Solésence Extends Competitive Edge Through Strategic Partnerships and Debt Management

Recent filings highlight Solésence’s focus on minerals-based personal care and diagnostics ingredients leveraging long-term contracts and prudent capital structure.

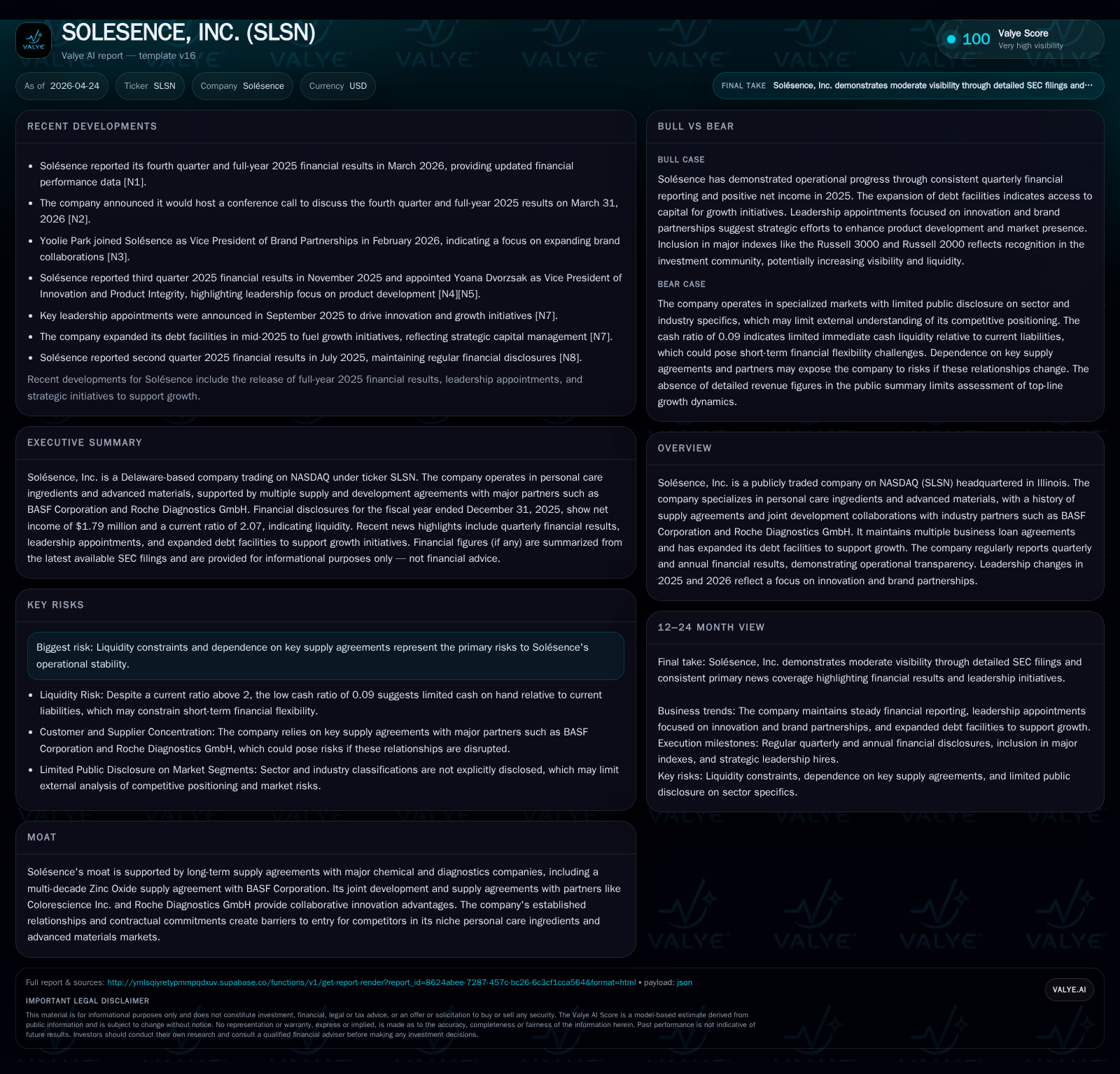

Solésence, Inc., trading on NASDAQ as SLSN, emphasizes its core markets in skin health products and diagnostic life sciences ingredients with a minerals-based product portfolio. The company operates as a single business segment, facilitating streamlined management and reinforcing its niche market focus. Its competitive moat is anchored by a multi-decade Zinc Oxide supply agreement with BASF Corporation alongside joint development agreements with partners such as Roche Diagnostics GmbH and Colorescience Inc. Liquidity management via amended loan agreements with Beachcorp, LLC supports operational stability amid inherent risks tied to contract dependence. Going forward, monitoring innovation pipeline developments and loan maturity amendments will be critical.

Latest Operating Updates Reaffirm Solésence’s Market Focus

Solésence's most recent quarterly report filed on November 12, 2025 ([S2]) highlights the company’s strategic focus on skin health products and diagnostic life sciences ingredients—both areas where its minerals-based solutions claim practical and competitive advantages. The company emphasized close collaboration with existing customers to tailor materials according to precise performance specifications for various end-use manufacturers. Notably, the firm reports operating as a single business segment, simplifying management oversight across its product lines which include both raw materials sold to manufacturing customers and branded Solésence® products marketed directly to skin care companies.

This concentrated segment approach avoids complexities of diversified operations and indicates streamlined execution priorities. Additional updates in the March 31, 2026 event filing ([S3]) confirm continued commitment to these target markets without significant structural changes.

Business Model: Minerals-Based Materials for Skin Care and Diagnostics

Solésence generates revenue primarily through supply contracts for specialty minerals—most notably Zinc Oxide—and advanced material formulations utilized in personal care products and diagnostic assays ([S1]). The company leverages proprietary processing know-how to produce high-purity mineral actives that serve as key functional ingredients in sunscreen formulations (for UV protection) and medical diagnostic components.

Revenue flows via multi-year supply agreements with large industry players such as BASF Corporation, securing steady demand under fixed terms including volume commitments (, [S1]). Joint development agreements supplement pure supply contracts by facilitating co-innovation projects aimed at enhancing product efficacy or expanding application scope, notably with Colorescience Inc., an established cosmetics brand specializing in mineral-based makeup, and Roche Diagnostics GmbH for life sciences applications.

This dual approach—combining ingredient supply with collaborative R&D—provides differentiation versus generic commodity suppliers by embedding Solésence deep within customer value chains through both technical partnership and contractual arrangements.

Market Position Bolstered by Exclusive Supply and Joint Development Agreements

The company’s competitive position rests heavily on its exclusive Zinc Oxide supply agreement with BASF Corporation, which dates back over two decades (, [S17]). This rare multi-decade contract functions as a significant barrier to entry for competitors given the scale, quality standards, and regulatory hurdles associated with these materials.

Additional joint development agreements extend this moat by binding customers like Roche Diagnostics GmbH not only commercially but also through shared innovation initiatives that encourage ongoing collaboration rather than supplier switching ([S6]). Such arrangements foster higher switching costs for customers due to the customized nature of the products developed jointly.

The company's relationships are further reinforced by supply deals with emerging cosmetic brands like Ilia Beauty, Inc., underscoring an ability to adapt products to diverse customer needs while maintaining stable contractual frameworks ([S14]).

Industry Dynamics Encourage Niche Competitive Moat Formation

The personal care ingredient industry increasingly values specialized minerals-based actives that meet rising consumer demand for natural, skin-friendly formulations. Suppliers like Solésence must overcome stringent regulatory compliance and consistent quality demands from OEM customers who typically integrate these ingredients into complex products.

Industry competition includes commoditized mineral producers but Solésence's differentiated positioning via proprietary formulations, joint development partnerships, and long-term contracts reduces price sensitivity relative to commodity peers ().

Supply chain reliability is critical since fluctuations can disrupt end-product manufacturing schedules; thus, Solésence's established contract terms provide customers with confidence in uninterrupted supply.

Growth Drivers: Innovation Pipeline and Customer Collaborations

Recent leadership appointments throughout late 2025 signal management’s intent to prioritize innovation capacity alongside strengthening brand partnerships (). This strategic emphasis could fuel incremental product line extensions or new mineral formulations aligned with evolving industry trends such as enhanced photoprotection or multifunctional skincare actives.

Moreover, joint development initiatives leverage customer insights directly into R&D efforts, increasing the probability that resulting materials meet commercial expectations promptly ([S1], [S2]). Geographic expansion has not been explicitly stated but given the global nature of cosmetics manufacturers and diagnostics firms involved, indirect global reach is implied via partner networks.

Capacity utilization factors or manufacturing scale expansions have not been detailed recently but may emerge as future catalysts if demand growth accelerates beyond existing capabilities.

Potential Headwinds: Liquidity Constraints and Agreement Dependencies

A key risk factor lies in Solésence's reliance on several cornerstone contracts which underpin most of its revenue stream (). Any disruption or nonrenewal could materially affect operational viability given the company's relatively niche market scope.

The company maintains multiple revolving loan agreements secured by accounts receivable and inventory facilities provided by Beachcorp, LLC ([S2]). Amendments enacted through late 2023 extend maturities of these credit lines until October 1, 2025 ([S2]), providing breathing room for near-term refinancing or reduction strategies.

As of year-end 2025 according to [F1] data, cash & equivalents stood at approximately $1.29 million. Current assets exceeded liabilities at roughly a 2.07x ratio indicating adequate short-term coverage though free cash flow remained negative due to substantial capital expenditure activity (3% capex increase YoY) [F1]. Such leverage suggests cautious monitoring is warranted especially if revenue growth slows or working capital intensifies.

Upcoming Catalysts and Execution Metrics to Monitor

Stakeholders should watch for disclosures following the March 31, 2026 earnings call where updated financial results are expected ([N1], [N2], [S3]). Any announcements concerning new partnership agreements or expansions of existing contracts would indicate progress along growth trajectories.

Debt facility amendments or refinancing efforts—potentially extending maturity dates beyond October 2025—will be essential to maintain operational flexibility ([S2], [S3]). Furthermore, milestones related to joint development programs might reveal emerging offerings poised for commercial scale-up.

Monitoring operating cash flow trends post-heavy capex periods may also serve as a barometer for underlying profitability improvements or efficiency gains over coming quarters.

Financial Overview: Capital Structure, Liquidity, and Profitability

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2 | -9 | 2 | -57.7% | |

| 2024 | 4 | 2 | 5 | 5 | +196.5% |

| 2023 | -4 | -2 | -4 | 1 | -67.4% |

| 2022 | -3 | -2 | -2 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 10.2 | |

| 2024 | -3 | 28.3 |

| 2023 | -3 | -230.8 |

| 2022 | -4 | -46.4 |

Source: SEC companyfacts cache [F1]. *Latest available fiscal year data from [F1]

The company delivered a rebound in operating income in FY2025 recovering from losses in prior years yet operating cash flow reverted negative mainly driven by heavy capex spend which exceeded $4 million in FY2024 reflecting investments likely targeted at capacity or process improvements ([F1], [S2]). Despite these pressures net income turned modestly positive at $1.79 million in FY2025 representing approximately a 10% return on equity based on year-end equity balances.

Debt structure centers around business loans with Beachcorp LLC including amended revolving credit lines capped initially at $8 million but currently smaller usage reportedly aligned with asset-backed borrowing bases under covenants ([S2]).

This analysis is based purely on publicly available SEC filings and news releases without any investment recommendation or financial advice offered herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments