Sadot Group Confronts Legal, Operational, and Capital Challenges in Global Agri-Foods Pivot

Recent quarterly disclosures highlight Sadot Group's intensified focus on its agri-commodity supply chain amid legal disputes and liquidity strains.

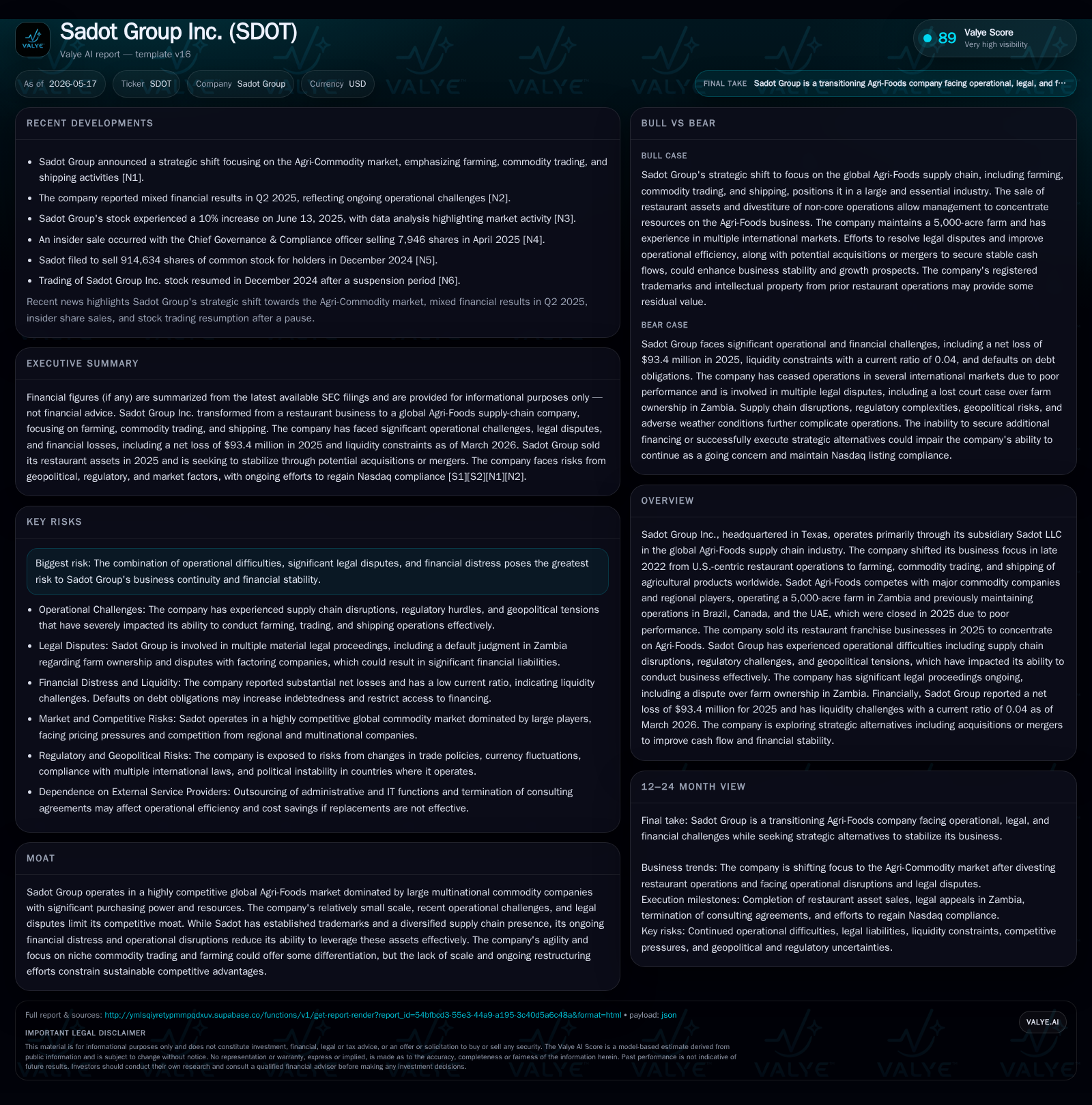

Sadot Group Inc. has shifted from its prior U.S.-centric restaurant operations to establish itself in the global Agri-Foods sector, centering on farming, commodity trading, and shipping. The latest quarterly filing underscores ongoing operational disruptions, legal disputes, and severe liquidity constraints resulting in delisting notices from Nasdaq. While the company operates a flagship 5,000-acre farm in Zambia and engages in commodity trading, legal challenges and impaired assets have constrained growth prospects. The firm is actively pursuing strategic options to restore compliance and financial stability but faces significant execution risks due to scale disadvantages and unfavorable market conditions.

Recent Operating Update: Intensified Struggles Highlighted in Q1 2026 Filing

Sadot Group’s May 15, 2026 Form 10-Q lays bare a challenging near-term operating environment exacerbated by ongoing legal proceedings, supply chain disruptions, regulatory hurdles, and liquidity pressures [S2]. The Company disclosed receipt of a Nasdaq letter citing noncompliance with minimum stockholders’ equity requirements—a critical status that puts the firm at risk of delisting unless remedied within specified deadlines [S3]. Sadot is reportedly preparing a compliance plan but emphasizes uncertainty whether Nasdaq will accept it or provide extensions.

Operationally, Sadot continues to face severe disruptions across its global supply chain that impair its core Agri-Foods businesses—farming major commodities like soybean meal, wheat, and corn; commodity trading; and shipping via dry bulk cargo vessels. Challenges include sourcing delays for raw materials exacerbated by geopolitical tensions and trade restrictions; logistical bottlenecks impacting transportation efficiency; adverse weather conditions affecting crop yields; labor shortages; regulatory complexities especially in African jurisdictions; and equipment failures [S1], [S2].

Notably, Sadot recognized an $11.8 million impairment related to its majority-owned subsidiary's approximately 5,000-acre farm operations in Zambia after a default judgment was entered against it in late 2025 [S1], [S22]. Although the company has appealed this ruling—and seeks recovery of $3.5 million—the ruling creates material uncertainty over the asset’s value and future utility.

The Company’s broader international footprint has contracted materially as underperforming operations in Brazil, Canada, the UAE, Ukraine, and Singapore were closed between late 2024 through 2025 due to lackluster performance or strategic realignment [S1], [S22]. This refocus aims to concentrate resources on core agri-commodity activities but also narrows geographic diversification.

Business Model: From Restaurants to Global Agri-Foods Supply Chain

Sadot Group fundamentally transformed its business model starting late 2022 when it pivoted away from a U.S.-centric restaurant portfolio toward becoming an integrated global agri-food company [S1]. Now headquartered in Burleson, Texas, Sadot operates via subsidiary Sadot LLC internationally across farming (notably Zambia), commodity trading across Americas (via Sadot Latam), and shipping agricultural products worldwide.

Revenue originates primarily from sales of agricultural commodities such as soybean meal, wheat, corn—as either raw materials or feedstock—shipped globally using dry bulk cargo vessels [S1],[S22]. Revenue drivers include volumes traded/farmed; contract pricing dependent on highly volatile commodity markets; mix shifts toward higher-value crops (avocado/mango trees); geographic reach; and currency fluctuations.

The company earns consulting fees for facilitating trade routes (e.g., agreements with Buenaventura Trading LLC until its cancellation) but has scrapped profit-sharing arrangements due to poor operational returns [S25]. Its farming operations are capital intensive requiring substantial capex for land acquisition/provider contracts (e.g., Indonesia farmland deposit written off Q4 2025) and infrastructure amidst ongoing regulatory challenges [S22].

Sadot's recent contraction of physical presence outside Zambia raises questions about sustainable reach versus competitors who leverage multi-regional scale. Operational execution depends heavily on managing complex cross-border regulations including taxation (with exposure to Brazilian Real, Canadian Dollar, Zambian Kwacha exchange rates), environmental standards involving genetically modified organism policies, trade tariffs/subsidies regimes as well as navigating evolving political instabilities or sanctions [S1], [S2].

Industry Structure & Competitive Position: Small Player Against Powerful Multinationals

Sadot operates in a competitive arena dominated by large multinational commodity conglomerates known collectively as ABCD firms—ADM, Bunge, Cargill, Louis-Dreyfus—and sizable regional players often benefiting from extensive supply chains & logistics networks plus deep capital pools.

Relative to these incumbents:

- Sadot is small-scale with limited buying power impacting price negotiations.

- Lack of diversified geographic assets post-closure of Brazil/Canada/UAE limits revenue sources.

- Financial distress constrains ability to invest in capex or technology needed for efficient supply chain integration or enhancements.

- Legal distractions from ongoing court proceedings siphon resources away from competitive initiatives.

Judgments already impair balance sheet (Zambia farm) with uncertainty prolonging capital lock-up periods [S21], [S16].

- Liquidity Crisis: With a current ratio at approximately 0.04 reflecting negligible short-term assets against substantial liabilities ($60M+), ongoing cash flow deficits necessitate urgent capital injections or risk default accelerations while triggering dilution liabilities from convertible debt instruments held by creditors [F1], [S27].

- Regulatory Complexity: Navigating multi-jurisdictional agricultural policies amid changing trade rules requires continuous adaptation at operational cost.

- Competitive Pressures: Losing ground to dominant players strains pricing power making margin improvement difficult absent product/service uniqueness.

- Operational Inefficiencies: Inconsistent farming yields due to inclement weather/labor shortfalls/equipment failures exacerbate unpredictability impacting contract fulfillment capabilities.

- Nasdaq Compliance Uncertainty: Failure to meet listing requirements within deadlines would significantly restrict capital market access reducing visibility among potential institutional investors further tightening financing options [S3].

- Macroeconomic Factors: Global recessions or inflationary periods could depress demand for traded commodities severely impacting revenue streams [S5].

What To Watch Next

Investors and analysts should monitor:

- Acceptance status of Nasdaq compliance plan filings alongside timing/extensions granted or denied.

- Progress updates on Zambia farm appeal outcome within expected one-year timeframe including potential settlements or further impairments.

- Quarterly reports disclosing any resolution progress on legal disputes particularly those involving multi-million-dollar claims like Lombard Trading International Corp. cases.

- Signs of reengagement or successful onboarding of new trading partners replacing former agreements like Buenaventura.

- Changes in working capital metrics signaling improvement or deterioration against liquidity crunch backdrop.

- Any announcements of financing deals including stock issuances or convertible note restructurings potentially dilutive to shareholders.

- Operational KPIs showcasing volume growth or margin recovery indicative of stabilized supply chains amidst existing geopolitical headwinds.

Financial Profile Snapshot (As of Q1 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $12mm | |

| 2026-03-31 | ||

| Net debt | $443753 | |

| 2026-03-31 | ||

| Current assets | $2mm | |

| 2026-03-31 | ||

| Current liabilities | $60mm | |

| 2026-03-31 | ||

| Current ratio | 0.04x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & Equivalents | $11.7 million | |

| 2022-09-30 | ||

| Total Debt | $12.1 million | |

| 2026-03-31 | ||

| Current Assets | $2.38 million | |

| 2026-03-31 | ||

| Current Liabilities | $60.1 million | |

| 2026-03-31 | ||

| Current Ratio | 0.04 | |

| 2026-03-31 |

This snapshot reveals critical liquidity challenges with current liabilities vastly exceeding liquid assets reflected by the alarmingly low current ratio underscoring urgency for refinancing or asset sales/operational turnaround [F1], [S27]. While $11.7 million cash reported at fiscal year-end remains significant on absolute levels it falls short compared to near-term obligations indicating stretched financial flexibility.

Summary Analysis

Sadot Group’s transition into global agri-foods represents a bold strategic pivot potentially tapping into fundamental food security themes worldwide. However, recent quarters underscore that this path is fraught with tight cash flows amidst costly legal entanglements impairing key assets like the Zambian farm. The Company’s reduced international footprint reflects an unwinding of overextension but still leaves it vulnerable to market giants wielding superior scale advantages. Liquidity deficiencies magnify refinancing risks especially under Nasdaq delisting pressures challenging investor confidence.

Substantial uncertainties persist regarding timely resolution of pending litigations critical for asset preservation alongside sustained efforts needed to streamline fragmented supply chains hindered by geopolitical volatility. Future viability hinges upon executing a credible Nasdaq compliance roadmap supported by tangible operational improvements coupled with securing stable funding sources without excessive dilution—or alternatively strategic divestitures or partnerships enabling scale benefits.

Until such milestones are achieved convincingly the enterprise remains embroiled in a precarious phase spotlighting the typical risks small players face competing against entrenched agri-supply giants in an industry sensitive both to macroeconomic cycles and localized political/regulatory shocks.

This analysis is based strictly on publicly available SEC filings through May 2026 and industry context without offering investment recommendations or forecasts. Readers should perform their own due diligence regarding evolving developments affecting Sadot Group Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments