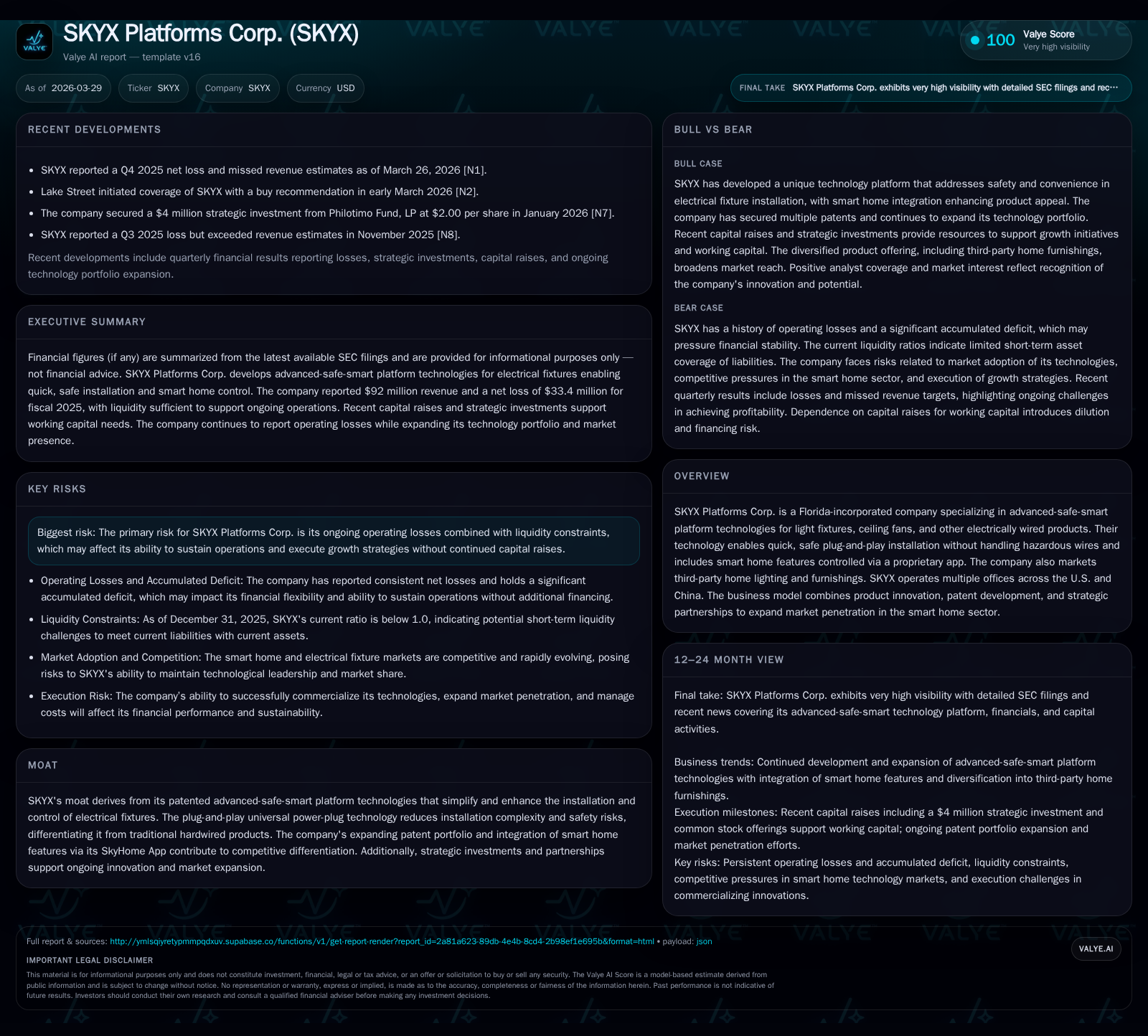

SKYX Platforms Navigates Innovation and Liquidity Challenges Amid Persistent Losses

SKYX Platforms Corp. leverages patented smart home electrical technology while managing sustained operating deficits and tight liquidity conditions.

SKYX Platforms Corp. has developed a patented plug-and-play electrical platform technology aimed at simplifying installation and enhancing safety for home fixtures, supporting modest revenue growth since 2016. Despite technological progress, the company reported an operating loss exceeding $29 million in 2025 with ongoing negative cash flows, presenting liquidity pressures. Recent equity financings totaling nearly $30 million have provided capital relief but highlight continued funding requirements. The company's outlook depends on expanding market penetration, further patent development, and strategic partnerships amid competitive and financial headwinds.

Innovative Platform Technology Underpinning Early Revenue Growth

SKYX Platforms Corp. has developed an advanced-safe-smart platform technology tailored for electrically wired home products such as light fixtures and ceiling fans. Central to its offering is a patented universal power-plug that simplifies installation by enabling plug-and-play functionality, mitigating the hazards of traditional hardwiring methods . This innovation targets a key challenge in smart home integration—balancing ease of use with safety.

Complementing hardware innovation is the proprietary SkyHome App, which integrates smart controls directly with connected products to enhance user experience and retention within an increasingly competitive IoT market . The company’s patent portfolio supports this technological moat against commoditization.

Historical financial data shows modest revenue progression from $7.0 million in fiscal year 2016 to approximately $7.7 million in fiscal year 2017, representing a 9.8% year-over-year increase consistent with initial commercialization efforts [F1]. This revenue base reflects early-stage traction typical for hybrid hardware-software platform ventures.

Financial Performance: Persistent Losses during Modest Top-Line Growth

While revenues have grown modestly in earlier years, SKYX continues to face significant profitability hurdles. Operating losses improved slightly to approximately -$29.1 million in fiscal year 2025 from -$32.1 million in the prior year—a year-over-year improvement of about 9.3%—indicating some operational leverage as expenses are spread over growing activities [F1].

Net losses followed a similar trajectory with $33.4 million reported in 2025 compared to $35.8 million in 2024, reflecting a 6.6% improvement but still demonstrating substantial red ink on the income statement [F1]. Operating cash flow remained negative at roughly -$13.3 million for 2025 versus -$18.3 million the prior year; this partial recovery aligns with ongoing high investment in R&D and marketing necessary for product advancement [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -33 | -13 | -29 | +6.6% |

| 2024 | -36 | -18 | -32 | +10.0% |

| 2023 | -40 | -13 | -38 | -47.0% |

| 2022 | -27 | -14 | -27 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | ROE% |

|---|---|---|

| 2025 | 1020616 | 728.3 |

| 2024 | -882.4 | |

| 2023 | 38055 | -244.9 |

| 2022 | 38055 | -341.9 |

Source: SEC companyfacts cache [F1].

Note: Post-2017 revenue figures are not explicitly detailed beyond growth commentary; operating income and net losses are per audited SEC filings [F1].

Capital Structure and Liquidity Profile

As of December 31, 2025, SKYX reported cash and cash equivalents of approximately $8 million against current liabilities of about $24.6 million resulting in a current ratio near 0.63—indicative of significant liquidity pressure [F1][S4][S10]. This shortfall highlights working capital constraints that may limit operational flexibility without additional financing or restructuring.

Capital raising activities between late 2025 and early 2026 include multiple equity financings: issuance of Series A-2 Preferred Stock raising around $2 million [S9], common stock sales generating approximately $4 million [S7], and a notable registered direct offering completed January 26, 2026 raising roughly $25 million at $2.50 per share [S13][S16]. These proceeds support working capital needs and general corporate purposes amid ongoing cash burn.

Restricted cash collateralizing letters of credit decreased from about $2.8 million to roughly $2 million over recent years—reflecting negotiated credit arrangements linked to leasing or supplier commitments [S4][S6].

Unusually for a company reporting consistent losses, SKYX paid dividends exceeding $1 million in fiscal year 2025 tied primarily to preferred stock obligations that carry cumulative dividend rights at stipulated rates [F1][S11][S12][S23]. There is no evidence of share repurchase programs.

Strategic Outlook and Market Positioning

SKYX aims to strengthen its competitive positioning through ongoing patent development and expansion of strategic distribution partnerships primarily across U.S.-China corridors where it maintains operations . The integrated SkyHome App remains central to its value proposition by enhancing device interoperability within consumer IoT ecosystems.

Recent analyst coverage initiating with a buy recommendation signals market confidence in SKYX’s technology differentiation despite the absence of explicit guidance on future revenues or shipment volumes [N3]. The combination of hardware patents coupled with embedded software functionality creates barriers against commoditized alternatives lacking interoperable plug standards.

Investor Considerations and Risks

Investors should monitor several key factors due to limited public guidance: progression on patent filings extending intellectual property protection; pace of partnership expansion; commercial ramp evidence via shipment disclosures; potential shifts toward profitability through cost management; and capital raise frequency given persistent liquidity concerns.

Risks include continued heavy operating losses necessitating dilutionary capital raises; potential patent enforcement challenges; adoption risks amid competing technologies; and inherent going concern considerations despite auditor affirmations based on management plans addressing liquidity issues [S21].

Disclaimer: This analysis synthesizes publicly available SEC filings and news sources without providing investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments