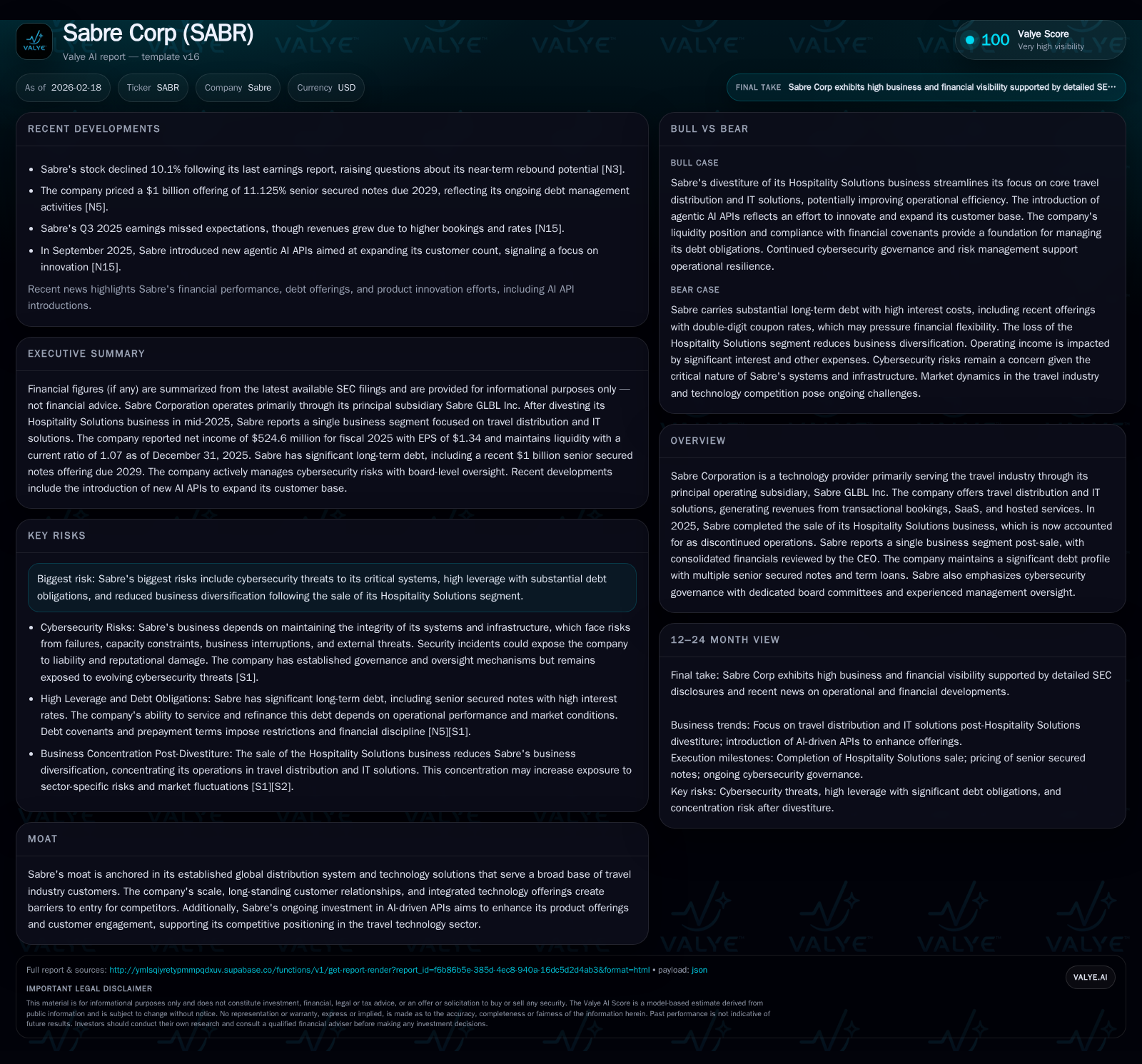

Sabre Corp’s Recovery Through SaaS Growth and Debt Management

Sabre Corp reversed multi-year losses in 2025, bolstered by SaaS expansion and significant debt refinancing.

Sabre Corporation experienced a notable financial turnaround in FY2025 after years of operating losses, driven by strategic divestment from its Hospitality Solutions segment and a renewed focus on scalable travel distribution solutions with growing SaaS revenue. Despite strong operating and net income improvements, the company continues to carry substantial leverage with senior secured notes maturing primarily between 2027 and 2030. Sabre also emphasizes robust cybersecurity governance to safeguard its mission-critical platforms. Key areas to watch include ongoing cash flow recovery, further SaaS adoption fueled by AI-driven product innovation, and the management of its complex capital structure.

From Losses to Profitability: Sabre’s Recent Financial Trajectory

Sabre Corporation's financial performance showed a marked turnaround in FY2025. The company posted operating income of $295 million, a 3.3% increase year-over-year from $286 million in FY2024, following substantial losses in prior years including -$261 million in FY2022 [F1]. Revenue increased approximately 4.8% YoY to about $1.02 billion in FY2025 compared to previous years [F1]. Net income swung dramatically from a loss of $279 million in FY2024 to a profit of $525 million in FY2025, reflecting a recovery exceeding 280% [F1].

Despite this earnings improvement, operating cash flows have not yet fully recovered. For example, Q1 2025 operating cash flow was negative approximately $81 million, evidencing working capital pressures despite improved profitability [F1]. Capital expenditures remained steady at around $83 million annually, consistent with prior years [F1], resulting in negative free cash flow estimated near -$163 million for FY2025 (operating cash flow minus capex) [F1].

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 525 | 295 | 83 | +288.2% |

| 2024 | -279 | 286 | 84 | +47.2% |

| 2023 | -528 | 47 | 87 | -21.2% |

| 2022 | -435 | -261 | 69 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, CFO, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -50.6 |

| 2024 | 17.4 |

| 2023 | 38.3 |

| 2022 | 49.9 |

Source: SEC companyfacts cache [F1].

*Latest full year revenue approximated based on latest filings; 'NA' where data is insufficient or unavailable [F1].

Historical Growth Drivers and Focus on Travel Distribution Technology

Post-2025 divestiture of its Hospitality Solutions segment [S1], Sabre concentrates exclusively on travel distribution technology centered around its Global Distribution System (GDS). This platform supports airline ticketing, hotel bookings via third-party integrations, and ancillary travel services worldwide [F1][S1]. The shift emphasizes recurring revenues from software-as-a-service (SaaS) and hosted IT solutions that provide more predictable margins versus transaction-based fees alone.

While detailed booking volumes or SaaS revenue breakdowns are not explicitly disclosed in available filings or news sources [F1][S1], the strategic focus on SaaS underpins margin expansion and customer retention efforts.

Impact of Divesting Hospitality Solutions

The divestiture completed in 2025 simplifies Sabre's business model by focusing on core travel technology offerings [N3][S1]. While reducing diversification within the broader travel ecosystem, it allows targeted investment into platform modernization and AI capabilities [N3]. This streamlining is reflected in consolidated financial reporting post-divestiture.

AI-driven APIs: Innovation for Competitive Differentiation

Sabre invests in AI-powered APIs aimed at enhancing user experience through personalized content delivery, dynamic pricing signals, and streamlined booking workflows [S1]. These innovations seek to increase platform stickiness among agency customers by embedding advanced analytics at multiple interaction points.

Such developments require continuous R&D investment to maintain competitive parity amid evolving travel technology landscapes supported by robust cybersecurity governance frameworks detailed below.

Debt Profile and Capital Structure After Refinancings

Sabre’s total debt remains elevated above $4 billion primarily consisting of senior secured term loans and high-yield notes maturing between late-2027 and mid-2030 [S4][S5][S13][F1]. Notable debt facilities include:

- Amended Term Loan B facilities extending maturity to November 15, 2029, bearing interest at Term SOFR plus approximately 600 basis points [S10]

- Senior secured notes with coupon rates ranging from roughly 7.32% to 11.125%, some repaid or refinanced during early-to-mid FY2025 [S13]

- A securitization facility supporting accounts receivable financing at SOFR plus about 400 basis points [S22]

As of mid-2025, the weighted average interest rate across short-term borrowings was about 8.17%, reflecting leverage-sensitive credit conditions [S17]. Financial covenants remain met but restrict dividends or large-scale buybacks [S10].

Cash Flow Trends and Capital Allocation Amid High Leverage

Operating cash flow remains constrained despite profitability gains; Q1 FY2025 recorded negative operating cash flow (~-$81 million), while capex stayed around $83 million annually [F1], resulting in negative free cash flow near -$163 million for FY2025. This dynamic poses challenges for deleveraging.

No dividends have been paid since before FY2020, nor have there been share repurchases since FY2021 or earlier periods [F1], consistent with management’s focus on debt reduction and system upgrades over shareholder returns given capital constraints.

Cybersecurity Governance as Operational Pillar

Sabre maintains rigorous cybersecurity oversight through dedicated board committees including the Audit Committee which reviews cyber risk profiles quarterly with input from the CIO and CISO—who holds multiple advanced degrees plus certifications such as CISSP—supported by a cross-functional Cybersecurity Governance Committee led by the CISO [S1].

This comprehensive governance is critical given Sabre's role underpinning global travel infrastructure vulnerable to cyber threats that could cause operational disruption or reputational damage.

Outlook: Growth Prospects and Risks Ahead

Growth prospects depend on continued recovery of travel industry transactional volumes complemented by expanded adoption of AI-enabled SaaS products enhancing customer engagement [N3][S1]. Success deploying predictive analytics APIs offers potential for incremental recurring revenue upside.

However, high leverage constrains aggressive expansion initiatives requiring upfront investment before returns materialize. Additionally, cybersecurity threats remain an ongoing risk necessitating sustained protective investments.

Key Milestones Beyond 2026 to Monitor

With limited explicit financial guidance post-hospitality divestiture [N3][S3], key factors include:

- Monitoring quarterly operating cash flow relative to EBITDA benchmarks indicating liquidity improvement;

- Managing refinancing risks as term loan maturities approach late-decade windows;

- Tracking adoption rates for AI-driven API products reflected indirectly via SaaS revenue growth;

- Observing covenant compliance status and any changes in board-level cybersecurity oversight. These will collectively influence whether Sabre sustains its recovered position as a leading travel technology provider while managing financial risk prudently.

Disclaimer: This analysis is based solely on publicly available information including SEC filings and news releases cited herein. It does not constitute investment advice or recommendations. Readers should conduct their own due diligence when evaluating Sabre Corp or any other securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments