Reading International's Liquidity Pressures Challenge Growth in Cinema and Real Estate Segments

Recent quarterly disclosures highlight Reading International's ongoing liquidity constraints amidst its dual-focus business model.

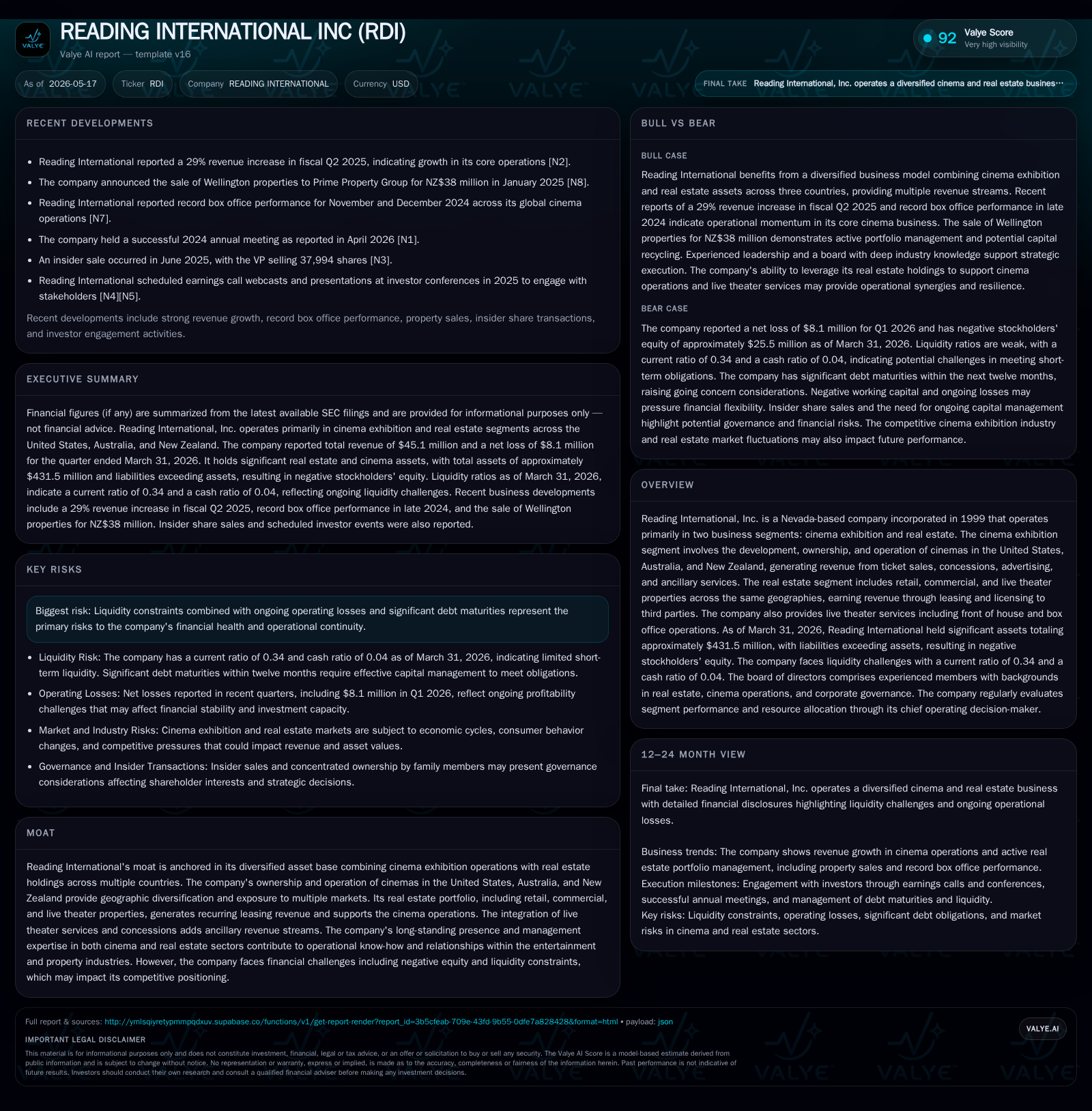

Reading International operates cinema exhibition and real estate businesses across the US, Australia, and New Zealand. The latest quarterly SEC filings disclose continuing liquidity challenges marked by a current ratio of 0.34 and net debt nearing $180 million, despite diversified revenue streams from cinema ticketing, concessions, and leasing. While the company maintained goodwill without impairment, significant debt maturities pose short-term risks. Growth potential hinges on successful asset monetizations and stable cinema market demand amid evolving consumer behaviors.

Recent Operating Update: Q1 2026 Highlights

Reading International's Q1 2026 filing dated May 15 details stable depreciation expenses on operating properties at $3.2 million (down marginally from $3.3 million in the prior year quarter) signaling consistent maintenance capex [S2]. The company reports active Construction-in-Progress (CIP) investments within operating properties reflecting ongoing upgrades or expansions to both cinema locations and real estate holdings. These capital commitments indicate a continued focus on asset improvement despite financial pressures.

However, liquidity metrics expose severe constraints: the current ratio stands at a low 0.34 with current assets of $44.8 million against liabilities exceeding $130.9 million as of March 31, 2026 [F1]. Cash reserves are limited to approximately $5.5 million while total debt measured about $184.6 million leaving net debt near $179 million — a leverage level that presents refinancing challenges given negative working capital [F1][S2]. These conditions underscore pressing near-term cash flow management considerations.

In an associated May 15 event filing (8-K), the company affirmed no goodwill impairments following quantitative tests at December 31, 2025 which assessed fair values using discounted cash flows incorporating updated market assumptions [S3][S8]. This outcome suggests that despite hardship signals, management still believes the intrinsic value of intangible assets remains intact.

Business Model: Dual Segments Focused on Entertainment Venues and Real Estate

Reading International operates fundamentally through two intertwined segments:

Cinema Exhibition: Ownership and operation of movie theaters across the United States, Australia, and New Zealand generate revenues from multiple streams including admissions ticket sales, concessions (food & beverages), advertising within theaters, and supplementary services such as premium/video-on-demand offerings [S1]. Geographic diversity allows exposure to different market dynamics but also requires adeptness in regional consumer preferences.

Real Estate: Complementary to cinemas are real estate assets comprising retail outlets, commercial spaces available for lease, and live theater venues mainly concentrated in the same geographies [S1]. Leasing income provides recurring cash flow less susceptible to box office cyclicality than cinema operations. The real estate segment also encompasses front-of-house and box office service provisions which integrate operationally with entertainment offerings.

Revenue generation mechanics depend on attracting moviegoers who pay for tickets and concessions—a combination influenced by film release cycles, competition from streaming platforms, and consumer discretionary trends. Meanwhile leasing contracts likely involve medium-to-long term agreements providing steady income streams buffered against entertainment sector volatility.

Industry Structure and Competitive Position

The global cinema exhibition industry is transitioning post-pandemic with fluctuating attendance patterns impacted by digital streaming alternatives. Reading International benefits from diversified portfolios spanning three countries reducing geographic concentration risk but still faces intense competition from multiplex chains with scale advantages.

Furthermore, integration with real estate holdings offers strategic synergies through control over prime venue sites enhancing customer experience cohesion between films showings and retail/service amenities distribution. However, this hybrid model requires balancing operational complexities across distinct industries—cinema exhibition is highly sensitive to content success cycles while real estate demands tenant retention management.

Reading’s competitive moat hinges on ownership of unique assets consolidated under singular management particularly Village East Property in NYC secured through acquisition maneuvers detailed in recent filings [S1]. Additionally, regulatory factors affecting property leases or entertainment venues – especially amid urban planning shifts or pandemic-related restrictions – remain potential disruptors.

Competition from digital streaming platforms challenges the core cinema admission model potentially limiting pricing power long term unless experiential differentiation improves sufficiently.

Furthermore, geographic exposure brings currency fluctuation risks impacting reported earnings alongside macroeconomic sensitivities influencing discretionary spending patterns across three countries involved.

What to Watch Next

Investors should monitor several key developments to gauge Reading’s trajectory:

- Progress on debt refinancing efforts or real estate asset sales that would alleviate immediate liquidity pressures.

- Quarterly updates on cinema attendance volumes and concessions sales commenting on recovery sustainability amid evolving consumer preferences.

- Lease renewal rates and occupancy metrics within the real estate portfolio providing insights into income stability.

- Updates on capital expenditures particularly around construction-in-progress projects that could unlock future revenue streams.

- Any signs of goodwill impairment recognition in subsequent periods which could indicate deteriorating asset values.

- Shifts in operating income margins pointing toward operational efficiencies or cost pressures adaptation.

Financial Snapshot Summary (As of March 31, 2026) [F1]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $6mm | |

| 2026-03-31 | ||

| Total debt | $185mm | |

| 2026-03-31 | ||

| Net debt | $179mm | |

| 2026-03-31 | ||

| Current assets | $45mm | |

| 2026-03-31 | ||

| Current liabilities | $131mm | |

| 2026-03-31 | ||

| Current ratio | 0.34x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD millions) | Period End |

|---|---|---|

| Cash & Equivalents | 5.5 | |

| 2026-03-31 | ||

| Total Debt | 184.6 | |

| 2026-03-31 | ||

| Net Debt | 179.0 | |

| 2026-03-31 | ||

| Current Assets | 44.8 | |

| 2026-03-31 | ||

| Current Liabilities | 130.9 | |

| 2026-03-31 | ||

| Current Ratio | 0.34 | |

| 2026-03-31 |

This data underscores balance sheet pressure points accentuated by limited near-term liquidity buffers relative to obligations.

This analysis is based solely on disclosures up to May 17, 2026. No investment recommendations are provided.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments