Teledyne Technologies' Growth Drives Capital Allocation Amid Defense Sector Dependencies

Teledyne Technologies posted robust profitability in 2025 supported by defense contracts and innovation in nano-drone technology, while facing growth limits tied to government spending.

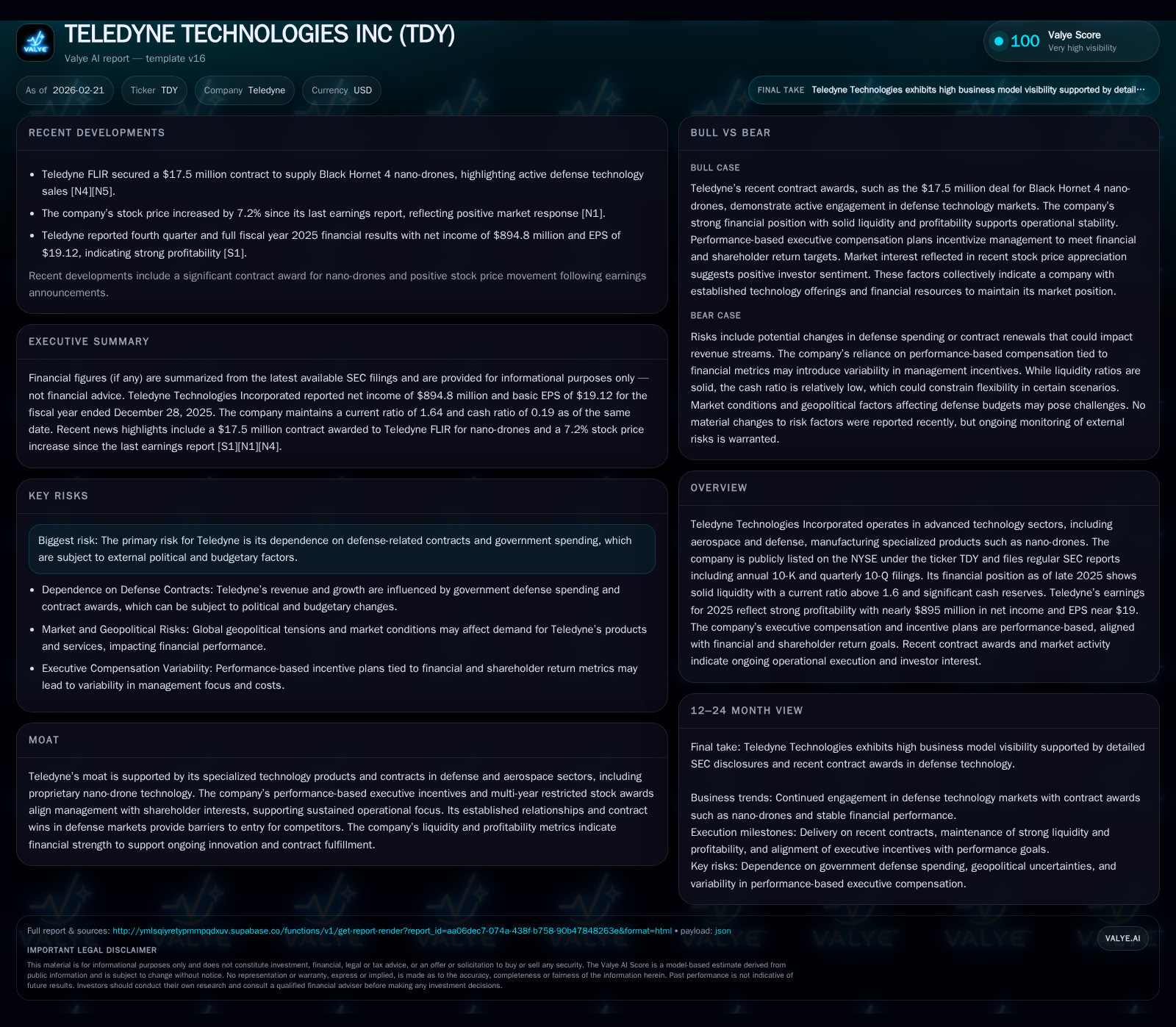

Teledyne Technologies (TDY) delivered solid financial performance in 2025 with revenues near $1 billion and net income close to $895 million. The company benefits from a strong moat rooted in its aerospace and defense technologies, including proprietary nano-drones, which underpin its backlog and ongoing contract wins. Despite steady cash flow generation and active capital allocation via share repurchases, future growth faces headwinds from the inherent cyclicality and political risk of defense budgets. Investors should monitor contract awards, government spending patterns, and execution on innovation as key growth levers.

Company Overview and Industry Position

Teledyne Technologies Incorporated operates within the advanced technology sectors focusing on aerospace and defense markets. Its product portfolio includes highly specialized instruments and systems such as nano-drones, sensors, digital imaging equipment, and engineered systems tailored for defense applications [N10][S1]. The company's moat is reinforced by proprietary technology platforms like the Black Hornet series nano-drones and enduring governmental contracts that create significant barriers to new entrants.

Historical Financial Performance

Teledyne's financial results for the full year ending December 28, 2025, reveal substantial operating leverage during top-line pressures. Revenue slightly declined by about 4.6% from the previous year to approximately $1.02 billion [F1]. Nonetheless, operating income expanded robustly by over 16% year-over-year to roughly $1.15 billion [F1], reflecting efficiency gains or favorable product mix shifts.

Net income for FY 2025 was nearly $895 million, marking a healthy increase of over 9% compared to the prior year [F1]. This profitability is noteworthy given the modest revenue contraction and suggests rigorous cost controls or higher-margin contract wins during the period.

Operating cash flow has held firm at around $1.19 billion for both FY 2024 and FY 2025 [F1], sustaining liquidity despite a marked rise in capital expenditures of over 40%, reaching approximately $117 million in FY 2025 [F1]. The elevated capex underscores investments possibly related to R&D or facility enhancements crucial for maintaining technological leadership.

Financial Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 895 | 1191 | 1150 | 117 | +9.2% |

| 2024 | 819 | 1192 | 989 | 84 | -7.5% |

| 2023 | 886 | 836 | 1034 | 115 | +12.3% |

| 2022 | 789 | 487 | 972 | 93 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 403 | 1074 | 8.5 |

| 2024 | 354 | 1108 | 8.6 |

| 2023 | 721 | 9.6 | |

| 2022 | 394 | 9.7 |

Source: SEC companyfacts cache [F1].

Note: Dividend data unavailable; Buybacks data omitted for years <2 points.

Capital Structure and Returns

Equity stood at over $10.5 billion by end-2025 [F1], implying a return on equity calculated at roughly 8.5%, consistent with mid-tier aerospace/defense peers where capital intensity and R&D investments anchor returns.

The company continues active capital deployment into share repurchases—$403 million was spent in FY 2025 [F1]. There was no dividend information available from SEC filings for this period; however, management’s incentive structures are heavily weighted toward stock-based awards promoting shareholder alignment [S8][S9].

Free cash flow approximates $1.07 billion after adjusting CFO minus capex spend—highlighting strong internal funds generation supporting both organic growth investments and capital returns.

Executive Compensation Alignment

At the leadership level, Teledyne adopts a rigorous performance-based compensation model encompassing annual bonuses linked to operating profits, revenue thresholds, capital efficiency metrics like managed working capital relative to revenue, plus individual objectives [S8][S10]. Long-term equity incentives vest contingent upon outperforming S&P benchmarks on total shareholder return across three-year periods [S8]. The CEO’s restricted stock unit grants target above base salary multiples (140%), reflecting confidence in sustained value creation incentives.

Growth Prospects and Recent Developments

Recent contract awards reinforce Teledyne's steady pipeline—most prominently an incremental award of $17.5 million related to the Black Hornet nano-drone program finalized early February 2026 [N10][N11]. This contract signifies continuing demand for compact unmanned aircraft systems with applications spanning intelligence, surveillance, reconnaissance missions within defense sectors.

Further growth could be propelled by ramping adoption of these nano-technology products alongside synergistic offerings across sensor systems deployed on military platforms or civilian aerospace programs.

However, Teledyne remains dependent on U.S. government defense budgets with inherent risk stemming from geopolitical tensions or changing political priorities influencing contract volumes [S4][S5]. Budgetary fluctuations typically impact order visibility and timing which caps visibility on midterm revenue trajectories.

Industry Context Analysis

The broader aerospace and defense sector experiences cyclical pressures connected to government funding cycles coupled with accelerating technological shifts demanding continuous R&D investments—notably in autonomous systems like drones which are becoming mission-critical assets.

Manufacturing complexity in advanced electronics segments drives margin pressures but also creates entrenched supply chain dependencies that protect key incumbents such as Teledyne against new entrants.

Key Risks

The predominant risks acknowledged include sensitivity to evolving U.S./international defense spending policies where congressional appropriations directly affect contract awarding timelines [S4][S21]. Additionally, regulatory changes or trade restrictions could constrain overseas business expansions.

Operational risks involve sustaining innovation pace particularly amid competing private-sector players developing next-generation unmanned aerial vehicles or sensor technologies that could erode market share if not matched continuously.

What To Watch Going Forward (Analysis)

- New contract announcements beyond current backlogs signaling government commitment levels.

- Changes in U.S. federal budget allocations for key agencies influencing procurement activity.

- Execution success of technology advancement efforts critical for maintaining competitive edge especially concerning miniature drone systems.

- Capital allocation patterns to gauge whether buybacks remain prioritized vs dividend initiatives or investments.

- Shareholder return outcomes tracked relative to market benchmarks that drive executive deferred compensation vesting conditions.

This analysis synthesizes publicly available SEC disclosures and news reports as of early Q1/2026 without extending beyond disclosed facts into speculative forecasts or investment recommendations.

Disclaimer: This report is intended strictly for informational purposes regarding TELEDYNE TECHNOLOGIES INC.'s financial condition and strategic position based on available documentation from SEC filings and credible news sources as cited herein; it should not be construed as investment advice or a solicitation for purchase or sale of securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments