Revolution Medicines Faces Scaling Challenges Despite Expanding Clinical Pipeline and Capital Reserves

The clinical-stage biotech continues to incur widening losses while progressing precision oncology assets, with profitability hinging on regulatory and commercial execution.

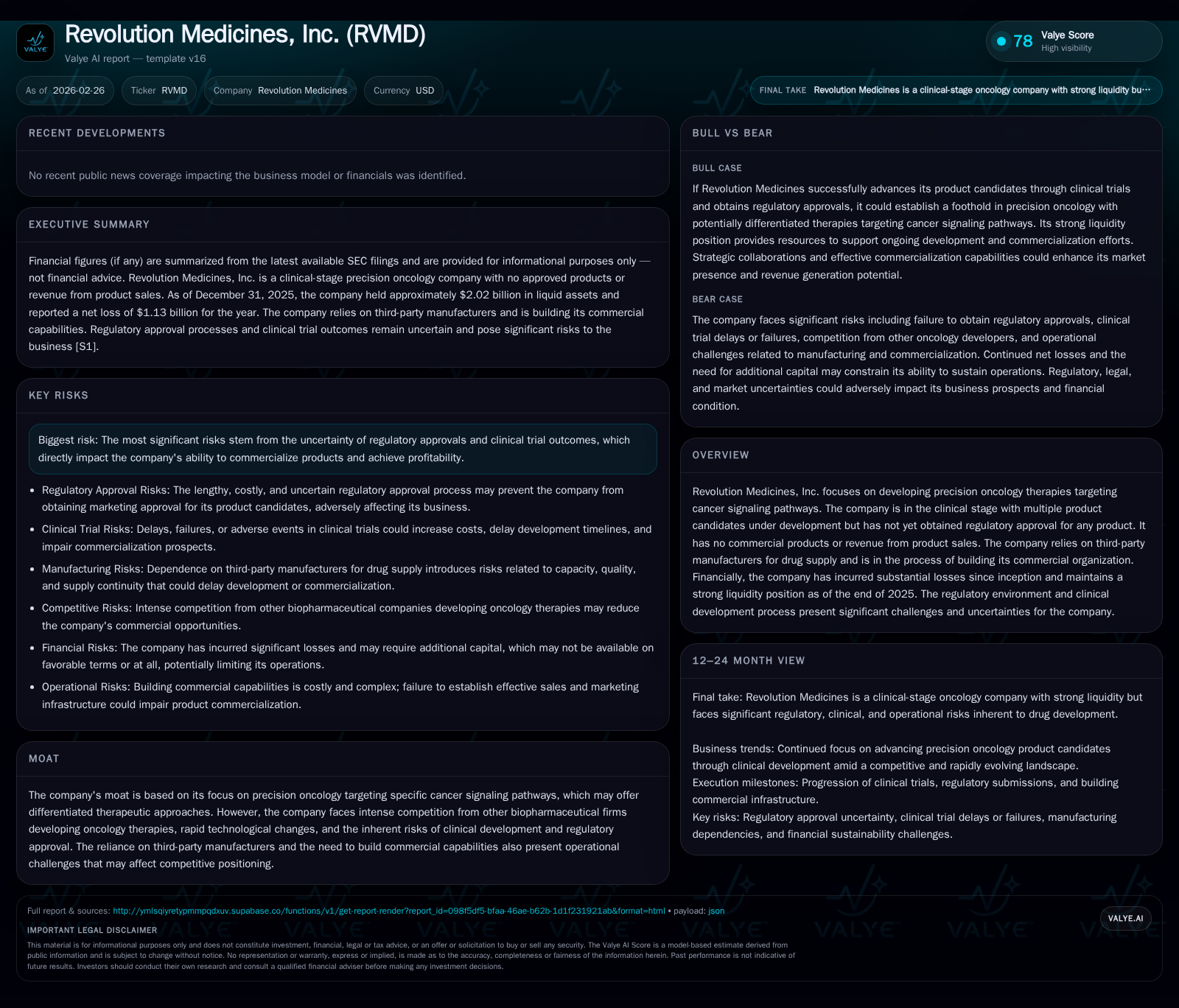

Revolution Medicines, Inc. remains a pre-revenue, clinical-stage company deeply invested in oncology drug development targeting cancer signaling pathways. Since inception, it has systematically expanded its pipeline but has yet to secure any regulatory approvals or product sales, resulting in continued net losses that more than doubled in 2025 relative to 2024. The company retains a healthy liquidity position bolstered by capital raises and strategic agreements but faces significant risks from regulatory uncertainty, competitive pressures, and operational scale-up needs. Future growth relies on successful clinical milestones and the eventual market introduction of its candidates, while investors should monitor upcoming trial readouts and commercial preparedness.

Company Overview

Revolution Medicines, Inc. is a clinical-stage precision oncology company focused on developing targeted therapies that modulate cancer signaling pathways. Founded in October 2014, it has yet to bring any product candidates to regulatory approval or commercial sale. Its operations concentrate on securing intellectual property rights, conducting discovery and translational research, and advancing multiple product candidates through clinical development phases. The company relies heavily on third-party manufacturers for drug supply and is building commercial infrastructure as it approaches potential market entry.

Historical Financial Performance

Revolution Medicines has operated at a loss since inception, consistent with expectations for a clinical-stage biotech without approved products or revenues. Net losses accelerated sharply from fiscal years 2023 to 2025 due to increased investments across R&D pipelines and corporate functions. Operating income declined from -$258 million in 2022 to -$1.18 billion by end-2025, representing a roughly 71.5% deterioration year-over-year between 2024 and 2025 [F1]. Net losses similarly increased by about 88.5% to exceed $1.13 billion in FY 2025.

Operating cash flow reflected the burn rate with CFO worsening from -$224 million (FY22) to nearly -$898 million (FY25), alongside modestly rising capital expenditures reaching about $16 million last year for manufacturing partnerships and commercial readiness [F1]. Free cash flow remained deeply negative near -$914 million in FY25 after deducting capex.

Despite ongoing losses, the company maintained a robust balance sheet with $384 million in cash & equivalents by year-end 2025 and a strong current ratio above 7x indicating liquidity strength to fund near-term operations [F1]. Equity was $1.63 billion at year-end 2025 reflecting accumulated deficits but substantial shareholder investment.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1131 | -898 | -1182 | 16 | -88.5% |

| 2024 | -600 | -557 | -690 | 10 | -37.5% |

| 2023 | -436 | -351 | -487 | 8 | -75.5% |

| 2022 | -249 | -224 | -258 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -914 | -69.3 |

| 2024 | -568 | -26.5 |

| 2023 | -358 | -23.9 |

| 2022 | -235 | -36.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not reported as no sales have occurred.

Development Pipeline and Growth Prospects

While detailed public data on individual candidates' recent progress is limited beyond earnings transcripts [N1], disclosures emphasize multiple programs targeting critical oncogenic drivers within cancer signaling networks — an area of significant scientific focus due to pathway complexity and resistance mechanisms.

The company's competitive edge lies in innovative molecule design potentially enabling selective pathway inhibition with improved efficacy and tolerability compared to competitors pursuing Ras/MAPK axis or related targets [S1][N1]. However, this field is highly competitive with rapid technological advances requiring sustained innovation.

Future growth prospects depend materially on:

- Successful completion of ongoing clinical trials meeting safety and efficacy endpoints;

- Obtaining regulatory approvals across jurisdictions;

- Building internal commercial capabilities or forming partnerships/licensing arrangements;

- Navigating reimbursement landscapes complicated by healthcare reforms such as the Inflation Reduction Act affecting specialty drug pricing .

Failure in any of these areas could significantly limit growth potential.

Financial Outlook and Milestones

No explicit forward guidance was provided recently beyond general management commentary emphasizing near-term focus on advancing late-stage studies and preparing for possible product launches contingent upon approvals [N1][S1].

Key upcoming catalysts include pivotal trial data readouts which will influence valuation inflection points as well as announcements of new collaborations that might mitigate commercialization risks or augment capital resources.

Returns and Capital Allocation

As a pre-commercial entity incurring heavy development expenses exceeding $1 billion annually [F1], Revolution Medicines currently does not generate returns nor distribute dividends or conduct share repurchases.

Approximate return on equity based on recent net income relative to equity levels is deeply negative near -69%, reflecting losses absorbed against shareholders’ equity base [F1]. This underscores the high-risk profile typical of biotechs prior to revenue generation.

Capital allocation priorities focus heavily on funding R&D expansion (clinical trial costs/materials) plus modest investments into infrastructure needed for eventual commercialization [S17].

Risk Considerations

The company faces typical biotechnology sector risks intensified by its developmental phase:

- Regulatory hurdles including unpredictable FDA/EMA approval timelines and risk of failed trials or additional data requests delaying marketing authorization [N1];

- Competitive dynamics with multiple well-capitalized peers developing alternative targeted oncology agents creating pressure on differentiation;

- Operational challenges arising from dependence on third-party manufacturers for drug supply; building a commercial organization requires significant capital given limited prior experience;

- Intellectual property risks including patent disputes that could incur costly litigation diverting resources ;

- Financing risk despite current cash buffers (~$384M), future capital needs remain substantial given burn rates; uncertain equity/debt markets could restrict funding access impacting program continuity or timelines [S17][F1];

- Pricing & reimbursement reforms driven by recent U.S legislative measures targeting specialty drug cost containment potentially impacting net pricing power post-launch enforcement beginning after 2026 timelines ;

- Legal contingencies related to mergers historically linked through EQRx acquisition with accrued reserves of $5 million reflecting continuing liabilities though not material relative to overall financials currently [S1].

Summary Outlook

Revolution Medicines exemplifies a clinical-stage biotech blending cutting-edge science with high capital consumption prior to market entry milestones. It maintains substantive liquidity sufficient for current heavy R&D commitments but will require additional financing unless dramatic trial successes accelerate partner deals or early commercialization revenues materialize.

Investors should closely monitor pipeline progress updates especially pivotal efficacy data expected within forthcoming quarters alongside management commentary regarding commercial build-out pace plus external factors such as competitor breakthroughs or health policy shifts that may materially reshape opportunity windows.

Disclaimer: This report provides analysis based solely on publicly available information as of February 26, 2026. It contains no investment advice nor recommendations regarding the securities discussed.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments