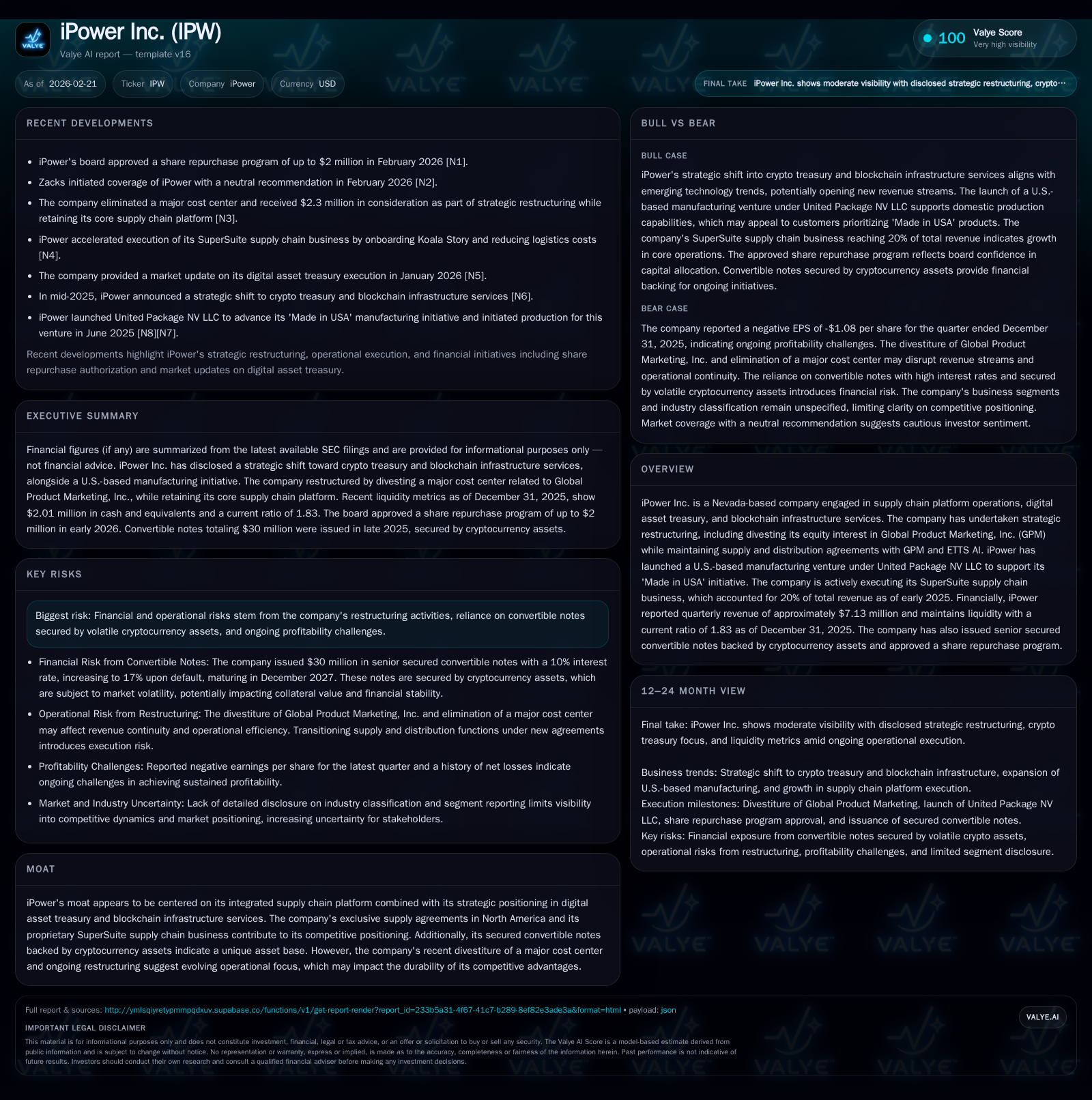

How iPower Inc. Balances SuperSuite Growth with Digital Asset Risks and Capital Constraints

iPower Inc. is evolving its supply chain platform while managing the inherent risks of cryptocurrency-backed debt and limited capital resources.

iPower Inc. has undergone significant strategic restructuring, notably divesting its equity stake in Global Product Marketing (GPM), while maintaining supply agreements that preserve its distribution role. Revenue has contracted sharply since 2024, driven by these changes and operational pressures, although the emergent SuperSuite supply chain platform now comprises about 20% of revenue and offers diversification potential. The company’s capital structure includes senior secured convertible notes backed by volatile digital assets, providing financing flexibility but adding risk exposures. A $2 million share repurchase program signals an intent to return capital despite ongoing losses and constrained cash flows. Near-term milestones hinge on successful integration of SuperSuite clients, ramp-up of U.S.-based manufacturing, and registration compliance for convertible note liquidity.

Historical Revenue Trends and Operating Income Volatility

iPower Inc.'s fiscal trajectory reveals pronounced challenges as it adjusts its business model. Annual revenues peaked at approximately $88.9 million in FY2023 before declining to $86.1 million in FY2024 and further collapsing by over 23% to $66.1 million in FY2025 [F1]. This contraction coincides with the company’s February 2026 divestiture of its equity interest in Global Product Marketing (GPM) [N1], a move that eliminated a major cost center but shifted revenue recognition dynamics.

Operating income followed a negative path exacerbated by restructuring costs and operational shifts: from a positive $2.3 million in FY2022 down to a loss of nearly $13.5 million in FY2023; improving slightly to -$963k in FY2024; then worsening dramatically (-$5.87 million) through FY2025 [F1]. These swings suggest substantial operational leverage coupled with disruption from strategic pivots.

Net income similarly deteriorated into losses post-2022 but showed signs of narrowing negative gaps by FY2024 (loss of -$1.53 million) and posted a positive net income of $219k for the six months ending Dec-31, 2024 [F1]. However, net income for FY2025 is not available from provided tags.

Operating cash flows reflect this struggle; after strong cash generation exceeding $9 million in FY2023, CFO dropped sharply by over 109% year-over-year to a negative -$579k in FY2025 [F1]. Capital expenditure remained modest at $164k for FY2025 compared to prior years indicating limited reinvestment capacity.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 66 | -1 | -6 | -23.2% | ||

| 2024 | 86 | -2 | 6 | -1 | -3.2% | +87.2% |

| 2023 | 89 | -12 | 9 | -13 | +11.9% | -888.3% |

| 2022 | 79 | 2 | -17 | 2 | +295.7% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -1 |

| 2024 | 6 |

| 2023 | 9 |

| 2022 | -17 |

Source: SEC companyfacts cache [F1].

Note: Net income data for FY2025 is not available from provided tags.

Drivers Behind iPower’s Revenue Contraction and Profitability Pressure

iPower's February 2026 restructuring dismantled the GPM equity stake while preserving commercial ties via supply agreements [N1][S7]. This action removed GPM's sales function—a significant revenue contributor—leading to accounting impacts consistent with top-line contraction.

However, iPower continues acting as exclusive supplier for all SKUs historically distributed through GPM across the United States, Canada, and Mexico under a five-year supply & distribution agreement with automatic renewals every two years unless terminated with notice [S7]. Pricing allows iPower to add up to a 15% margin over net cost plus receive cooperative marketing fees under separate agreements.

This shift reflects an intentional tradeoff: reducing complexity and overhead related to directly managing GPM’s sales operations but retaining product flow control and margin capture opportunities [N1][S7]. The structure involves credit offsets tied to promissory note payments illustrating bespoke financial engineering to preserve working capital utility.

The loss of GPM's direct sales likely distorted revenue recognition timing and magnitude but helped stabilize gross margins — a key lever given the weight of operating losses previously arising from bundled cost centers.

Unpacking the SuperSuite Platform’s Role in Diversifying Revenue Streams

iPower builds strategic growth around its SuperSuite business—an integrated supply chain platform complemented by proprietary SaaS layers aimed at logistics optimization [N6]. As of early 2025, SuperSuite contributed roughly one-fifth (20%) of overall revenues [F1][N6].

The company recently accelerated onboarding of large brand Koala Story to reduce third-party logistics expenses through automation and enhanced freight consolidation approaches [N6]. This reflects sector-native trends where embedded supply chain SaaS solutions create stickiness via operational cost savings paired with enhanced visibility.

SuperSuite's expansion mitigates dependence on legacy distribution agreements by injecting proprietary technology-enabled offerings that command higher value capture.

Its incorporation of tools for inventory tracking, purchase order automation, and logistics analytics aligns with broader industry movements toward supply chain digitization—critical given recent global disruptions affecting fulfillment throughput and cost bases.

Strategic Restructuring: Divestiture of GPM Equity Interest and Supply Agreement Impact

The divestiture included transfer of software assets via a Software Asset Transfer Agreement enabling perpetual licenses between iPower and GPM [S24]. Subsequently, under the Supply & Distribution Agreement effective February 1, 2026, iPower retained exclusive supplier status for all SKUs historically branded within GPM’s marketing channels across US, Canada, Mexico territory [N1][S7].

Pricing mechanics embed:

- A baseline cost plus allowance for up to a flat maximum margin add-on around 15%

- Cooperative marketing fees negotiated separately incentivizing joint promotional efforts

- Credit/offset application against promissory note receivables tying payment flows across agreements cohesively

Term length is five years with automatic renewals barring termination notices within defined windows ensuring medium-term commercial stability without direct sales overhead burdens for iPower [S7].

This model mirrors common supply chain practices where distributors act as fulfillment hubs charging suppliers flex-based margins plus marketing support fees under contractual safety nets limiting exposure to counterparty default or margin squeeze risks.

Digital Asset Treasury: Opportunities Amid Volatility and Capital Structure Implications

iPower has moved strategically into digital asset treasury management as part of diversifying funding sources while capitalizing on blockchain infrastructure services [N7][S25][S26]. In December 2025, it announced initial purchases approximating $2.2 million split between Bitcoin and Ethereum securing critical crypto reserves underpinning liquidity pools.

This digital asset backing supports hybrid financing instruments while exposing balance sheet composition heavily toward volatile cryptocurrencies—assets that fluctuate widely based on regulatory sentiment and market cycles typical within blockchain subsectors.

Blockchain infrastructure services complement treasury functions via offering secure crypto custody solutions augmented by proprietary platforms integrating tokenized asset management with compliance workflows enhancing ecosystem trustworthiness.

While these assets enhance leverage capacity enabling issuance of senior secured convertible notes collateralized against such holdings [S5], valuation swings present marked risk factors requiring robust risk management protocols including stress-testing collateral coverage ratios amid adverse crypto market shifts.

Convertible Notes Backed by Cryptocurrency: Financing Flexibility versus Risk Exposure

In late December 2025, iPower closed issuances totaling approximately $7 million across Series A/B senior secured convertible notes bearing fixed coupon interest rates at an annual rate of 10%, maturing December 23, 2027 [S10][S11]. An additional mandatory closing added around $2 million principal upon registration statement effectiveness [S22].

These notes are fully collateralized by cryptocurrency assets underlying the Security Agreement creating first priority liens on crypto collateral managed under multiple subsidiary guaranties limiting unsecured credit exposure [S5][S16]. The inclusion of registration rights signifies obligations surrounding public resale capabilities impacting future dilution risks especially relevant given conversion mechanisms tied to VWAP-based pricing floors ranging broadly between $2.27 floor price upward based on market trading periods prior conversion notices [S15][S22].

Interest is payable monthly commencing January 1, 2026 with escalation clauses elevating rates up to 17% under event-of-default conditions acting as deterrents against covenant breaches [S10]. This debt form offers considerable flexibility compared to traditional bank facilities yet trades off volatility exposure embedded within crypto collateral pools alongside potential shareholder dilution modulated through conversion triggers governed by trading price dynamics.

Capital Allocation Priorities: Share Repurchase Program and Cash Position Analysis

iPower’s board authorized a share repurchase program capped at $2 million announced February 10, 2026 aiming to opportunistically buy back shares either via open market or privately negotiated transactions including Rule 10b5-1 plans [N2][S4]. This move indicates confidence signals despite ongoing operating losses demonstrated over successive fiscal periods.

As of December ’25 quarter end, the company reported approximately $2 million in cash & equivalents alongside current assets near $14.7 million versus liabilities around $8 million culminating in a current ratio near a healthy ~1.83x suggesting reasonable near-term liquidity buffer [F1].

Free cash flow remains negative given operating cash outflows combined with modest capex spend (approximate free cash flow: -$743k calculated as operating cash flow minus capex), highlighting constrained internal capital generation emphasizing reliance on external financing or operational improvement for sustainable capital returns [F1].

No dividends have been declared or paid reflecting prudent reinvestment or balance sheet preservation stance during transitionary phases documented within restructuring disclosures implying cautious stewardship focusing on deleveraging risks coupled with leveraging growth initiatives conservatively rather than shareholder yield enhancement currently.

Near-Term Expectations and Milestones to Monitor

Explicit forward guidance remains undisclosed; however critical upcoming milestones include:

- Completion and effectiveness of SEC registration statements linked to Series A Convertible Notes ensuring liquidity pathways for holders thereby influencing secondary trading dynamics impacting conversion activity potential withholding dilution outcomes [S10][S22]

- Progressive onboarding velocity within SuperSuite platform especially large clients like Koala Story signifying validation points for revenue diversification beyond legacy supplier roles thus potential inflection in top line composition percentages relative total revenues [N6]

- Operational ramp-up success metrics from United Package NV LLC manufacturing venture supporting "Made In USA" initiatives anticipated to enhance domestic supply resilience potentially creating competitive differentiation amid heightened reshoring trends observed globally post-pandemic disruptions [N1]

- Ongoing management updates regarding digital asset treasury execution detailing portfolio allocations versus market valuations providing insight into collateral sufficiency against convertible note obligations detailing risk exposure adjustments under volatile market environments affecting credit cushion adequacy [N7]

This forward-looking discussion should be treated as analysis reflecting company-reported intents absent explicit quantifications or projections from filings or press releases.

Risk Factors in Light of Strategic Changes and Market Dynamics

iPower maintains a consistent risk profile year-over-year without material changes since its Annual Report Form 10-K ending June ’25 per SEC disclosures highlighting principal concerns involving operational uncertainty from restructuring moves; reliance on volatile cryptocurrency-backed debt instruments; concentration risk tied to exclusive supply contracts particularly post-GPM divestiture; persistent profitability challenges evidenced across multiple fiscal cycles including negative operating leverage effects; marketplace disruptions within blockchain infrastructure realms influenced by rapidly evolving regulations potentially impacting asset valuations securing convertible notes; potential delays or failures meeting registration deadlines for converted securities affecting liquidity conditions; among others detailed comprehensively in prior filings [S6][N1][F1].

The confluence of these elements demands continuous monitoring juxtaposing growth aspirations against inherent risks elevated via non-traditional capital structures anchored on digital assets while navigating evolving competitive landscapes within supply chain SaaS integration spheres.

Disclaimer: This report is intended solely for informational purposes based on publicly available data as cited herein; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments