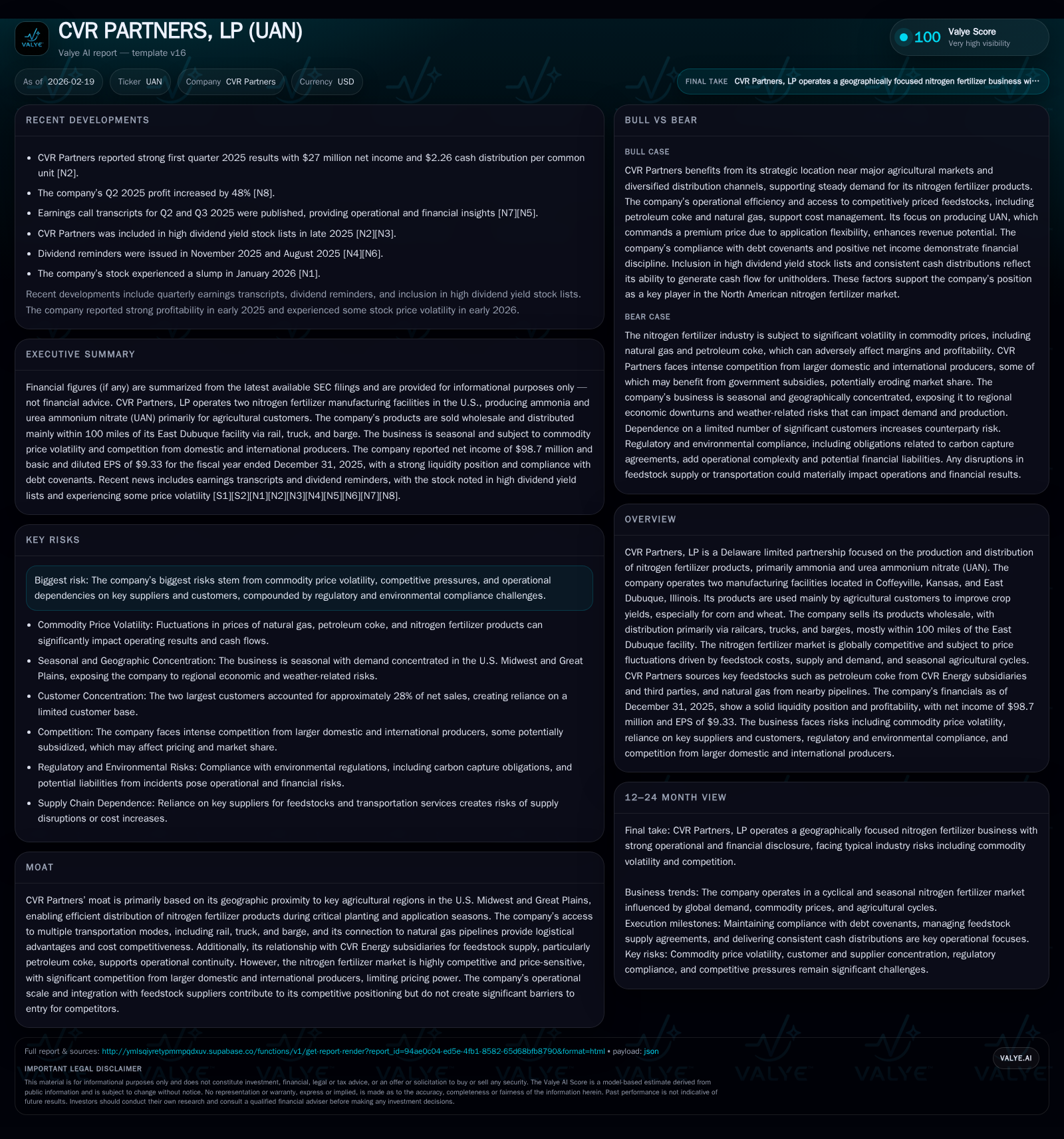

CVR Partners’ Profit Resilience Amid Fertilizer Market Volatility

CVR Partners leverages its Midwest location and integrated feedstock supply to sustain earnings despite volatile nitrogen fertilizer markets.

CVR Partners, LP operates two nitrogen fertilizer manufacturing facilities strategically located in the U.S. Midwest, enabling proximity to key agricultural regions that seasonally drive demand for ammonia and UAN products. Following a trough in 2024, the company posted a notable 42.4% rebound in operating income in 2025, supported by efficient feedstock sourcing primarily from CVR Energy subsidiaries and multimodal distribution logistics. While pricing and volume remain vulnerable to commodity cycles and customer concentration, CVR’s operational integration and geographic advantages underpin its profit resilience amid competitive and regulatory headwinds.

Operational Footprint and Market Context

CVR Partners operates two nitrogen fertilizer manufacturing facilities critically positioned in the Midwest — Coffeyville, Kansas and East Dubuque, Illinois [S4][S5][S17]. This geographic location situates the Partnership near prime U.S. agricultural zones—the Corn Belt and Great Plains—where demand for nitrogen fertilizers such as ammonia and UAN peaks during seasonal planting cycles [S12]. The East Dubuque facility benefits from pipeline connectivity to the Northern Natural Gas interstate system within one mile of site—a strategic advantage for sourcing competitively priced natural gas used as feedstock hydrogen for ammonia production [S5]. Likewise, Coffeyville uniquely uses petroleum coke sourced largely (~36%) from CVR Energy subsidiaries along with third-party suppliers to convert into hydrogen via gasification for nitrogen fertilizer production—the only North American facility to employ this process [S5].

Distribution leverage is realized through multimodal logistics: railcars primarily via Union Pacific or Burlington Northern Santa Fe railroads deliver mostly on destination point basis with freight arranged by CVR Partners [S5]. Truck shipments are handled more commonly on shipping point basis with customers arranging freight. With direct barge access on the Mississippi River near East Dubuque, products reach agricultural customers efficiently within a ~100 mile radius—a critical factor for timely fertilizer application in planting seasons [S5]. These shipping point vs. destination point bases reflect important sector nuances impacting freight cost responsibilities.

Financial Performance Trends: From Peak to Adaptive Growth

CVR Partners' financial history showcases marked cyclicality reflecting commodity price swings inherent in nitrogen fertilizer markets. Operating income peaked robustly at $319.9 million in FY2022 but declined sharply through FY2023 ($201.4 million) to a trough of roughly $90.3 million in FY2024—reflecting depressed price realizations and challenging feedstock cost dynamics [F1]. In 2025, operating income rebounded strongly by 42.4%, reaching $128.7 million [F1]. Net income showed a parallel surge (+62%) recovering to $98.7 million after reaching $60.9 million in 2024 [F1].

Operating cash flow (CFO) maintained relative stability despite profitability swings: about $150 million was generated both years ending 2024–25 versus higher levels above $240 million seen earlier [F1]. Capital expenditures (capex) rose notably (+37%) in 2025 to $50.8 million amid ongoing turnaround maintenance and strategic asset refurbishment [F1]. The resulting approximate free cash flow (CFO minus capex) stood near $98.8 million for 2025—the operational leverage of returns amid elevated reinvestment costs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 99 | 150 | 129 | 51 | +62.0% |

| 2024 | 61 | 151 | 90 | 37 | -64.7% |

| 2023 | 172 | 244 | 201 | 24 | -39.9% |

| 2022 | 287 | 301 | 320 | 45 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 99 | |

| 2024 | 0 | 113 |

| 2023 | 0 | 219 |

| 2022 | 12 | 257 |

Source: SEC companyfacts cache [F1]. +37%

Note: Revenue figures are not available from provided tags; dividends data is not disclosed; buybacks ceased post-2022.

Drivers Behind the Operating Income Recovery

The recovery was principally driven by enhanced operational execution leveraging favorable feedstock arrangements and responsive product mix optimization [S1][S2][F1]. CVR Partners continues to capitalize on its unique pet coke integration at Coffeyville; transitioning about one third of input supplies from CVR Energy subsidiaries ensures cost stability relative to volatile natural gas markets experienced broadly across the sector [S5]. At East Dubuque, pipeline natural gas affords competitive hydrogen production costs enabling flexible conversion between ammonia and UAN output tuned to market demand shifts [S17].

Seasonal farm activity focusing on corn and wheat crops allows CVR Partners to capture concentrated selling windows during spring and early summer when retailers aggressively purchase ammonium fertilizers [S12]. Fixed-price contracts under one year reduce exposure but also limit upside participation during rapid price surges; nevertheless, disciplined scheduling mitigates inventory carrying costs amidst volatile price swings.

Outlook Amid Cyclical Pressures

Looking ahead, CVR Partners faces typical cyclical constraints tied closely to corn belt planting schedules, global grain prices influencing fertilizer demand, and competitive pricing pressures amplified by subsidized international producers [N1][S13][S14]. The company does not provide explicit earnings guidance; limited visibility amplifies investor focus on external indicators.

Growth may be capped by reliance on short-term contract pricing that limits upside capture during commodity rallies [S4]. Demand sensitivity is heightened due to regulatory scrutiny over potential price caps or import tariffs disrupting trade flows [S15][S6]. Concentration risk remains material as top two customers represent approximately 28% of net sales—volume fluctuations tied to weather or liquidity constraints could materially affect results given short contract durations typical of the industry [S6].

Feedstock Sourcing & Supply Chain Advantages

Feedstock integration remains a principal moat element for CVR Partners [S5]. Approximately 36% of pet coke feedstock is sourced from CVR Energy-owned Coffeyville Refinery subsidiaries providing supply security atypical within the sector where third-party availability is often more variable.

The East Dubuque Facility’s proximity (within one mile) to Northern Natural Gas pipeline enables firm access to competitively priced natural gas with multiple receipt points reducing curtailment risk [S5]. Combined with direct access to barge docks on the Mississippi River adjacent to East Dubuque gives multimodal logistics flexibility: rail serves long-distance customers mostly delivered on destination point basis while trucks cater local deliveries commonly sold shipping point basis where customers arrange freight—as standard industry practice.

These logistical advantages reduce freight cost volatility exposures while enhancing service reliability pivotal during highly time-sensitive planting seasons.

Capital Structure, Cash Flow Analysis & Returns

At year-end 2025, CVR Partners held cash & equivalents of approximately $69 million against current liabilities near $97 million producing a current ratio around a healthy 2.21 indicating solid short-term liquidity [F1].

Long-term debt includes secured notes due June 2028 totaling about $550 million plus finance lease obligations around $20 million net of issuance costs reported at September quarter-end prior year [S7][S10][S16], with all covenants reportedly complied with affording operational financial flexibility.

Despite strong cash generation (~$150 million CFO annually), capital spending rose markedly (+37%) reflecting scheduled maintenance turnarounds typical every three years plus incremental facility enhancements aimed at preserving high utilization rates [F1][S11]. No repurchases of common units occurred through FY2024–25 following modest buybacks earlier emphasizing prioritization of capital reinvestment over distributions or share buybacks recently.

Dividends paid are not disclosed explicitly suggesting distributions remain variable contingent on available cash post capex/reserve requirements consistent with partnership structure risks around variable quarterly payouts noted by management disclosures [S8].

Competitive Positioning Within U.S Nitrogen Market

The U.S nitrogen market is intensely price-sensitive dominated by large players such as CF Industries Holdings Inc., Nutrien Ltd., Koch Fertilizer Company LLC alongside smaller competitors like LSB Industries emphasizing scale's role alongside geographic advantages especially near core demand zones like the Corn Belt / Great Plains [S15][S4].

Foreign competition remains formidable particularly where subsidized exporters can undercut domestic producer pricing creating margin pressure especially during oversupply cycles or mild growing seasons depressing volumes.

Within this environment product differentiation is limited thus delivered price competitiveness combined with logistic efficiency underpin customer retention — factors where CVR’s proximity advantage combined with its integrated feedstock supply chain confer meaningful albeit not insurmountable barriers limiting commoditization erosion.

Risks: Market Volatility, Regulation & Customer Concentration

Risks arise from volatile input commodity prices notably natural gas impacting production costs alongside fluctuating global agricultural commodity markets dictating fertilizer purchasing behavior risking volume unpredictability season-to-season [S8][S9][S29].

Environmental regulatory compliance imposes ongoing capital costs plus risks of citations or cleanup liabilities associated with hazardous substances spillage or emissions governed under CERCLA/EPCRA regimes adding financial uncertainty given evolving legal frameworks [S19]. Expanded government scrutiny into fertilizer pricing could introduce ceilings impacting revenue potential complicating planning further [S6][S15].

Customer concentration amplifies vulnerability should principal purchasers scale back volumes unexpectedly given absence of long-term minimum purchase contracts typical across industry increasing dependency on spot market sales fluctuations impacting earnings stability materially [S6].

Operational hazards including unplanned shutdowns or labor disruptions pose downside risks capable of compressing margins at peak seasons further amplifying earnings variability inherent in business model relying heavily on just-in-time delivery aligned tightly with farming calendars.

Key Metrics & Indicators To Monitor

Investors should track quarterly fertilizer pricing trends — particularly product netbacks (price at gate less freight costs) which directly inform margin recovery alongside evolving pet coke versus natural gas feedstock cost spreads given their material influence over unit economics [N1][S3][S13].

Seasonal shipment volumes especially during spring planting provide leading insights reflecting weather-dependent acreage decisions coupled with macro grain price movements globally impacting producer incomes driving purchases.

Capital expenditure plans versus actual spending will reveal investment intensity balances between sustaining asset integrity versus expansion/optimization initiatives relevant against tightening environmental regulations increasing compliance outlays.

Finally changes in customer buying patterns among top purchasers remain critical given concentration risks—any significant volume shifts could materially alter operating leverage outcomes requiring close market surveillance considering limited contract durations restricting long-horizon revenue visibility.

Disclaimer: This report presents an objective analysis based exclusively on publicly available filings (SEC reports) cited herein without extrapolating beyond documented evidence nor offering investment recommendations or price forecasts for CVR Partners LP (NYSE:UAN). Readers should perform their own due diligence respecting company disclosures prior to making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments