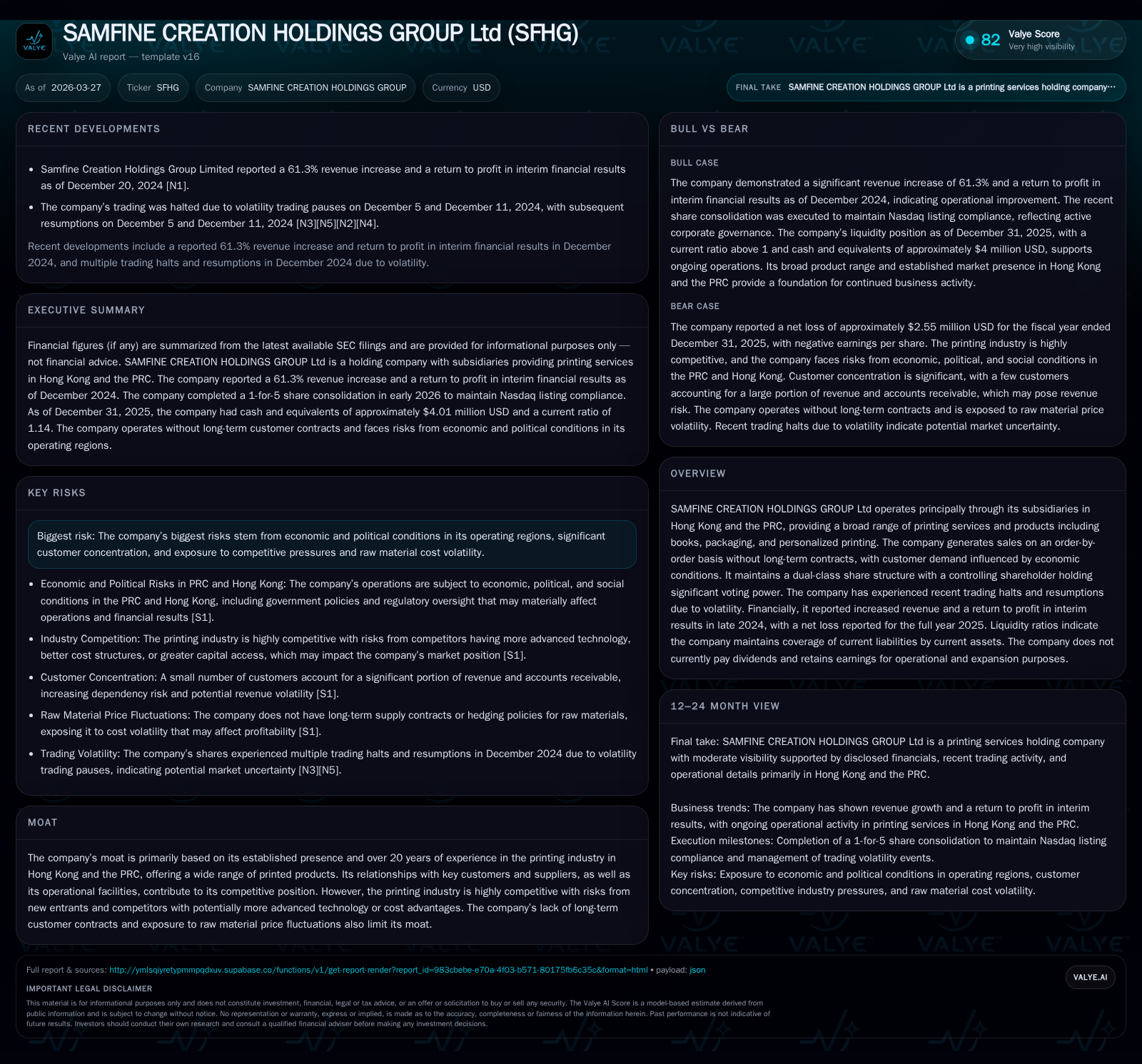

SAMFINE CREATION HOLDINGS Reports Revenue Growth While Operating Losses and Cash Flow Worsen in 2025

SFHG’s 2025 results show rising revenue alongside deepening net losses, increased capital spending, and liquidity sustained by a share consolidation amid cost and market pressures.

SAMFINE CREATION HOLDINGS Group (SFHG) operates primarily in Hong Kong and the PRC printing markets with over two decades of experience. While revenue increased to $10.46 million in the first half of 2025, the company recorded significant operating and net losses for the full year. Operating cash flow deteriorated alongside a sharp rise in capital expenditure reflecting strategic investments. The company executed a 1-for-5 share consolidation to maintain Nasdaq listing compliance. Liquidity remains adequate with a current ratio of approximately 1.14x, though operating cash flow trends highlight ongoing financial pressure. SFHG faces margin challenges from raw material cost volatility and competitive market dynamics, compounded by an order-driven model without long-term contracts. No dividends have been declared, with earnings retained for operational needs and expansion.

Historical Financial Overview: Revenue Growth Contrasted with Rising Losses

SAMFINE CREATION HOLDINGS Group (SFHG) reported revenue of approximately $10.46 million for the first half of 2025 [F1]. Despite this top-line growth, profitability metrics deteriorated significantly. Operating income declined sharply to a loss of $2.77 million for full-year 2025 compared with a loss of $297K in 2024, representing an over 830% year-over-year decrease [F1]. Net income followed suit, with losses expanding from $342K in 2024 to $2.55 million in 2025, a decline exceeding 640% [F1].

Operating cash flow also worsened considerably, decreasing by more than 75% from negative $1.54 million in 2024 to negative $2.7 million in 2025 [F1]. Capital expenditures rose markedly to $518K in fiscal year 2025 from negligible levels previously, signaling increased investments likely aimed at capacity or technology upgrades within its printing operations [F1][S5]. This combination has resulted in negative free cash flow nearing -$3.22 million.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | -3 | -3 | 518156 | -643.3% |

| 2024 | 0 | -2 | 0 | 3038 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -38.3 |

| 2024 | -2 | -3.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue is reported for first half year; profitability and cash flow figures correspond to full fiscal years.

Market Structure Adjustments: Share Consolidation and Trading Activity

In response to share price volatility and to meet Nasdaq listing requirements under Rule 5550(a)(2), SFHG executed a one-for-five share consolidation effective February 27, 2026 [S2]. This reduced outstanding shares from approximately 20.3 million to about 4 million while maintaining existing ownership percentages due to uniform consolidation across Class A and Class B shares [S2][S4].

The company’s dual-class structure features Class A Ordinary Shares with one vote each and Class B shares carrying twenty votes each — concentrating voting control among insiders [S4]. These governance features alongside the share consolidation may influence market liquidity and investor perception.

Operational Context: Mature Printing Service Provider amid Competitive Pressures

SFHG’s core business involves providing printing services principally through subsidiaries located in Hong Kong and mainland China offering products including children’s books, educational materials, art books, packaging products such as shopping bags and boxes [S1]. Sales are generated on an order-by-order basis without long-term contracts which limits revenue visibility.

The printing industry in this region is highly competitive with risks including new entrants leveraging advanced technologies or cost advantages that could pressure SFHG’s pricing and margins [S1]. The company faces additional challenges from fluctuating raw material prices — primarily paper costs linked to global wood pulp markets — without hedging mechanisms or long-term supply agreements [S1][S22].

Macro-Political Factors Influencing Demand Stability

SFHG’s operations are subject to economic and political conditions prevailing in Hong Kong and the PRC which can impact customer demand patterns given discretionary nature of many printed products [S1][S17]. Changes in regulatory environments or political arrangements could affect business confidence or capital availability impacting sales.

Capital Allocation: Dividend Policy and Investment Focus

The company has not declared or paid dividends recently; all earnings are retained to support operations and growth initiatives [S3][S4]. Dividend payments depend on board discretion subject to solvency requirements under Cayman Islands law and availability of funds received from subsidiaries [S3][S13].

Capital expenditures expanded substantially reflecting strategic investments potentially aimed at enhancing production capabilities or efficiency given the scale of increase from prior periods [F1][S5][S14].

Operating cash flows remain negative due largely to net losses combined with working capital increases driven by higher accounts receivable balances related to sales growth but delayed payments [F1][S19][S21].

Financing arrangements include banking facilities secured by controlling shareholders’ guarantees supporting liquidity needs amid operating cash burn [S6][S7][S9]. Lease obligations contribute fixed payment commitments but no off-balance sheet liabilities were identified that would materially affect financial flexibility [S11][S19].

Liquidity Position as of December 31, 2025

Current assets totaled approximately $13.12 million against current liabilities of about $11.46 million yielding a current ratio near 1.14x indicating sufficient but tight short-term liquidity coverage [F1]. Cash and equivalents stood at roughly $4 million at year-end reflecting ongoing cash consumption driven by operational losses and working capital demands [F1].

Outlook Considerations

No formal forward guidance has been disclosed regarding profitability improvements or revenue targets. Key indicators for monitoring include gross margin trends reflecting cost pass-through ability; operating income stabilization post-investment; working capital management effectiveness; and potential shifts towards longer-term contracts enhancing revenue predictability.

Continued scrutiny of macroeconomic developments across Hong Kong and the PRC alongside competitive dynamics will be essential for assessing SFHG’s path toward financial stability.

This report is based on publicly available SEC filings dated March 27, 2026 (20-F) along with related disclosures without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments