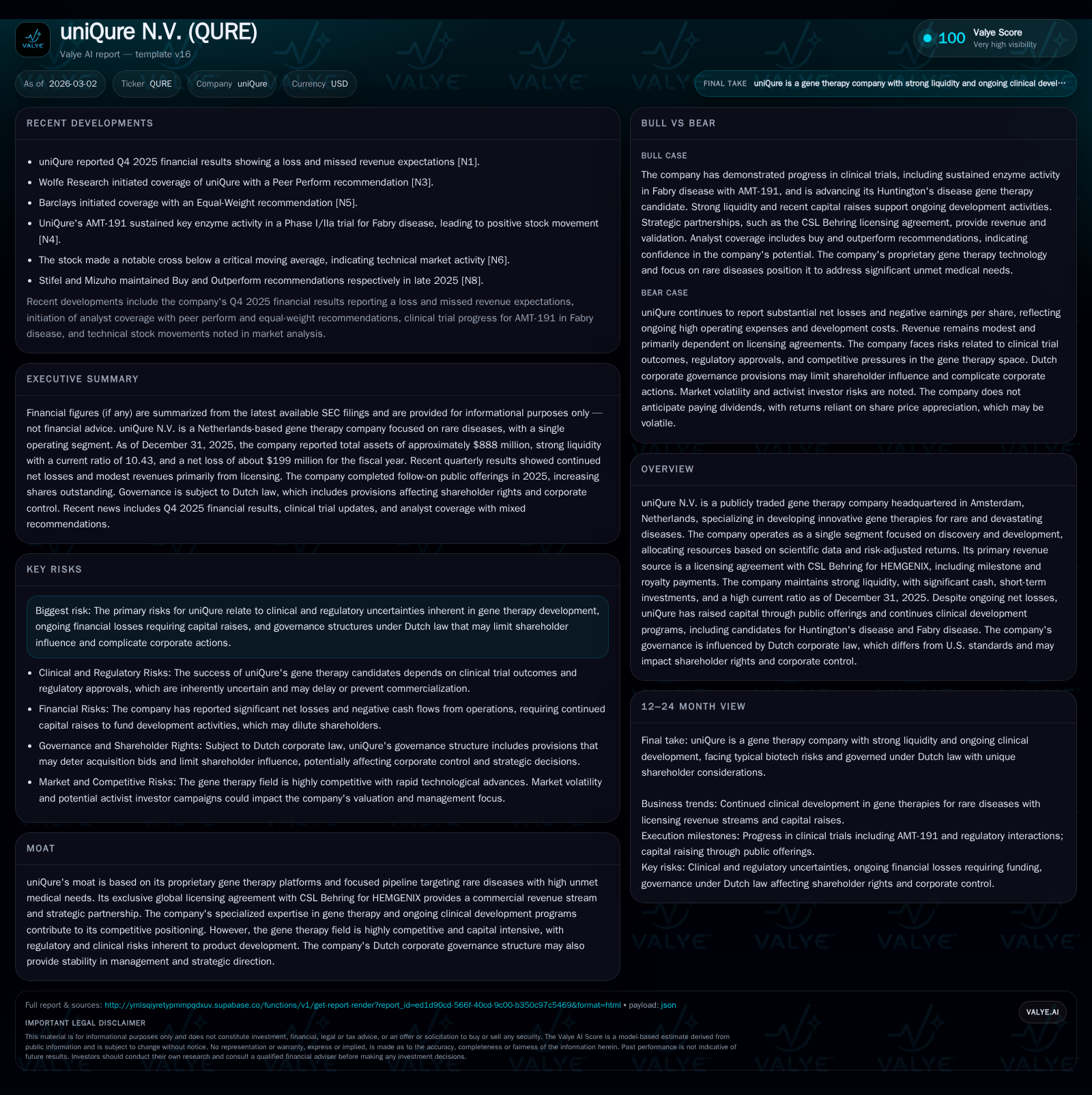

uniQure N.V.'s Financial Struggles Amid Regulatory Challenges and Pipeline Development

uniQure faces ongoing financial pressure with substantial operating losses and negative cash flow, balancing capital-intensive gene therapy development against regulatory hurdles and milestone-driven revenues.

uniQure N.V. reported sustained operating losses and negative operating cash flow in 2025, reflecting high R&D investment in its gene therapy pipeline. The company’s primary revenue derives from licensing agreements with CSL Behring for HEMGENIX, supported by a significant royalty financing arrangement. Regulatory setbacks, notably the FDA’s rejection of AMT-130 Phase I/II data, have delayed clinical progress and affected near-term prospects. UniQure maintains solid liquidity and a strong current ratio, but long-term growth depends on successful clinical advancement, milestone achievements, and prudent capital allocation within a governance framework shaped by Dutch corporate law.

Historical Financial Performance

uniQure N.V. has exhibited persistent financial losses driven by heavy investment in gene therapy research and development targeting rare diseases. For the fiscal year ending December 31, 2025, the company reported an operating loss of approximately $185.3 million, closely aligned with the prior year's loss of $184.3 million and significantly less than the $282.9 million loss in 2023 [F1]. Net income was negative $199.0 million in 2025.

Revenue declined markedly by 47.8% year-over-year to about $16.1 million in 2025 from $27.1 million in 2024 as uniQure completed its transition from contract manufacturing towards milestone-based license revenue primarily from CSL Behring's HEMGENIX product [F1][S5]. Operating cash flow remained negative at roughly $178 million but improved slightly compared with the previous year’s outflow of $182.7 million [F1]. Capital expenditures were modest at $439 thousand in 2025 compared to multi-million-dollar investments earlier in the decade.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | -178 | -185 | 0 |

| 2024 | -183 | -184 | 3 |

| 2023 | -146 | -283 | 7 |

| 2022 | -145 | -143 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -178 |

| 2024 | -186 |

| 2023 | -153 |

| 2022 | -163 |

Source: SEC companyfacts cache [F1].

Source: SEC filings and company disclosures [F1][S5]

Business Model and Revenue Drivers

uniQure's principal revenue source stems from its licensing agreement with CSL Behring granting exclusive global rights to HEMGENIX (etranacogene dezaparvovec-drlb). This includes upfront payments recognized upon contract closing, sales royalties based on net sales performance, and milestone payments contingent upon regulatory approvals or commercial milestones achieved by CSL Behring [S12].

The company ceased direct manufacturing services for HEMGENIX by mid-2024, shifting commercial risk downstream while monetizing future royalty streams through a May 2023 Royalty Financing Agreement that provided an upfront payment of $375 million against future low-tier royalties capped at approximately $693.8 million through June 2032 or up to roughly $850 million if milestones are unmet through December 2038 [S8][S12]. This structure enhances near-term liquidity but limits upside potential.

Current royalty revenue remains modest as HEMGENIX market adoption develops gradually; this explains part of the recent revenue decline relative to prior manufacturing income [N1][S12].

Pipeline Progress and Regulatory Challenges

UniQure's development pipeline includes gene therapies targeting Huntington’s disease (AMT-130) and Fabry disease (AMT-191), among others [S1][N5]. These programs underpin future growth prospects through potential milestone payments and eventual commercialization royalties or direct sales.

However, regulatory setbacks have emerged: On March 2, 2026, uniQure announced that the FDA rejected its Phase I/II data submission for AMT-130 due to concerns over study design or data quality issues, causing a sharp stock price drop exceeding 40% immediately after disclosure [N3][N1]. This delays planned pivotal trials necessary for Biologics License Application submissions anticipated before mid-2027.

Conversely, positive interim results from early-phase trials of AMT-191 demonstrated sustained enzyme activity supporting potential efficacy in Fabry disease treatment; however, timelines remain uncertain given inherent complexities in gene therapy development [N5].

Capital Structure and Liquidity

As of December 31, 2025, uniQure held cash and cash equivalents near $80 million alongside substantial short-term investments supporting total current assets above $655 million against current liabilities around $63 million — yielding a strong current ratio exceeding 10:1 indicative of robust liquidity management [F1][S26][S20].

Debt obligations primarily consist of venture loans totaling approximately $50 million under amended facilities with interest-only periods extending through at least late-2028 or later contingent on product approval milestones such as BLA filings for AMT-130 prior to June 15, 2027 [S10][S11][S16]. These loans include covenants requiring minimum cash balances tied inversely to outstanding principal based on market capitalization thresholds.

Further financial commitments include contingent milestone payments related to the acquisition of uniQure France SAS totaling up to EUR160 million (approximately $188 million), dependent on successful pipeline progress predominantly across U.S./EU regulatory jurisdictions expected over coming years [S25][S27]. Some obligations may be settled via equity issuances mitigating immediate cash outflows but dilutive effects are considerations.

Recent equity raises have bolstered capital resources with net proceeds exceeding $380 million from follow-on public offerings during the past year alongside proceeds from issuance of pre-funded warrants totaling over $23 million supporting runway amidst continuing operational spending [S21][S20].

Governance and Shareholder Dynamics

UniQure operates under Dutch corporate law as a naamloze vennootschap which entails unique governance features compared to U.S.-based counterparts including protections that may limit shareholder activism especially during periods of valuation volatility [S17][S29]. Insiders — including directors and major shareholders — collectively own approximately 47% of outstanding shares providing them significant control over strategic decisions such as board elections or major transactions which may not align fully with minority shareholder interests.

This ownership concentration can provide stability during operational challenges but may reduce external pressures for change if management performance is questioned.

Outlook: Key Milestones and Risks

Near-to-medium term outlook remains subject to several critical factors:

- Resumption timing for pivotal AMT-130 trials following FDA feedback,

- Achievement probability and timing of developmental milestones especially for AMT-260 acquired via uniQure France,

- Maintaining capital adequacy without excessive dilution or onerous debt terms,

- Market uptake pace for HEMGENIX impacting royalty revenue growth,

- Navigating Dutch legal framework implications on shareholder engagement dynamics.

Gene therapy development inherently involves prolonged investment cycles with significant technical and regulatory risks; uniQure exemplifies these dynamics given its extended history since inception through predecessor entities in the late ’90s.

Conclusion

UniQure remains positioned within a challenging yet promising segment focused on gene therapies addressing rare diseases leveraging proprietary platforms commercialized via CSL Behring’s HEMGENIX franchise generating critical non-dilutive funding streams. Persistent net losses near $200 million annually alongside negative operating cash flows underscore reliance on external financing bolstered recently through royalty monetizations and equity offerings.

Regulatory setbacks such as FDA rejection related to AMT-130 highlight material risks inherent throughout gene therapy innovation cycles despite encouraging early-stage clinical signals elsewhere within its pipeline.

Effective management balancing capital deployment against pursuing key regulatory milestones while maintaining ample liquidity within Dutch statutory governance will be essential in shaping uniQure’s path toward sustainable value creation.

Disclaimer: This report is based solely on publicly available information as of March 2, 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments