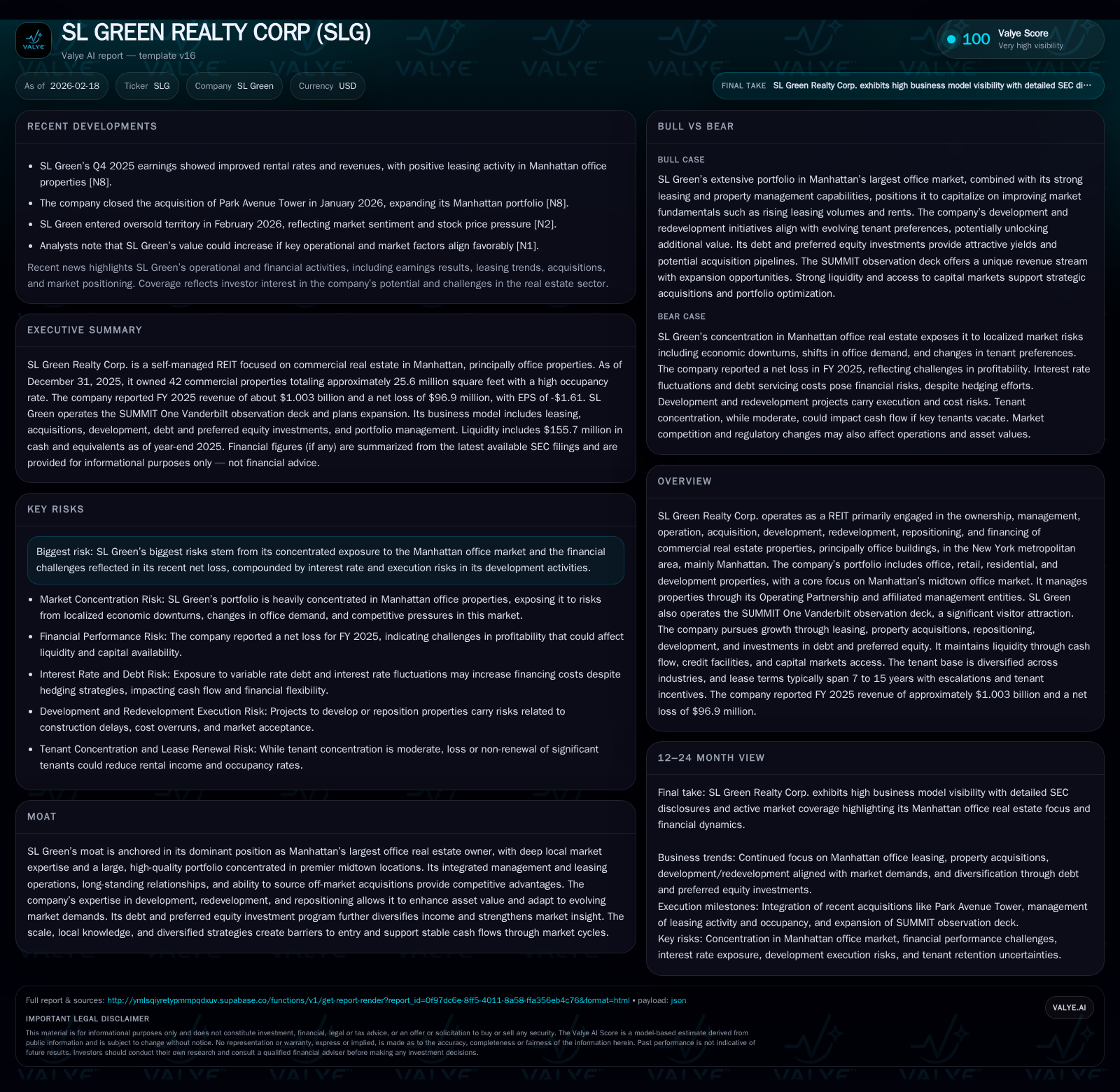

SL Green Realty’s Recovery Balances Office Market Focus with Refinancing and Redevelopment Risks

Manhattan's dominant office landlord rebounds revenue with leasing gains but faces net loss and refinancing deadlines.

SL Green Realty Corp. reaffirmed its status as Manhattan’s largest office landlord with sustained revenue growth driven by leasing improvements and strategic acquisitions in 2025. However, profitability remains challenged, reflecting continued market headwinds resulting in a net loss despite strong operating income. The company’s capital structure shows significant near-term refinancing obligations amid moderate liquidity buffers while focusing on redevelopment and the expansion of its SUMMIT observation deck business to diversify income. Careful execution of leasing, asset repositioning, and debt management will be critical catalysts to unlock shareholder value in 2026.

Historical Performance: Revenue Growth Amid Margin Pressure

SL Green Realty Corp., the preeminent office landlord in Manhattan’s commercial real estate scene, reported total revenues of $1.003 billion for fiscal year 2025, marking a solid 13.2% increase year-over-year from $886 million in 2024 [F1]. This growth was primarily driven by improved leasing velocity and rental rate enhancements across its midtown Manhattan office portfolio — Manhattan being the largest U.S. central business district with approximately 417 million square feet of inventory [S16].

Despite top-line growth, operating income declined by nearly 11% year-over-year to $652 million from $731 million the prior year [F1], reflecting margin compression likely due to rising operating expenses such as property management costs, tenant improvement allowances, and maintenance linked to repositioning older buildings. This divergence underlines increasing cost intensity in managing aging urban core assets amid evolving tenant preferences.

The bottom line showed a net loss of $97 million for FY2025 compared with a net income of $22 million in FY2024 [F1]. This swing reflects non-cash impairment charges on legacy assets amid market uncertainty, interest expense pressures related to corporate debt and joint venture financing, plus fair value adjustments on derivatives and investment portfolios [S21][S23]. These factors highlight ongoing profitability challenges despite improving leasing fundamentals.

Operating cash flow also contracted steeply by 36% year-over-year to approximately $83 million [F1], indicating that while rents stabilized or rose in some submarkets, substantial capital expenditures—particularly for redevelopment projects—and elevated leasing incentives weighed on free cash flow generation capacity. The company plans around $39 million in recurring capital expenditures plus more than $20 million for development or redevelopment at consolidated properties, alongside joint venture commitments exceeding $34 million [S18][S19].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1003 | -97 | 83 | 652 | +13.2% | -540.3% |

| 2024 | 886 | 22 | 130 | 731 | -3.0% | +103.9% |

| 2023 | 914 | -565 | 230 | +10.5% | -623.1% | |

| 2022 | 827 | -78 | 276 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 243 | -2.6 | |

| 2024 | 219 | 0 | 0.6 |

| 2023 | 231 | 0 | -14.9 |

| 2022 | 262 | 151 | -1.7 |

Source: SEC companyfacts cache [F1].

Note: Buyback data is zero for recent years except for earlier periods; Operating Income data unavailable for FY2023.

Portfolio Composition and Market Positioning

SL Green’s portfolio remains heavily concentrated in Manhattan office real estate with ownership or joint venture interests covering approximately 26 million square feet predominantly centered around midtown locations with a weighted average leased occupancy rate above 92% as of December 31, 2025 [S1]. This includes commercial office space complemented by retail footprints (313k sq ft), residential segments (585k sq ft), and active development sites totaling roughly 1.25 million square feet aimed at future repositioning.

The company leverages integrated property management and leasing teams enabling proactive tenant retention strategies supported by deep market knowledge driving off-market lease transactions [S22]. The ancillary SUMMIT One Vanderbilt observation deck business attracted approximately 2.2 million visitors during calendar year 2025 and is positioned for international expansion with a Paris location targeted for opening in 2027 [S16].

Growth Prospects: Leasing Momentum Meets Redevelopment Ambitions

Growth drivers include:

- Leasing Activity: Ongoing improvement in leasing velocity supported by declining vacancies creating upward rental rate pressure especially within premium midtown assets enhanced through modernization efforts.

- Development & Redevelopment: Strategic investments aiming to upgrade building efficiency, tenant amenities, sustainability features, and hybrid work readiness are expected to unlock asset value while addressing evolving occupant demands [S19].

- SUMMIT Expansion: International brand extension into new markets such as Paris offers diversification beyond traditional rent-based revenue streams.

- Debt & Preferred Equity Investments: Opportunistic investments leveraging SLG’s underwriting capabilities broaden yield sources beyond direct property ownership risks concentrated in New York City markets [S16].

However, growth is tempered by risks including elevated interest rates increasing capital costs; shifts toward decentralized work reducing long-term absorption; execution risks on costly renovations potentially compressing margins; and regulatory uncertainties impacting taxation or building standards.

Capital Structure: Navigating Refinancing Challenges Amid Adequate Liquidity

SL Green maintains diversified corporate-level debt comprised of a $1.25 billion revolving credit facility alongside term loans totaling approximately $1.15 billion maturing between late-2025 and mid-2027 subject to extension options [S6][S7][S15][S18][S24]. Property-level mortgage financing adds complexity to maturity schedules requiring careful refinancing given current credit conditions.

Liquidity stands at approximately $156 million in cash complemented by over $850 million undrawn revolver capacity as of late FY2025 providing operational runway through upcoming maturities without immediate distress signals; management reports compliance with all restrictive covenants limiting dividend payments or incremental indebtedness during defaults scenarios [S16][S19][S21][S27][N3].

Interest costs have risen given floating rate exposures hedged primarily via derivatives stabilizing effective borrowing rates near low-to-mid single digits; variable rate debt accounts for roughly one-tenth of total borrowings after considering mitigating variable-rate investments offsetting exposure [S23][S25][S27][S28].

Capital allocation prioritizes liquidity preservation and funding organic growth over share repurchases which have been dormant since FY2022; dividends paid increased modestly to $243 million in FY2025 consistent with REIT distribution requirements [F1][S25][S26].

Key Catalysts & Risks: Execution under Microscope Amid Market Cyclicality

Upcoming milestones include:

- Monitoring renewal rates and new leasing velocity across flagship properties as hybrid work patterns evolve impacting NOI recovery.

- Progress on redevelopment projects unlocking deferred value amid market softness.

- Successful rollout of additional SUMMIT venues validating brand scalability beyond New York.

- Refinancing upcoming debt maturities without onerous rate increases or covenant breaches ensuring stable cost structures.

Risks include:

- High exposure to Manhattan office market vulnerable if flexible workspace preferences permanently reduce demand.

- Execution risk on expensive renovations amid inflationary pressures risking cost overruns.

- Interest rate fluctuations potentially impairing profitability despite hedging.

- Regulatory uncertainties affecting operating costs or capital expenditure requirements.

Conclusion: A Delicate Rebound Balancing Opportunity and Risk in NYC Office Sector

SL Green Realty remains the dominant landlord navigating shifting urban office dynamics through active portfolio management combining steady-state leasing gains alongside strategic development plays enhanced by diversification into visitor experiences like SUMMIT One Vanderbilt [N11]. Despite lingering profitability challenges reflected in net losses driven by non-cash items [F1], liquidity profiles coupled with refinancing pathways provide prudent confidence barring unforeseen disruptions [N3]. Investors should monitor leasing momentum post-pandemic alongside redevelopment execution as pivotal factors shaping sustainable earnings power ahead [N4].

Disclaimer: This report is intended solely for informational purposes based on publicly available information including SEC filings and recent news coverage; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments