Quad/Graphics Strengthens First-Quarter Results as Operational Challenges Persist

Quad/Graphics delivered a first-quarter earnings beat despite liquidity constraints, signaling both resilience and ongoing execution risks.

In its latest quarterly filing, Quad/Graphics reported stronger-than-expected earnings, reflecting operational improvements amid a challenging business services environment. However, the company's liquidity position remains tight, with a current ratio below 1.0, underscoring financial constraints. The printing and business services sector continues to face structural pressure from digital alternatives and evolving customer demands. Quad’s growth outlook hinges on contract renewals, cost efficiencies, and selective service expansion, while risks include market headwinds and operational leverage. Key near-term milestones involve monitoring backlog conversions and margin mix shifts.

Q1 2026 Operating Update Highlights

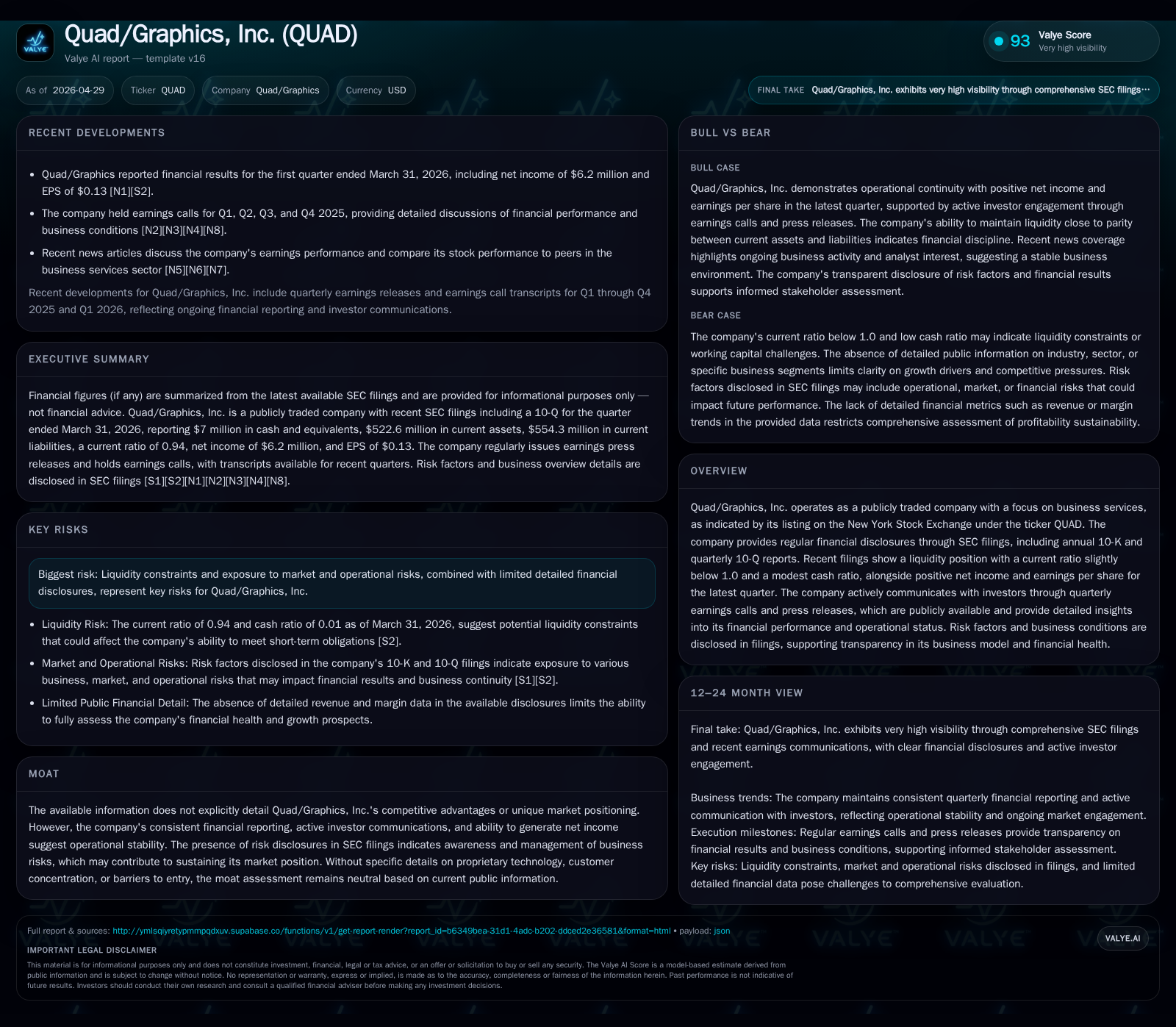

Quad/Graphics’ first quarter ended March 31, 2026 reflected encouraging operational progress with revenues and net income surpassing analyst expectations. The company announced its quarterly earnings via an April 28 press release incorporated in its April 29 10-Q filing [S2][S3]. Despite leveraging challenges in the legacy printing market segment, Quad delivered positive net income supported by strategic cost controls and pricing discipline in select service lines. However, the company’s liquidity position remains constrained; the current ratio measured at 0.94 as of quarter-end signals working capital tensions given current liabilities slightly exceed current assets [F1]. This liquidity strain is accentuated by limited cash reserves of $7 million amidst substantial near-term obligations totaling over $550 million [F1]. Management commentary underscores focus on operational efficiencies but also cautions regarding ongoing industry headwinds affecting volume demand and margin sustainability [S2]. Collectively, these results illustrate a company navigating a difficult environment but maintaining earnings resilience through adaptive measures.

Business Model and Service Offering in Context

Quad/Graphics generates revenue primarily through commercial printing and integrated business services tailored for large corporate clients. The company’s offerings span high-volume print production—as brochures, magazines, catalogs—coupled with marketing services including direct mail campaigns and digital media integrations that enhance client reach beyond print alone [S1]. This diversification aims to mitigate pure print volume erosion by capturing incremental value from cross-platform marketing workflows where switching costs rise due to customized production processes and data-driven campaign management systems [S2]. Nonetheless, core printing operations are capital-intensive with high fixed costs requiring disciplined capacity utilization management. Contractual arrangements with customers often involve negotiated pricing tiers based on volume commitments and service complexity which influence operating margins. The firm’s strength lies in its ability to blend scale manufacturing efficiencies with customized solutions responsive to client marketing objectives—a competitive necessity in an industry transitioning toward digital convergence.

Industry and Competitive Environment Assessment

The commercial printing sector faces structural challenges as digital communication channels progressively substitute traditional print media. This shift erodes volumes across catalogues, magazines, and transactional printing—historically pillars of Quad’s business model [S1][S24]. Competitors include other diversified print providers as well as digital marketing firms increasingly encroaching on value pools once dominated by print-centric platforms. Pricing power is limited as customers exercise greater bargaining leverage amid oversupply conditions and subdued end-market demand. Additionally, supply chain complexities related to paper sourcing and energy inputs inject cost volatility that impairs margin stability. Regulatory considerations center mostly on environmental compliance regarding paper waste and emissions but have not posed material disruptions recently [S24]. The pace of digital adoption varies by customer segment with some legacy sectors slower to transition—offering transient reprieves—yet overall industry dynamics underpin challenging secular pressures shaping print volume trajectories.

Identifying Growth Catalysts and Expansion Opportunities

Growth opportunities hinge on Quad’s ability to deepen integrated service offerings that marry traditional print with programmatic digital marketing solutions—a hybrid approach demanded increasingly by clients seeking unified campaigns across media formats [S2]. Management highlights an active pipeline of contract renewals reflective of sustained customer relationships but emphasizes the imperative to innovate service mix to elevate margins beyond commoditized print pricing structures [N6]. Geographic expansion remains selective with priorities accorded to regions exhibiting stable industrial demand or underpenetrated advertising spend. Incremental gains also stem from productivity enhancements via investments in automation technologies aiming to lower unit costs per output while improving turnaround times [S2]. These drivers link directly to measurable KPIs such as booking-to backlog conversion rates, renewal win percentages, and margin mix shifts favoring higher-value services.

Key Risks and Constraints to Watch

Crucial risks emanate from Quad’s tight liquidity position evidenced by a sub-1 current ratio which constrains financial flexibility amid capital intensive operations requiring ongoing maintenance capex [F1][S23]. The printing volumes remain susceptible to cyclical downturns aligned with broader advertising spend patterns in economic slowdowns or accelerated media digitization trends eroding demand more rapidly than anticipated [S23]. Rising input costs—particularly paper prices and energy—pose margin compression risks unless offset by price increases or operational efficiencies. Customer concentration risk exists where loss or non-renewal of marquee contracts could materially impact revenue profiles given the long sales cycle typical in this industry segment. Lastly, technological disruption through superior digital platforms threatens market share unless Quad successfully evolves its offering portfolio aligned with changing consumer communications behavior.

Near-Term Milestones and Market Signals to Monitor

Key upcoming events shaping sentiment around Quad’s trajectory include the scheduled Q2 2026 earnings release which will provide updates on revenue momentum post-Q1 gains along with updated guidance [S2][N2]. Contract renewal announcements remain significant markers given their direct influence on forward backlog visibility critical for revenue stability. Additionally, macroeconomic indicators tied to print sector demand—such as advertising spending trends reported quarterly—and assessments of digital migration speeds will serve as leading signals for strategic recalibration needs [N3]. Monitoring cost control effectiveness alongside margin improvements especially within high-growth digital integration service lines will illuminate execution credibility moving forward.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $7mm | |

| 2026-03-31 | ||

| Current assets | $523mm | |

| 2026-03-31 | ||

| Current liabilities | $554mm | |

| 2026-03-31 | ||

| Current ratio | 0.94x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | $7,000,000 |

| Current Assets | $522,600,000 |

| Current Liabilities | $554,300,000 |

| Current Ratio | 0.94 |

This snapshot confirms a lean liquidity cushion relative to substantial short-term payables highlighting importance of prudent working capital management as Quad presses operational adjustments under industry headwinds.

The foregoing analysis bases conclusions strictly on recent SEC filings combined with publicly accessible disclosures without speculative projections or investment recommendations. Quad/Graphics exhibits operational adaptability evidenced by quarterly earnings outperformance yet navigates ongoing structural challenges within commercial printing necessitating vigilance around financial resources management and demand evolution.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments