SEACOR Marine Holdings Navigates Recovery with Operational Gains and Regulatory Headwinds

SEACOR Marine’s financial turnaround contrasts with ongoing environmental and regulatory challenges that shape its offshore marine services.

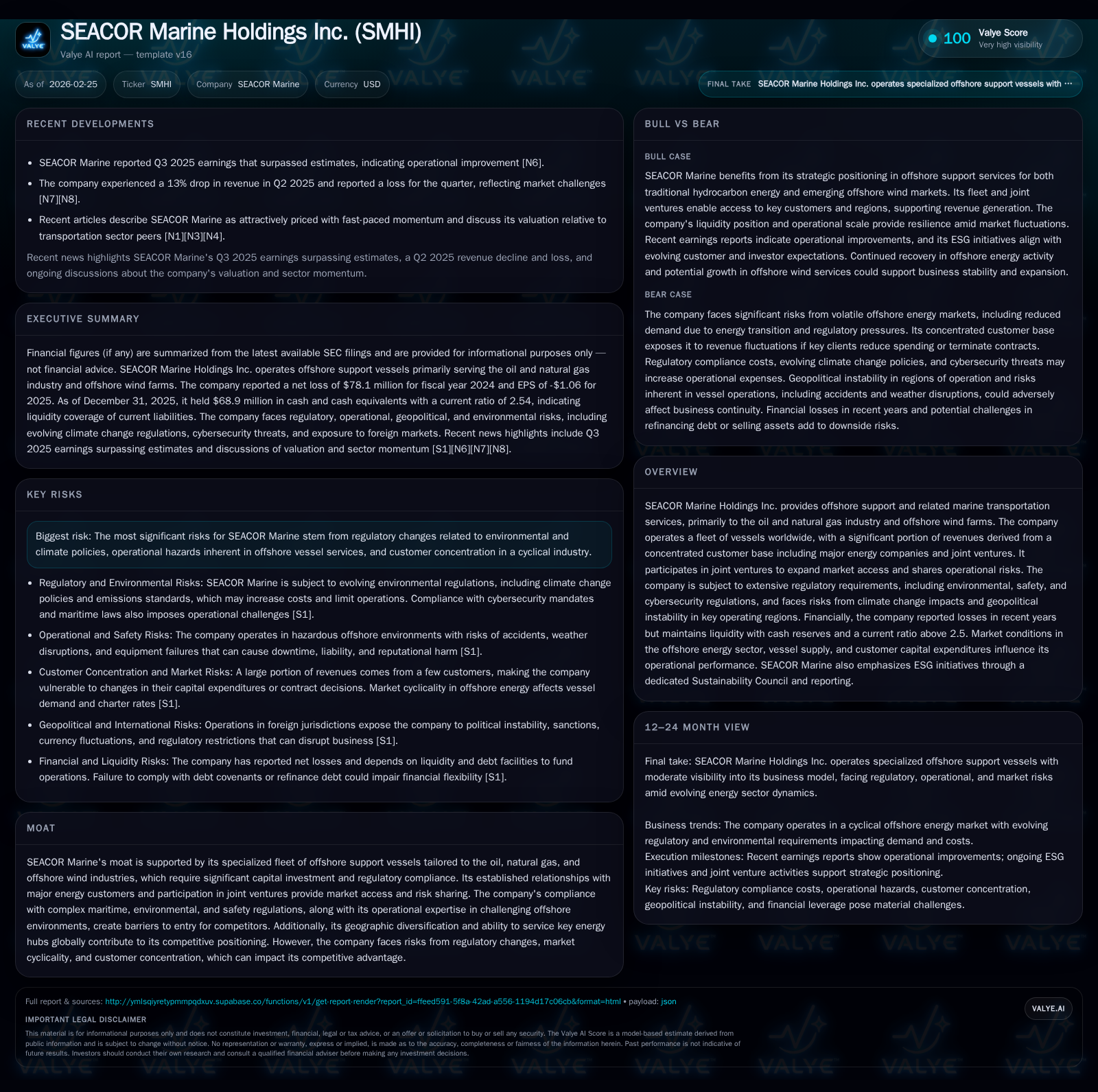

SEACOR Marine Holdings Inc. (SMHI) has experienced a turbulent recent past marked by fluctuating operating income and net losses amid a cyclical offshore marine sector. The company’s specialized vessel fleet and joint ventures underpin its market moat, yet regulatory volatility and customer concentration pose persistent risks. In 2025, the company returned to operating profitability but faced significant negative operating cash flows and heavy capital expenditures. Future growth depends on offshore oil, gas, and wind activity, balanced against evolving climate policies and geopolitical uncertainty. Monitoring cash flow trends, regulatory developments, and contract stability will be critical to assessing the company's trajectory.

Company Overview

SEACOR Marine Holdings Inc. (SMHI) provides crucial offshore support and marine transportation services primarily servicing the oil and natural gas sectors alongside emerging offshore wind projects globally [S1]. The business model revolves around a fleet of specialized vessels tailored for this capital-intensive energy segment, coupled with joint ventures facilitating expanded market footprint while sharing financial and operational risks [S6][S27]. SEACOR’s competitive advantages stem from its vessel specialization, compliance expertise in an increasingly regulated environment, long-standing relationships with major energy companies, and geographic diversity servicing key hubs worldwide [S18].

Historical Performance and Drivers

SMHI’s financial performance over the last several years shows wide swings linked to sector cyclicality and regulatory impacts. Operating income dropped sharply in 2022 (-$54M) and 2024 (-$10M), recovering to positive territory ($13.7M) in 2025 [F1]. Net income mirrored this volatility with steep losses across 2022-2024, including -$78M in 2024 [F1]. Revenue data beyond FY2017 is limited; however, the latest reported revenue was approximately $49.3 million as of the end of 2017 [F1]. This disparity indicates fluctuating utilization tied closely to customer spending on offshore exploration, development activities, and maintenance cycles.

Operating cash flow has been especially problematic — negative $36.4 million for FY2025 — compounded by sharply increased capital expenditures totaling nearly $49 million that year [F1]. This pattern reflects reinvestment into fleet modernization or expansion amidst uneven earnings. Despite these pressures, liquidity metrics remain healthy with year-end 2025 cash balances approaching $69 million and a current ratio over 2.5 indicating solid short-term solvency [F1][S5]. Debt totals approximately $339 million under a credit facility bearing fixed interest at over 10%, restricting financial flexibility via covenants but currently maintained in compliance [F1][S5]. Equity decreased from $378M in 2022 to roughly $264M by end-2025 reflective of accumulated losses [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -36 | 14 | 49 | ||

| 2024 | -78 | -10 | -10 | 7 | -738.8% |

| 2023 | -9 | 36 | 11 | +87.0% | |

| 2022 | -72 | -54 | 0 | -316.2% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -85 | |

| 2024 | -18 | -26.2 |

| 2023 | -2.5 | |

| 2022 | -18.9 |

Source: SEC companyfacts cache [F1].

Note: Operating income YoY reflects change between FY24-FY25; net income YoY reflects change between FY23-FY24.

This uneven historical financial profile illustrates dependence on offshore energy industry cycles as well as regulatory cost pressures impacting margins.

Industry Context

The offshore marine services sector is intensely sensitive to oil & gas exploration budgets which fluctuate widely based on commodity prices, technological advancements such as ultra-deep water drilling capabilities, shifts toward renewables like offshore wind farms, plus geopolitical events influencing supply chains . Vessel utilization also peaks seasonally—primarily in northern hemisphere summers—with adverse weather disruption carrying significant operational risk [S28][S21].

Compliance burdens have intensified recently: new US Coast Guard cybersecurity training rules add IT system costs; EPA methane emission reductions impose new standards affecting customers’ drilling operations potentially reducing vessel demand; SEC climate-related disclosure requirements remain pending judicial review but can increase reporting obligations; evolving state-implemented carbon regulations may restrict non-compliant vessels’ operation or devalue older assets requiring fleet upgrades [S14][S16][S21].

Furthermore, the overturning of Chevron deference injects complexity into judicial treatment of agency regulations adding uncertainty potentially hindering long-term planning for operators like SMHI [S13][S22].

The maritime sector also sees growing adoption of tech innovations such as AI-enabled fleet scheduling, emission tracking analytics, predictive maintenance – technology arms races driving differentiation alongside traditional commercial factors [S18]. Larger competitors with stronger balance sheets increasingly leverage these tools to gain competitive advantages.

Future Growth Prospects

SEACOR Marine’s path forward hinges on several variables:

- Energy Sector Activity: Demand from upstream oil/gas producers governs vessel utilization rates; a rebound or sustained investment in offshore developments would catalyze growth.

- Offshore Wind Expansion: Rising focus on clean energy opens incremental opportunities servicing wind farm construction/maintenance though still nascent compared with fossil fuel clientele.

- Regulatory Compliance Costs: Increasingly strict environmental mandates could raise costs or force fleet retirements constraining capacity unless investments accelerate.

- Joint Ventures: These partnerships can unlock new markets or share risks but depend on cooperative governance dynamics.

- Technological Investments: Adoption of emerging IT fleet management tools could improve efficiencies enabling better client retention or margin improvement.

Risks that may cap growth include cyclical downturns in hydrocarbon spending due to price shocks or policy shifts favoring renewables; customer consolidation trimming service contracts; climate-related operational disruptions; heightened litigation or insurance costs following accidents; competitive erosion by fleets with advanced technology or lower debt burdens [S6][S18][S19][S21].

Outlook & Milestones to Watch

No explicit guidance has been disclosed recently regarding revenue or earnings targets [N#][S#], so monitoring will focus on:

- Quarterly updates on vessel utilization rates reflecting offshore sector trends.

- Regulatory announcements particularly EPA/state methane plans implementation details impacting clients.

- Updates on joint venture expansions or disputes.

- Capital expenditure patterns signaling fleet growth or upgrades.

- Debt covenant compliance status given high leverage.

- Progress reports from the Sustainability Council detailing ESG goal adherence which influence investor sentiment.[S1][S9]

Returns & Capital Allocation

With losses depressingly extended until recent operational recovery, SMHI’s return on equity has been negative—approximated at -29%—driven largely by recurring net losses through at least FY2024 [F1]. Cash flow management remains challenging given negative operating cash flows compounded by elevated capital expenditures needed both for fleet maintenance/modernization as well as compliance investments [F1].

Despite strained cash flows, the company repurchased shares worth about $7 million in FY2025 indicating some confidence in capital allocation efficiency or opportunistic buybacks amid depressed stock pricing [F1]. No dividend information is reported suggesting focus remains on reinvestment and debt reduction given interest obligations exceeding annual EBIT margins earlier years.

Debt servicing will continue commanding attention considering the fixed cost nature of interest payments on outstanding credit facilities approaching $339 million at over 10% interest rate with operational volatility presenting risks for covenant breaches which could prompt acceleration clauses affecting liquidity [F1][S5].

Risk Factors Summary

SEACOR faces an array of risks: operational hazards inherent in offshore maritime activities have caused accidents impacting personnel safety and reputation historically prompting stringent safety protocols including regular audits [S1]. Concentrated customer exposure adds volatility risk as loss or contract reduction from any major client substantially impacts revenues given cancellable contracts with low liquidated damages provisions [S6][S27].

Environmental regulation evolution increases compliance cost burdens directly via equipment upgrades or indirectly through reduced customer demand if emissions constraints suppress upstream activity [S9][S14][S20]. Cybersecurity mandates impose additional cost layers amid growing digital shipboard system reliance [S14][S16].

Geopolitical instability affects regional operations variably across U.S., Africa/Europe, Middle East/Asia and Latin America locales requiring dynamic asset redeployment often challenged by local shipping laws favoring flagging/ownership restrictions further complicating fleet management efficiency [S25][S27][S28].

Litigation exposure spans property damage claims to anti-corruption statutes enforcement potentialities emphasizing need for robust compliance programs but management presently believes no material adverse effects are expected currently from pending cases [S4][S19][S24]. Negative public perceptions following incidents could hamper recruitment or customer relations creating intangible reputational risks relevant for tendering future contracts [S19][S24].

Summary

In sum, SEACOR Marine Holdings embodies a highly specialized player within the offshore marine services realm wrestling with cyclical headwinds amplified by tightening environmental regimes and rising technological competition. Recent signs point toward an operating profit resurgence despite continued net losses underscoring fragile financial health weighed down substantially by capital expenditures needed for fleet upkeep amidst regulatory mandates.

Monitoring quarterly activity metrics alongside diligence on evolving climate policies affecting both the company’s operations directly and its customers' upstream capital plans will be vital indicators of near-term outlook shifts. The interplay between sustained demand in hydrocarbons alongside emerging renewable energy service opportunities will likely define medium-term growth scope while capitalization decisions will critically influence financial resilience.

Disclaimer: This analysis is prepared solely for informational purposes grounded exclusively on provided SEC filings and publicly available data as of February 25, 2026. It does not constitute investment advice or recommendation towards SEACOR Marine Holdings Inc.'s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments