Riot Platforms Inc’s Transformation: Analyzing Financials and AI Infra Ambitions

Riot Platforms balances robust Bitcoin mining revenue growth against mounting losses as it advances into AI and high-performance computing infrastructure.

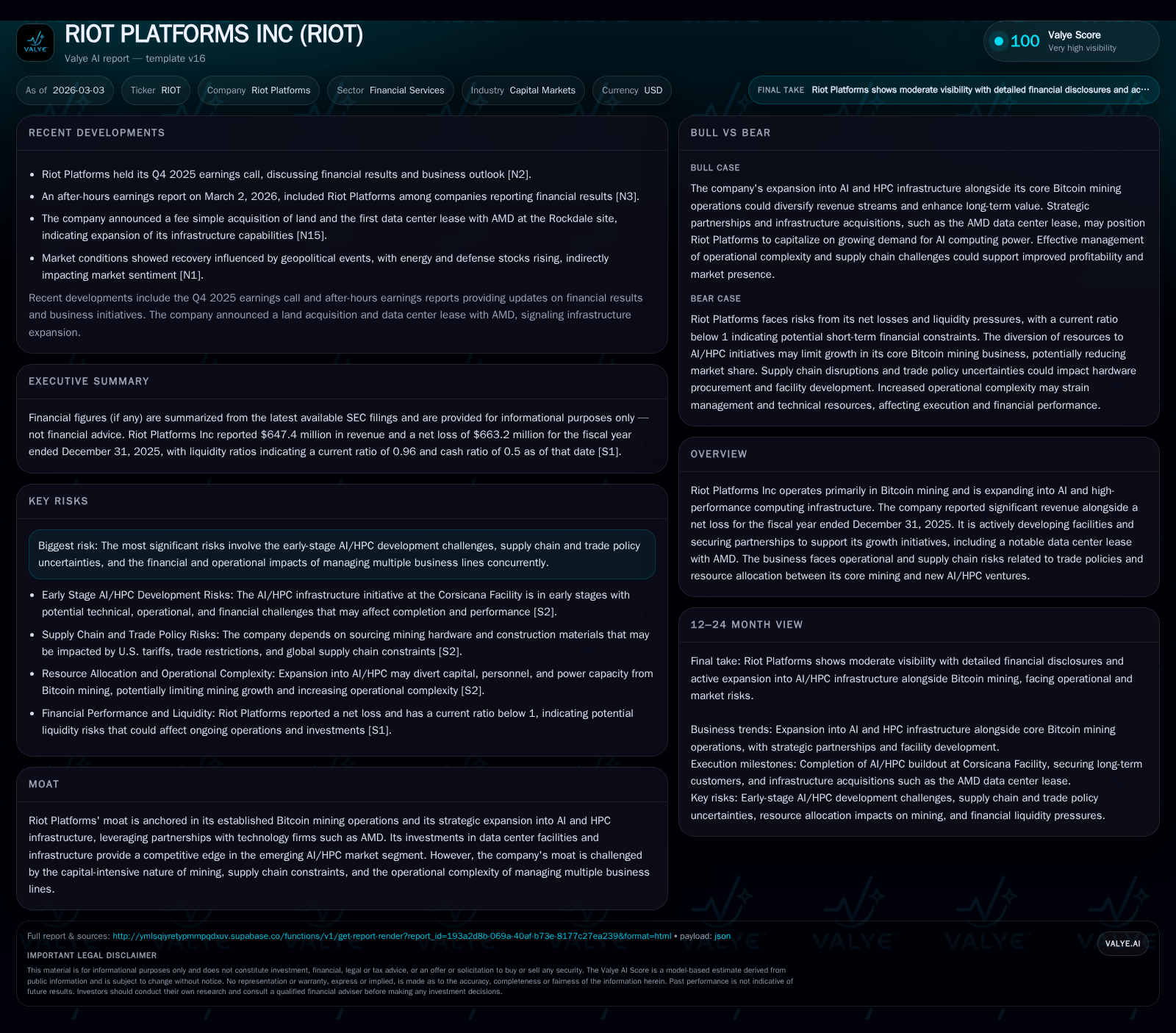

Riot Platforms delivered a substantial 72% revenue increase in fiscal 2025 driven by Bitcoin mining capacity expansion. However, this top-line surge was accompanied by a steep operating loss of $622 million, largely attributable to early-stage AI/HPC investments and operational complexities. The company is leveraging a significant $311 million partnership with AMD to develop AI infrastructure at its Corsicana Facility while managing supply chain and trade policy risks. Capital allocation remains aggressive with negative free cash flow reflecting heavy reinvestment, signaling a critical phase in Riot's dual-focus strategy between mining and AI ventures.

Historic Revenue Momentum Fueled by Bitcoin Mining

Riot Platforms Inc has demonstrated remarkable top-line momentum through rapid expansion of its Bitcoin mining operations. In fiscal year 2025, the company reported revenue of approximately $647 million, representing a robust 71.9% increase over the prior year’s $377 million figure [F1]. This acceleration stems from increased deployment of mining hardware capacity and operational scale gains that capitalized on prevailing network difficulty trends and bitcoin price dynamics. The historical sequence reflects steady revenue growth from $259 million in FY2022 rising through consecutive years despite challenging crypto market conditions.

This growth trajectory underscores Riot’s core competitive position in the highly capital-intensive and technologically specialized Bitcoin mining sector. Legacy investments in efficient ASIC miner deployment have underpinned better throughput and yield improvements, expanding available hashing power — a key operational metric directly correlating with revenue potential.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 647 | -663 | -573 | -622 | +71.9% | -706.2% |

| 2024 | 377 | 109 | -255 | 154 | +34.2% | +321.1% |

| 2023 | 281 | -49 | 33 | -63 | +8.3% | +90.3% |

| 2022 | 259 | -510 | 1 | -513 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 4 | -774 | -23.2 |

| 2024 | 12 | -495 | 3.5 |

| 2023 | 14 | -161 | -2.6 |

| 2022 | 10 | -148 |

Source: SEC companyfacts cache [F1].

Escalating Financial Losses Amid Expansion Efforts

While top-line growth has been commendable, Riot's profitability has deteriorated sharply amid its strategic expansion. Operating income swung from a positive $154 million in FY2024 to a significant operating loss of $622 million in FY2025 — a staggering decline of over 500% year-over-year [F1]. Correspondingly, net income also turned negative at -$663 million for FY2025 compared to a positive $109 million net in the prior year.

This widening loss profile primarily reflects elevated operating expenses tied to initial investments in new business lines alongside increased complexity from managing multiple high-capital operations simultaneously. Specifically, initial development activities related to Riot's AI and HPC infrastructure initiative have introduced substantial one-time buildout costs, as well as ongoing R&D and administrative expenses [S3], [N1]. Furthermore, supply chain inefficiencies and contractual complexities have likely contributed incremental burdens.

The plunge in operating cash flow to -$573 million (from -$255 million) further emphasizes the strain on core operations and indicates that expanded activities are absorbing cash faster than generated revenues can sustain at this stage [F1]. This negative free cash flow dynamic signals the need for continued external financing or disciplined capital allocation management.

| Fiscal Year | Operating Income (USD mln) | % OpInc YoY | Net Income (USD mln) | % Net YoY |

|---|---|---|---|---|

| 2025 | -622 | -505.1 | -663 | -706.2 |

| 2024 | 154 | 109 | ||

| 2023 | -63 | -49 | ||

| 2022 | -513 | -510 |

AI and HPC Infrastructure: The Next Frontier for Riot

Diversification beyond Bitcoin mining represents Riot’s strategic thrust into high-performance computing (HPC) aligned with artificial intelligence workloads, anchored by its Corsicana Facility development. Riot secured a landmark deal leasing out a significant portion of this facility to AMD valued at approximately $311 million — signifying material commercialization progress within its nascent AI business line [N9], [S2].

This transition requires intricate balancing acts: power availability must be allocated between energy-heavy mining rigs versus emerging HPC server deployments dedicated to machine learning tasks requiring low-latency compute clusters. Sector specialists note such resource partitioning involves sophisticated electricity distribution systems and real-time load management capabilities to optimize throughput across heterogeneous workloads.

Despite promising commercial arrangements, the buildout remains early stage with technical risks around scaling data center infrastructure while ensuring uptime reliability consistent with premium HPC standards — prerequisites for attracting additional long-term customers beyond AMD [S2]. Moreover, success hinges on ability to recruit third-party AI ecosystem partners capable of generating sustained revenue streams as the facility matures.

Operational Challenges and Supply Chain Risks

Riot faces persistent supply chain headwinds affecting both Bitcoin mining hardware procurement and specialized AI infrastructure materials amid fluctuating U.S. trade policies. Recent tariffs on imported components may inflate capital expenditure requirements or delay critical equipment deliveries essential for ramping operations at scale [S2], [S4].

Competition for limited supplies of construction materials, data center-grade electrical gear, and cutting-edge mining chips induce operational complexity—exacerbated by simultaneous demand from expanding AI/HPC needs alongside entrenched mining hardware upgrades.

This resource strain introduces execution risks including buildout slowdowns, cost overruns, or suboptimal equipment sourcing choices impacting overall profitability trajectories. Trade policy uncertainty compounds forecasting difficulty especially considering potential re-negotiations impacting import tariffs or export controls on high-tech components relevant to Riot's dual business lines [N11].

Capital Allocation: Investments, Cash Flows, and Shareholder Returns

Evaluating capital deployment reveals chronic investment intensity aligned with Riot's dual-growth ambition but constraining near-term financial returns. The company maintained high capital expenditures totaling roughly $201 million in FY2025; albeit down modestly from prior year levels reflecting possible timing variations or project phasing shifts [F1].

Alongside capex pressure, operating cash outflows deepened substantially pushing free cash flow toward an estimated negative $774 million in FY2025 when subtracting capex from operating cash flows — underscoring a heavy reinvestment cycle absent meaningful internal cash generation currently.

Liquidity metrics indicate near-term tightness with the current ratio dipping below parity at approximately 0.96 despite closing cash balances above $230 million [F1], [S7]. Shareholder returns through repurchases appear limited; buybacks totaled about $4.3 million compared with notably higher activity in previous years without any dividend distributions recorded recently or forecasted.

These trends highlight capital scarcity themes common among emerging blockchain infrastructure players transitioning into adjacent high-tech fields without established profit margins yet.

| Fiscal Year | Operating Cash Flow (USD mln) | % CFO YoY | Capex (USD mln) | % Capex YoY |

|---|---|---|---|---|

| 2025 | -573 | -124.6 | 201 | -16.2 |

| 2024 | -255 | 240 | ||

| 2023 | 33 | 194 | ||

| 2022 | 1 | 148 |

Key Milestones and What to Monitor Next

Looking forward, key milestones include observable progress on the Corsicana Facility’s AI/HPC buildout schedule as well as successful onboarding or contract renewals with additional commercial HPC customers beyond AMD partnerships — vital indicators that diversification efforts gain traction without compromising core mining businesses’ power utilization efficiency [N2], [S2].

Investor focus should also remain attuned to evolving U.S. trade policies affecting import tariffs on semiconductor components given their outsized influence on cost structures and deployment timelines [N11]. Equally critical will be how Riot manages operational complexity amid resource competition that might exacerbate losses or limit scaling agility.

Broader macroeconomic factors such as fluctuating energy costs or regulatory developments influencing cryptocurrency economics could further sway financial outcomes given Riot’s exposure primarily via electricity-intensive backend operations.

In sum, Riot Platforms is navigating an inflection point balancing strong historical growth underpinned by Bitcoin mining fundamentals against a capital- and risk-intensive expansion into sophisticated AI infrastructure sectors that require vigilant execution management and flexible financial stewardship.

Disclaimer: This analysis is presented solely for informational purposes referencing publicly available data sources including SEC filings and company disclosures as of March 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments