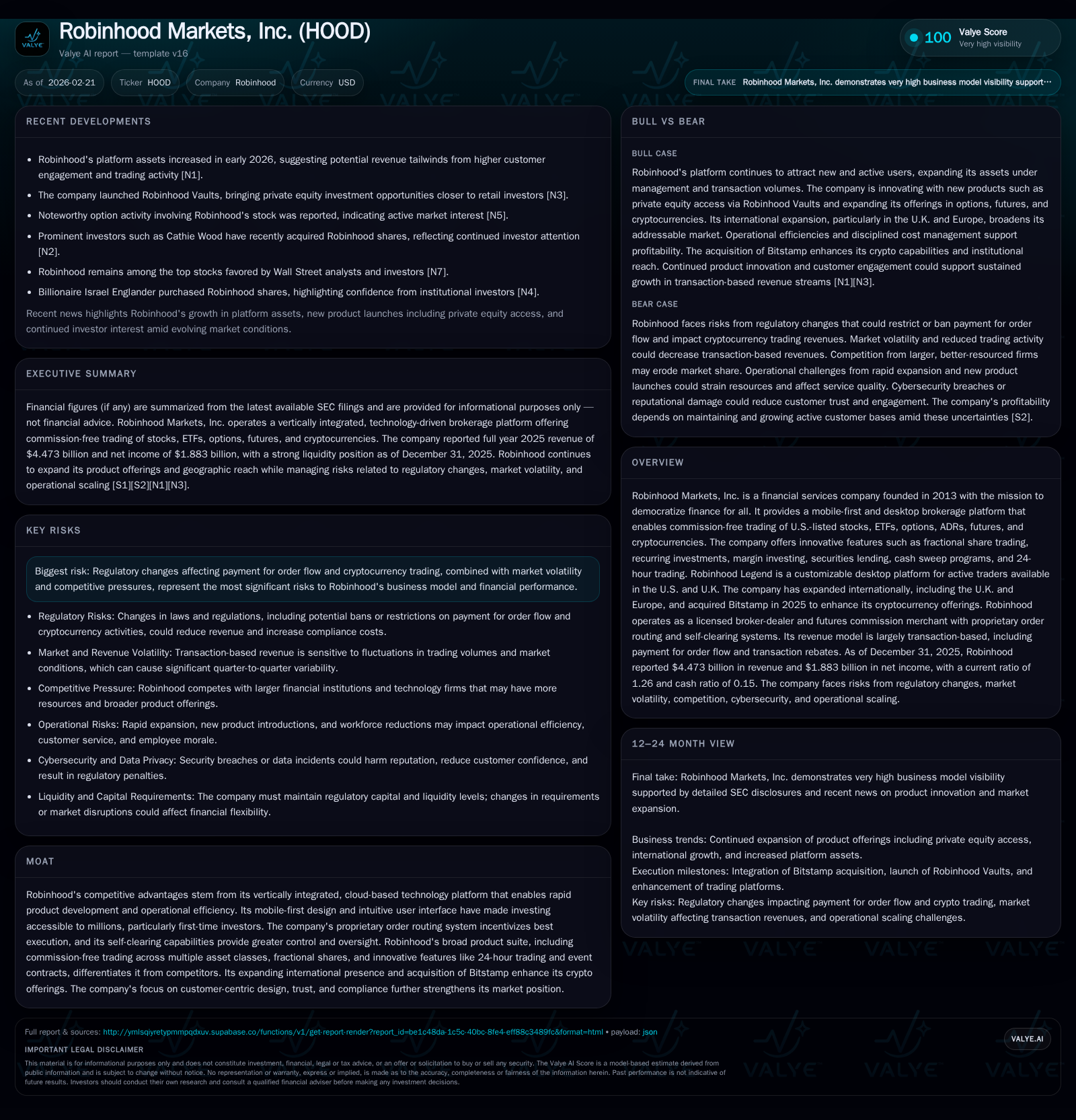

Robinhood Markets Emerges as Profit Leader with Surging Revenue and Strategic Expansion

Robinhood transitions from a disruptive startup to a profitable brokerage powerhouse driven by platform innovation and international growth.

Once known primarily for pioneering commission-free trading for amateur investors, Robinhood Markets, Inc. has successfully transformed into a highly profitable, multi-asset retail brokerage platform. By doubling revenue over two years to $4.47 billion in 2025 and achieving a strong net income of $1.88 billion, the company demonstrated operational excellence powered by proprietary order routing, self-clearing technology, and innovative features like fractional shares and 24-hour trading. Its acquisition of Bitstamp in 2025 accelerates crypto capabilities and international reach, underpinning further growth potential amid ongoing regulatory challenges and competitive pressures. Capital allocation remains disciplined with large share repurchases supporting an estimated 23.6% ROE and strong free cash flow generation.

From Startup to Profitability: Examining Robinhood’s Revenue and Earnings Surge

Robinhood Markets has charted a remarkable financial evolution since its founding in 2013 as a disruptor democratizing stock trading through commission-free access. The company’s financial trajectory between fiscal years 2022 through 2025 illustrates the maturation from operating losses into demonstrating substantial profitability and cash flow strength.[F1]

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 4.5 | 1883 | 1638 | +51.6% | +33.5% |

| 2024 | 3.0 | 1411 | -157 | +58.2% | +360.8% |

| 2023 | 1.9 | -541 | 1181 | +37.3% | +47.4% |

| 2022 | 1.4 | -1028 | -852 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 653 | |

| 2024 | 257 | 17.7 |

| 2023 | 608 | -8.1 |

| 2022 | -14.8 |

Source: SEC companyfacts cache [F1].

Note: Capex data for FY2023-FY25 not available from tags.

The jump in revenue from $1.87 billion in FY2023 to $4.47 billion in FY2025 (+51.6% YoY latest) reflects expanded transaction volumes across multiple asset classes including equities, options, futures, and increasingly cryptocurrencies.[F1][S1]

Notably, net income transitioned decisively positive after sustaining losses of $1+ billion annually during FY22-23 to a robust profit of $1.88 billion in FY25—a remarkable turnaround representing a +33.5% increase over FY24's net income of $1.41 billion.[F1]

Operating cash flow metrics reveal similar improvement trends with CFO rising from negative $157 million in FY24 to positive $1.64 billion in FY25—an increase of over elevenfold—highlighting improved operational efficiencies as Robinhood leverages its vertically integrated platform.[F1]

Key Drivers Behind 2025’s Growth: Platform Innovation and Market Position

Robinhood's competitive moat is anchored by its cloud-native technology stack enabling rapid scale combined with proprietary order routing algorithms that optimize payment for order flow (PFOF) economics while simultaneously meeting stringent "best execution" regulatory requirements.[S1][S16]

Its broad multi-asset offering includes commission-free trading on stocks, ETFs, options contracts—including innovative event contracts—and perpetual futures platforms active through Rothera Joint Venture.[S2][S16]

Innovations such as fractional share trading unlock investment flexibility for customers investing small sums or aiming for diversified portfolios.[S1][N12] Complementing this are recurring investments options that encourage steady participation.

Margin lending dynamics have evolved prudently within regulatory guidelines to support leverage without compromising risk controls,[S5] while securities lending programs generate additional revenue streams from customer stock loan-outs.[S16]

Importantly, Robinhood's self-clearing capacity distinguishes it operationally; controlling clearing processes reduces dependence on third-party parties which lowers costs and enhances settlement oversight—critical in volatile markets where trade execution precision impacts reputational trust.[S2][S25]

Combined with frictionless UX design targeting both novices and seasoned traders through Robinhood Legend desktop interface launched in key markets,[N12] these pillars underpin sustained transaction-based revenue growth despite competitive intensity.

Expanding the Footprint: International Growth and Crypto Integration through Bitstamp

Robinhood’s international strategy has accelerated via targeted expansion into U.K. and broader Europe with the strategic acquisition of Bitstamp completed in mid-2025.[N12][N3]

Bitstamp brings regulated crypto exchange infrastructure including European Union licenses enabling custodial services compliant with evolving AML/KYC standards prevalent across EU jurisdictions.[S26]

This cross-border market entry materially diversifies Robinhood’s customer base beyond U.S.-centric operations opening multiple avenues for revenue diversification while catering to rising global retail adoption of cryptocurrencies.[N12][S21]

Crypto offerings now integrate tightly with traditional brokerage services creating synergies across customer accounts facilitating seamless fund migration between fiat securities trading and crypto wallets—key for capturing the next-generation investor demographics increasingly interested in digital assets.[N12]

Moreover, the event-driven product innovations coupled with regulated crypto custody underscore Robinhood’s commitment to compliance-driven international scale confronting complex transnational regulations which include U.K.’s FCA oversight alongside Luxembourg’s CSSF among others.[S26][S21]

Risks on the Horizon: Regulatory Pressures and Market Dynamics

While Robinhood’s growth narrative is compelling, it faces significant regulatory headwinds primarily around Payment For Order Flow (PFOF), heightened scrutiny over crypto transactions, privacy laws enforcement, and evolving best execution mandates impacting routing practices.[S4][S6][S9][S25]

Payment for Order Flow continues attracting regulatory proposals aiming to curtail or ban it—a core component of Robinhood's commission-free business model that sustains much of its transaction-based revenue.[S4][S9] Changes here risk compressing margins or forcing structural business shifts.

Previously disclosed settlements involving FINRA and SEC fines exceeding $70 million across multiple matters including suspicious activity reporting delays,[S8][S13] collaring market orders practices,[S9] social media influencer regulatory reviews,[S9] data security incidents,[S14] contribute ongoing compliance cost burdens that could escalate further.

Operational complexity is compounded by fluctuating interest rate environments influencing net interest margins associated with cash sweep programs.[S4] Market volatility also influences trade volumes directly.

International expansion introduces jurisdictional licensing risks; unauthorized service deployments expose Robinhood to fines as regulators push back on unlicensed offerings outside approved territories.[S10][S21][S26]

Litigation exposure remains elevated including class actions tied to earlier volatile market episodes (eg Early-2021 trading restrictions investigations).[S12]

Lastly, competition is intense; incumbents copying commission-free trades combined with technological innovation keep pricing pressures high while some rivals eschew PFOF reducing its market-wide yield baseline impacting Robinhood’s principal revenue source.[S16][S25]

Capital Allocation Focus: Share Buybacks, Cash Flow Strength, and ROE Trends

Capital deployment reflects maturity with a $1.5 billion authorized share repurchase program initiated May '24 comprising significant buybacks ($810 million executed through Q3'25 increasing to $653 million full year).[S18][S23] Such buybacks indicate management confidence balancing cash deployment towards shareholder returns against organic growth funding.

Liquidity appears robust at fiscal year-end '25 with ~$4.3 billion cash plus equivalents supporting operational flexibility; current ratio stands at approximately 1.26 evidencing prudent working capital management given sizable customer deposit bases accounting for current liabilities exceeding $28 billion.[F1]

Approximate Return on Equity was calculated near ~23.6% based on net income divided by average equity balances ($7+ billion equity base), suggesting effective reinvestment return attributable to operating leverage gains post-turnaround.[F1]

Free cash flow projection—estimated at approximately $1.61 billion (CFO less limited CapEx)—supports balance sheet strength while enabling continued programmatic repurchases absent dividend payouts historically not provided by Robinhood thus far.[F1][S23]

Capital discipline complements operating model reinforcement; repurchase timing dynamically linked to market conditions within regulatory constraints notably including limitations imposed by recent anti-dilution taxes on buybacks such as U.S Inflation Reduction Act provisions.[S18][S23]

What to Watch: Market Metrics and Product Launches Guiding Future Outlook

Despite lack of explicit forward guidance,[N12] key performance indicators bear watching as leading signals of momentum:

- Early Q1 '26 saw reported rise in platform assets suggesting likely tailwinds for transactional fees as client engagement expands post-holiday season spikes typical in retail investing cycles.[N1]

- The launch of Retail Venture Investing (RVI) initiatives broadening retail access to traditionally private equity asset classes may catalyze new investor segments aligning with democratization mission,

- Expansion within cryptocurrencies leveraging Bitstamp's licensed infrastructure could realize incremental fee revenues amid evolving regulation-constrained markets,

- Ongoing order flow economics affected by best execution interpretive shifts will be pivotal; monitoring changes emanating from SEC/FINRA rule proposals is critical,

- Competitive marketing campaigns by rivals might pressure acquisition costs increasing churn rates;

- Cybersecurity enhancements remain crucial for preserving trust following prior incidents;

- Regulatory dialogues around social media marketing continue influencing customer acquisition channels restricting reach if tightened further[S9].

Analysis:

In absence of concrete guidance within filings or press releases up to Feb ’26,[N12][S3] investors should focus on quarterly volume metrics alongside retention statistics as leading variables forecasting sustained momentum or vulnerability phases. Royalty-free API integrations enabling third-party robo-advisory services via Robinhood could create complementary recurring revenue avenues worthy of observation going forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments