Plus Therapeutics Faces Intensifying Losses and Liquidity Challenges Amid Revenue Decline in 2025

Clinical-stage oncology developer and diagnostics pioneer reports significant net losses and cash burn despite modest revenues, underscoring continued reliance on external financing.

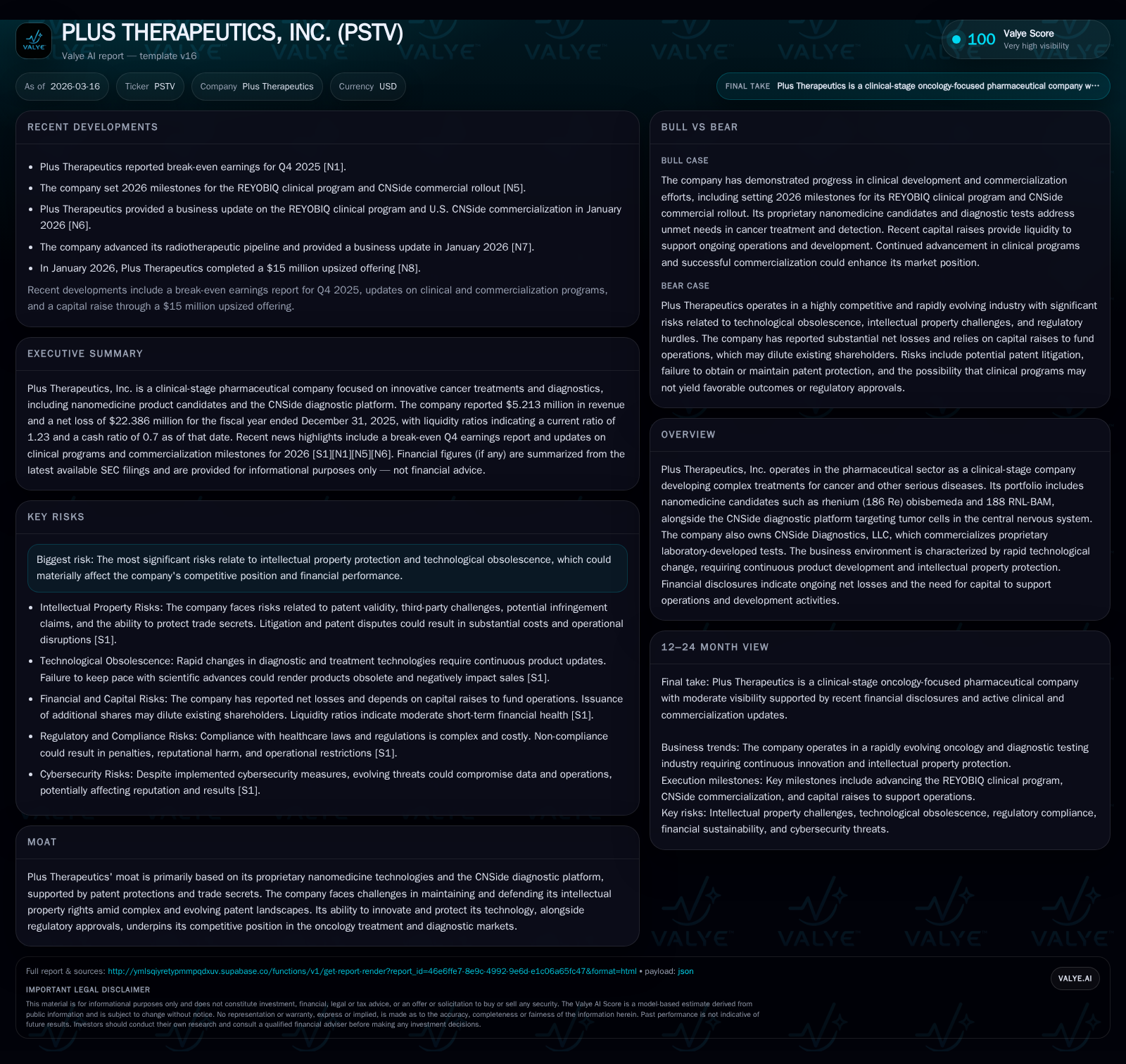

Plus Therapeutics, Inc., specializing in nanomedicine-based cancer therapies and CNS diagnostic technologies, reported a 10.5% revenue decline to $5.2 million in FY2025 alongside a 72.5% increase in net losses to $22.4 million. Operating cash outflows more than doubled year-over-year to $20.8 million, highlighting ongoing cash flow pressures. The company’s equity position improved to about $4.0 million but remains constrained relative to liabilities, with a current ratio near 1.23 as of year-end 2025. Capital allocation focused predominantly on R&D and clinical development, with limited capital expenditures recorded. Future growth depends on advancing clinical programs, regulatory progress, and diagnostic commercialization amid patent risks and regulatory complexities [F1][S1][S17][N1].

Company Overview

Plus Therapeutics, Inc. is a clinical-stage pharmaceutical company developing proprietary nanomedicine therapies for oncology alongside CNSide Diagnostics, LLC, which focuses on diagnostic testing for central nervous system tumors. The company’s pipeline includes radiotherapeutic candidates such as rhenium (186 Re) obisbemeda and 188 RNL-BAM designed to address unmet needs in cancer treatment.

Historical Financial Performance

The following table summarizes Plus Therapeutics' key financial metrics over recent years:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -22 | -21 | -15 | -10.5% | -72.5% |

| 2024 | 6 | -13 | -11 | -15 | +2.5% | |

| 2023 | -13 | -13 | -13 | +34.3% | ||

| 2022 | -20 | -13 | -20 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 374000 | -21 | -560.2 |

| 2024 | 374000 | -11 | 145.0 |

| 2023 | 126000 | 987.8 | |

| 2022 | -314.6 |

Source: SEC companyfacts cache [F1].

Revenues decreased modestly year-over-year while net losses expanded significantly in FY2025 due to increased operating expenses outpacing declining top-line results [F1]. Operating cash flow deterioration reflects substantial investments required to advance clinical programs.

Revenue Drivers and Growth Challenges

Plus Therapeutics generates revenues primarily from CNSide diagnostic testing services and milestone or licensing income associated with its nanomedicine drug candidates. The revenue contraction observed in FY2025 may be attributed to lower diagnostic test volumes or timing of milestone payments.

Future growth depends on:

- Successful progression of Phase II/III clinical trials for rhenium-based therapeutics.

- Regulatory approvals facilitating commercialization.

- Expansion of CNSide diagnostic test adoption across neuro-oncology centers.

- Strategic collaborations that may enhance revenue streams.

However, the company faces challenges including competitive pressures in radiopharmaceuticals and molecular diagnostics sectors; intellectual property litigation risks; evolving healthcare regulations; and reimbursement uncertainties [S1][S5][S7][S10].

Outlook and Key Milestones

While explicit forward guidance has not been publicly disclosed [N1], critical upcoming milestones include:

- Clinical data readouts from ongoing studies evaluating efficacy and safety of lead candidates.

- Regulatory submissions and approvals for therapeutic products.

- Growth metrics related to CNSide diagnostic test commercialization.

- Intellectual property developments including patent grants or potential litigation outcomes affecting exclusivity [S7][S10].

These milestones will be pivotal for demonstrating the commercial viability of Plus Therapeutics’ product offerings.

Capital Structure and Liquidity Position

As of December 31, 2025:

- Cash and equivalents totaled approximately $4.3 million against current liabilities of about $12.3 million resulting in a current ratio near 1.23 [F1].

- Stockholders’ equity improved to roughly $4.0 million following previous periods of negative equity driven by accumulated deficits [F1].

- Capital expenditures were limited to $67,000 reflecting focus on research and development rather than manufacturing expansion [F1].

The company has historically relied on equity issuances and convertible debt financings to fund operations amid persistent operating losses and negative cash flow from operations [S17][S19]. Maintaining access to capital markets remains critical given ongoing cash burn.

Share repurchases have been minimal but present ($374K), indicating cautious capital allocation amid liquidity constraints [F1].

Operational Efficiency and Return Metrics

Return on equity is substantially negative at approximately -560%, reflecting significant net losses relative to the small equity base typical of early-stage biopharma companies prior to commercialization [F1].

Operating leverage has deteriorated slightly with operating losses widening marginally year-over-year despite reduced revenue levels.

Strategic Moat Considerations

Plus Therapeutics’ competitive advantages stem from its proprietary nanotechnology platforms targeting cancer treatment combined with the CNSide diagnostic platform specializing in tumor detection within cerebrospinal fluid specimens. These assets are supported by patents but carry inherent risks related to intellectual property litigation and regulatory compliance complexities prevalent within the biotech sector [S7][S10].

The integration of therapeutic delivery with companion diagnostics positions Plus within emerging theranostic trends emphasizing precision medicine approaches in oncology care.

Industry Risks Specific to Plus Therapeutics

Key risk factors include:

- Intellectual property enforcement risks that could lead to costly litigation or limit market exclusivity.

- Compliance challenges navigating complex U.S. healthcare laws including fraud and abuse statutes which could result in penalties or operational restrictions [S1][S9].

- Rapid technological changes especially within diagnostics requiring continuous innovation investment.

- Dependence on external financing due to ongoing negative operating cash flows impacting liquidity stability [S17].

These risks underscore operational uncertainties even as the company advances its product pipeline.

Conclusion: Summary and Monitoring Focus

Plus Therapeutics continues to operate under challenging financial conditions characterized by growing net losses and significant cash burn despite modest revenues derived from diagnostics and early-stage therapeutics development.

Realizing value creation depends heavily on clinical advancement milestones translating into regulatory approvals coupled with successful commercialization of CNSide diagnostics while effectively managing intellectual property risks and regulatory compliance burdens.

Investors should closely monitor upcoming clinical data releases, regulatory filings/approvals, patent portfolio developments, diagnostic test volume trends, and capital raising activities as key indicators of the company’s trajectory toward sustainable operations.

This report is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments