Dissecting Social Commerce Partners Corp’s Financial Opacity Amid Sparse Disclosures

An investigative look into SCPQ’s limited SEC filings reveals significant informational gaps clouding its financial and operational narratives.

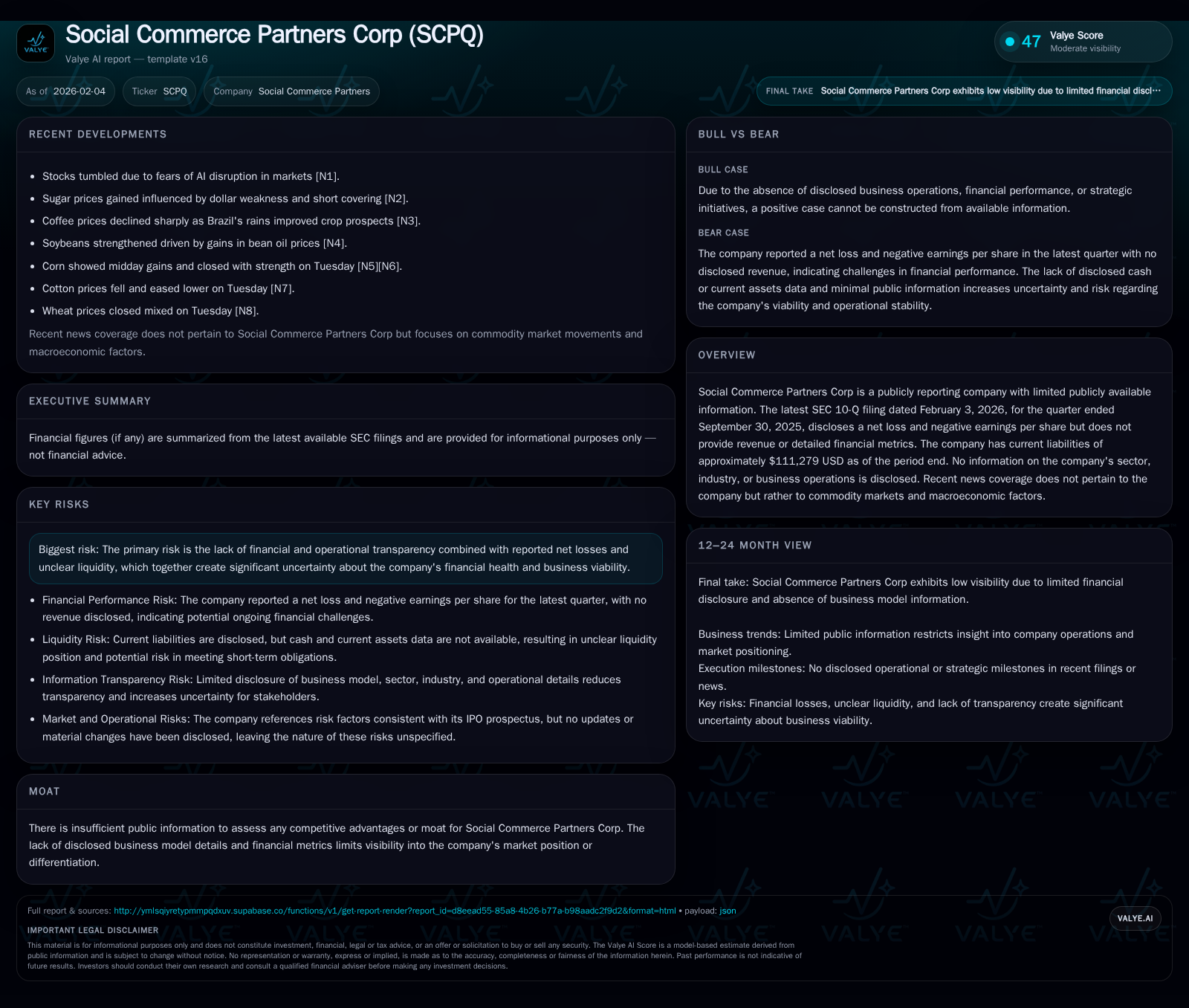

Social Commerce Partners Corp (SCPQ) represents a distinctive case study in the challenges of analyzing publicly reporting entities with minimal disclosure. The latest SEC 10-Q from early 2026 confirms net losses and current liabilities but conspicuously omits revenue and business context. This opacity impedes traditional valuation or competitive assessment frameworks, underscoring elevated investor risk tied to transparency voids. Analysts must grapple with the fundamental uncertainty presented by SCPQ’s blank operational canvas and unchanged IPO risk factors.

A Public Company Cloaked in Silence: Who is Social Commerce Partners Corp?

Social Commerce Partners Corp stands as a curious figure on the public stage—listed, filing quarterly reports as mandated, yet withholding foundational details that typically inform any meaningful analysis. Unlike its peers whose filings illuminate sectors, industries, and geographic footprints, SCPQ offers none. There is no official sector designation nor industry classification disclosed; even basic descriptions of its operations, markets served, or business models are absent [F1][S2]. This scarcity of information invites questions about the company’s transparency and complicates any attempt to situate SCPQ within established market frameworks. The usual matrix of competitive positioning, peer benchmarking, and sector dynamics simply cannot be applied here with any degree of confidence.

Decoding the SEC Filings: Available Financial Snapshots and What They Suggest

The company's most recent quarterly filing — a 10-Q dated February 3, 2026, covering the period ended September 30, 2025 — provides a slender thread to grasp its financial story [S2][F1]. It reports a net loss approximating $52,729 USD while carrying current liabilities around $111,279 USD. However, glaring omissions are stark: revenue figures are not disclosed, nor are cash flow statements that could hint at operating health or funding sufficiency. Such gaps restrict interpretation strictly to observable negatives — expenses indisputably exceed incomes; obligations exist without clarity on asset backing or liquidity sources. The absence of a revenue line heightens concern about operational scale or activity level and poses challenges in projecting future prospects based on concrete data.

The Net Loss Narrative: Assessing SCPQ’s Latest Reported Deficit

A net loss of roughly $52,700 is not necessarily devastating in isolation for companies in developmental stages or investing heavily in growth. Yet when this figure stands unaccompanied by any revenue disclosure—or narrative explaining capital deployment—the verdict tilts toward red flags for analysts seeking signals on sustainability [F1]. Losses suggest outflows surpass inflows; persistent deficits imply structural challenges unless offset by external funding or clear market opportunity roadmap. SCPQ’s silence on these dynamics leaves interpretations severely constrained. Without more extensive disclosures about business progress or strategy execution manifested through revenue trends, the loss figure alone accentuates uncertainty rather than clarifies performance trajectory.

Liabilities on the Ledger: Weighing Current Obligations Against Unknown Assets

Current liabilities nearing $111K reflect debts payable within a year potentially demanding cash outflows in the near term [F1]. Yet no corresponding asset disclosures surface — no indication if SCPQ holds liquid assets or long-term resources capable of cushioning such claims. This lopsided balance sheet fragment raises questions about working capital sufficiency and solvency robustness amid negative earnings. While $111K may be modest in absolute scale compared with many public entities, for a company invisible in terms of operations it stands as a meaningful figure warranting scrutiny. Without evidence of counterbalancing financial strength elsewhere on the books, these obligations could constrain flexibility or even threaten going concern status if unaddressed.

Absent Revenue and Operations: The Void in Sector and Industry Identity

A central challenge in evaluating SCPQ is this complete void regarding what it actually does. No disclosed sector affiliation — be it technology, retail, manufacturing, healthcare — deprives analysts of critical context to frame earnings expectations or benchmark expense structures [F1][S2]. Similarly missing is any mention of an industry vertical or target market geography; such omissions undermine efforts to understand competitive landscapes or growth dynamics that usually underpin investment theses. Typical analytical paradigms rely upon reference points drawn from peer performance metrics; here those points simply vanish. This informational vacuum obstructs any conventional appraisal beyond bare financial figures.

Investor Risks in the Shadows: Transparency Void and Market Implications

The bulk of uncovered risks stem directly from this profound lack of transparency [S2][F1]. In addition to net losses and liability levels unattributable to reassuringly visible revenue streams or assets lies the persistence of unamended IPO risk disclosures detailed initially at listing. The filing explicitly notes no material changes to those pre-existing risk factors as of this quarterly report — effectively an admission that known uncertainties remain unresolved after several reporting cycles [S2]. For buy-side analysts accustomed to deep due diligence supported by comprehensive data sets, such opacity fosters skepticism about valuation integrity and undermines confidence in management communications.

The Moat Mystery: Why Competitive Advantages Remain Undisclosed

Typical moat analyses seek evidence of sustainable differentiation—intangibles like proprietary technology, robust brand equity, network effects, scale advantages—manifested often through metrics such as customer acquisition cost trends or margin profiles. SCPQ offers none [F1]. No discussion exists regarding intellectual property holdings; no strategic positioning statements; no competitive landscape mapping. In the absence of operational transparency combined with consistent reporting silence around unique capabilities or market positioning, one must consider competitive advantages purely speculative at best—if present at all.

Contextualizing SCPQ Within Today’s Market Noise and Unrelated News Dominance

An additional hurdle emerges amid recent news cycles dominated largely by commodity price fluctuations and macroeconomic themes unrelated to SCPQ's activities [N1][N3][N4][N6][N10][N13]. Despite being publicly traded, SCPQ does not appear in headline coverage referencing corporate developments or sector trends. Instead, attention centers around other firms’ earnings updates (e.g., GSK), commodity rallies (soybeans, precious metals), currency shifts (dollar retreat), and large financial sector moves (Zurich's Beazley bid). This disconnect suggests very low engagement from market commentators and informs an overall impression of marginal visibility for SCPQ among key stakeholders.

Next Steps for Analysts: How to Approach Companies with Minimal Data

Given these layered opacity issues highlighted across financial statements and external information flows alike, analysts must adopt heightened caution when approaching SCPQ [S2]. Primary recommended steps include closely monitoring future SEC submissions for expanded disclosures or meaningful amendments to IPO risk factors previously flagged but not resolved. Where feasible direct inquiries toward management—through investor relations channels—may offer incremental insight though answers may remain limited given historical reticence. Portfolio managers faced with such profiles often defer positive judgements pending greater clarity while maintaining alertness to potential shifts in reporting practices that unlock actionable intelligence.

In sum, Social Commerce Partners Corp epitomizes the complexity inherent in evaluating publicly listed entities whose filings reveal more questions than answers. The net loss coupled with liabilities set against blank operational canvases creates a landscape where certainty is elusive rather than assured. Our review underscores a fundamental tension between regulatory compliance via minimalist disclosure versus investor demand for transparency essential to confidence-building analysis.

This report reflects information available as of early February 2026 grounded strictly on disclosed regulatory filings and factual news coverage without conjecture beyond documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments