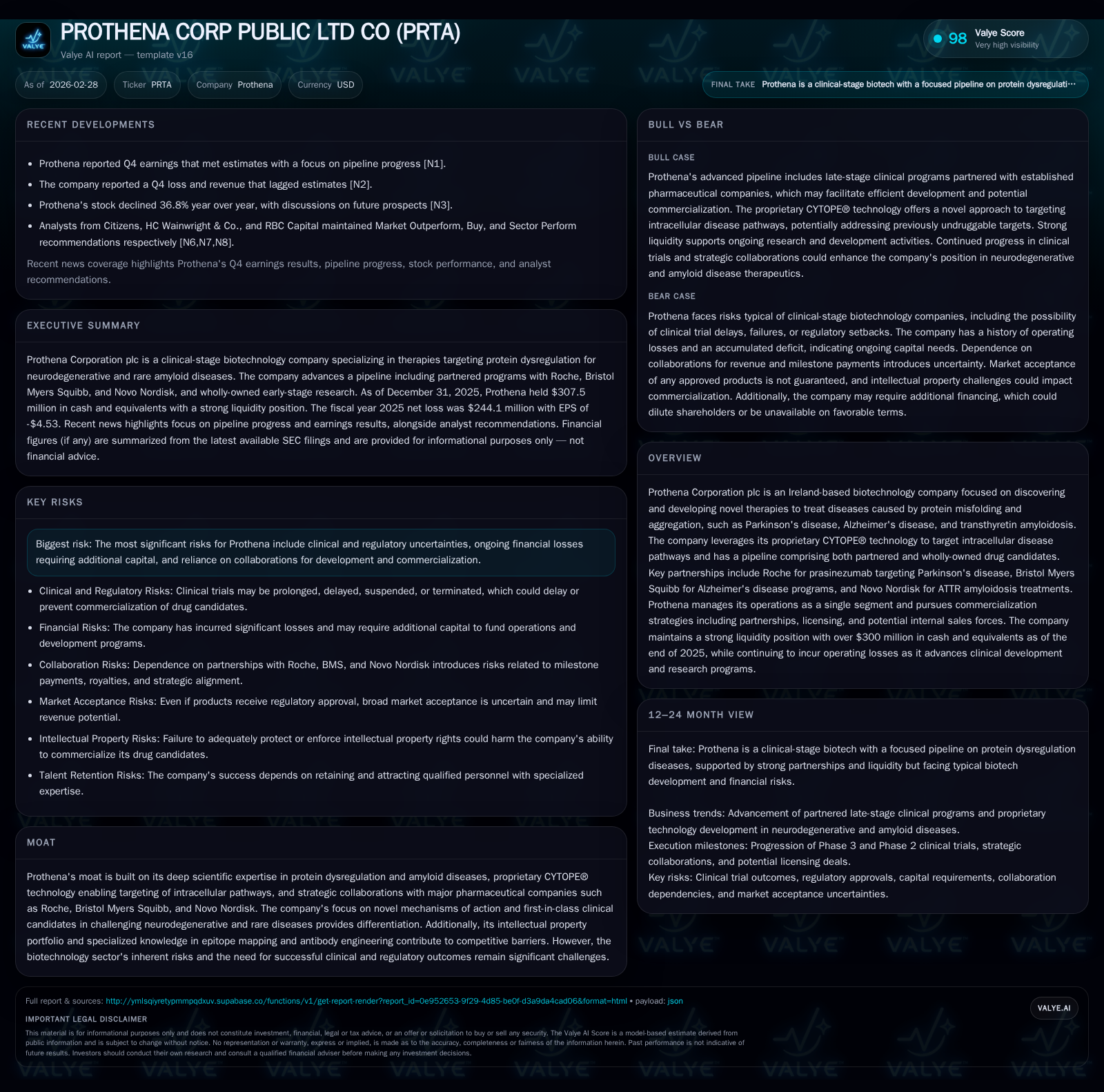

Prothena’s Pipeline Momentum Counters Rising Losses in Protein Misfolding Therapeutics

Prothena Corporation leverages proprietary CYTOPE® technology and major pharma partnerships to advance therapies for protein aggregation diseases but faces intensifying operating deficits and capital requirements.

Over recent years, Prothena has steadily increased its revenue driven by collaborations, yet operating losses have deepened substantially due to escalating research and development expenses typical of clinical-stage biotech firms. Its unique CYTOPE® platform targeting intracellular protein misfolding pathways underpins a diversified pipeline in Parkinson’s, Alzheimer’s, and ATTR amyloidosis, bolstered by key alliances with Roche, Bristol Myers Squibb, and Novo Nordisk. Despite a robust cash position providing runway into the near term, the company must navigate clinical readouts and secure additional financing to sustain its ambitious growth trajectory amid inherent regulatory risks.

Historical Growth: Revenue Trends and Operating Performance

Prothena's financial history reveals a modest top-line increase from $171K in 2016 to $256K by fiscal year-end 2019, illustrating limited revenues characteristic of pre-commercial biotechnology enterprises where income primarily derives from milestone payments rather than product sales [F1]. This plateaued revenue base has not kept pace with sharply escalating operating costs. Operating income deteriorated markedly over recent years—registering a loss of $214.6 million in 2025, a near doubling compared to prior years (-$154.6M in 2024 and -$191M in 2023) [F1]. The net income trend mirrors this trajectory, plunging to a $244.1 million loss in the latest reporting period.

This widening gap between revenue and operating expense can be attributed chiefly to intensified investment in research and development programs across Prothena's pipeline targeting protein misfolding disorders—a capital-intensive stage typical before drug commercialization. The resultant negative operating cash flows reached -$163.6 million in 2025, signaling substantial burn that underscores the company's reliance on external funding sources for sustainability [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -244 | -164 | -215 | -99.6% |

| 2024 | -122 | -150 | -155 | +16.8% |

| 2023 | -147 | -134 | -191 | -25.7% |

| 2022 | -117 | -109 | -132 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -87.0 |

| 2024 | -25.1 |

| 2023 | -26.2 |

| 2022 | -18.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY calculated using available data points; operating income and net loss indicate steep increases in losses aligned with R&D scale-up.

Scientific Differentiation: Proprietary CYTOPE® Technology and Portfolio Overview

At the core of Prothena’s scientific moat lies the proprietary CYTOPE® platform designed for intracellular targeting through precision epitope mapping of misfolded proteins implicated in neurodegenerative diseases. This approach diverges from conventional extracellular antibodies by enabling therapeutic intervention within cellular pathways driving aggregation disorders such as Parkinson’s (alpha-synuclein), Alzheimer’s (tau protein), and transthyretin amyloidosis (ATTR) .

The platform enables engineering antibodies with specificity to pathological epitopes—a complex undertaking requiring advanced biomolecular insights that form high barriers to entry. Such intracellular targeting is poised to revolutionize treatment paradigms where extracellular agents have shown limited efficacy.

This scientific differentiation supports an evolving pipeline encompassing both wholly-owned assets advancing through early-phase trials alongside partnered candidates progressing toward later stages. Notable wholly-owned assets include clinical candidates addressing rare peripheral amyloidopathies while partnered programs gain development leverage through pharma alliances.

Key Collaborations Driving Pipeline Advancement

Prothena's strategic partnerships are pivotal pillars underpinning its drug development progress:

Roche holds exclusive worldwide rights for prasinezumab targeting alpha-synuclein in Parkinson’s disease under a license that includes milestone payments tied to clinical trial initiation and patient dosing benchmarks achieved early on [S11]. Roche also potentially integrates Brain Shuttle™ technology enhancing blood-brain barrier penetration.

Bristol Myers Squibb advances BMS-986446 (formerly PRX005), an antibody candidate targeting tau pathology central to Alzheimer's disease progression; as well as PRX019 addressing other neurodegenerative targets under separate licensing deals that provide development funding plus potential milestones [S12,N1].

Novo Nordisk acquired rights related to Prothena’s ATTR amyloidosis portfolio following asset sales including coramitug (formerly PRX004), infusing upfront capital while retaining milestone participation [S12].

These collaborations not only provide non-dilutive capital inflows cushioning the high R&D expense profile but also enable risk-sharing during costly late-stage development phases frequently requiring tens or hundreds of millions per program. Moreover, partnerships afford access to commercial infrastructure accelerating eventual market entry while allowing Prothena to concentrate scientific focus on early discovery.

Financial Snapshot: Capital Structure, Cash Position, and Operating Losses

Prothena ended fiscal year 2025 with cash and cash equivalents totaling approximately $307.5 million against current liabilities near $40.8 million, translating into a very solid current ratio around 7.7—indicating substantial short-term liquidity coverage capacity amidst ongoing losses [F1,S5].

Despite this strong liquidity buffer, operating cash flow deficits highlight significant spending pressure; negative CFOs have increased annually reaching $163.6 million in 2025 from roughly $150 million one year prior. This figure reflects rising investments across multiple R&D fronts including clinical trial costs, manufacturing oversight outsourced predominantly to third parties as the company lacks internal production facilities [S7,S25].

Importantly, Prothena carries negligible debt level per most recent filings alike peer biotech firms foregoing leverage given elevated clinical risk profiles [S4,S18]. Financial strategy centers on extending runway principally via equity issuance programs including At-The-Market offerings complemented by milestone receipts from collaborators.

Future Growth Drivers and Development Milestones to Monitor

Several upcoming catalysts are poised to influence Prothena's trajectory:

Clinical data readouts from prasinezumab Phase II/III trials sponsored by Roche targeting early Parkinson’s biomarkers will be critical—positive outcomes could unlock further milestone payments alongside commercial opportunities [N1,N3].

Progression of BMS-986446 into pivotal Alzheimer’s studies may validate intracellular tau targeting approaches serving as a proof-of-concept for CYTOPE® applications.

Expansion of ATTR amyloidosis portfolio via Novo Nordisk collaborations coupled with potential label extensions or new indications represents medium-term upside.

Given biotechnology’s intrinsic binary outcomes tied tightly to regulatory approvals and trial successes, each milestone warrants close scrutiny relative to timing uncertainties inherent in CNS disorder development cycles.

Absent explicit management guidance on financial or timeline projections beyond standard disclosure of sufficient cash for next twelve months usage horizon ([S4]), stakeholders should monitor quarterly updates on program advancement alongside partnership announcements as directional indicators.

Capital Allocation Strategy and Return Metrics

Prothena devotes the bulk of its capital allocation toward research and development expenses consistent with pipeline expansion strategies—as reflected by escalating R&D spend documented in financial disclosures ([S10]). There have been no reported dividends or share repurchase initiatives acknowledging the imperative channeling of resources toward sustaining innovation efforts.

Equity capital raises through public offerings alongside collaboration payments alleviate funding pressures but embody dilution risks common among development-stage biotechs reliant on external financing vehicles ([S4],[S19]). Notably, recent restructuring actions initiated mid-2025 seek operational cost optimization suggesting management awareness about balancing growth ambitions against capital efficiency constraints ([S25]).

With reported shareholders’ equity approximately $280 million at end FY25 yet net losses exceeding $240 million annually ([F1]), calculated return on equity stands deeply negative near -87%, an expected metric given enterprise developmental phase incapable of generating profits presently.

Risks Associated with Clinical Development and Financing Needs

Prothena confronts several material risks impacting its business outlook:

Clinical trial outcomes represent binary inflection points—failures or delays could impose significant value impairments given reliance on successful advancement for regulatory approvals ([S17],[S28]).

Dependence on collaborations introduces execution risk related to milestone achievement timing as well as terms renegotiations potentially affecting future payment streams.

Persistent financial losses necessitate periodic capital raises which may not always occur on favorable terms or timely manner; scarcity of capital could curtail planned R&D activities or trigger restructuring measures ([S4],[S28]).

Biotech sector dynamics including complex regulatory landscapes specific to innovative compounds addressing challenging CNS indications heighten pathway uncertainty while intellectual property protections require constant vigilance ([S17]).

Collectively these factors underscore the precarious nature of long-duration biotech development cycles emphasizing rigorous project selection alongside prudent financial management.

This report synthesizes publicly available information without issuing investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments